The trajectory of the hydrogen sector in the United States hinges on a critical question: what criteria will be used to define the term “clean hydrogen” for tax purposes?

As previously outlined in our Field Guide to Clean Hydrogen, the stakes are high because the “clean hydrogen” label is the key to securing a broad array of federal government benefits and subsidies, including the new clean hydrogen production tax credit of up to $3 per kilogram (kg) of hydrogen under Section 45V (the “45V Credit”) of the Internal Revenue Code of 1986 (the “Code”). The Bipartisan Infrastructure Law (the “BIL”) enacted in 2021 and the Inflation Reduction Act of 2022 (the “IRA”) both established multiple clean hydrogen focused incentives. The BIL appropriated approximately $9.5 billion to the Department of Energy (“DoE”) for hydrogen focused programs. The full spectrum of the IRA’s hydrogen related provisions is discussed in this King & Spalding Client Alert.

On December 22, 2023 the IRS and Treasury provided a long-awaited definition for “clean hydrogen” in proposed regulations interpreting the 45V Credit (REG-117631-23) (the “45V Proposed Regulations”). Their release was coordinated with the DoE, which issued a “White Paper”, model and associated manual (the “GREET User Manual”) on measuring greenhouse gas (“GHG”) emissions. The Environmental Protection Agency (“EPA”) also issued a letter (“EPA Letter”) responding to the Treasury’s request for information related to the definition of lifecycle GHG emissions under the Clean Air Act to support Treasury’s interpretation and implementation of Section 45V.

The 45V Proposed Regulations were issued a month after the issuance of proposed regulations interpreting the Investment Tax Credit under Section 48 (the “ITC”). The proposed ITC regulations address the potential tax credit for qualifying hydrogen storage property and these proposed regulations limit taxpayers’ ability to claim the ITC for hydrogen storage to a very narrow set of circumstances. Please see our Client Alert IRS and Treasury Issue Section 48 Investment Tax Credit Proposed Regulations.

The definition of clean hydrogen under the 45V Proposed Regulations has drawn an unprecedented amount of attention and lobbying on all sides of the debate. This attention is the likely reason guidance was issued more than four months after the statutory deadline of August 16, 2023. Now that the 45V Proposed Regulations have been published, we expect similar or even more intense attention and lobbying on all sides regarding this critical element of the IRA and the Biden Administration’s overall hydrogen policy.

This Client Alert summarizes the key elements of the 45V Proposed Regulations and will be followed during and after the comment period (ending on February 26, 2024) by further in-depth analyses of specific issues arising from the combination of the 45V Proposed Regulations and the proposed ITC regulations.

KEY TAKEAWAYS

The 45V Proposed Regulations provide rules for:

- determining lifecycle GHG emissions resulting from eight identified hydrogen production pathways;

- petitioning for provisional emissions rates for hydrogen production pathways not covered by the regulations;

- verifying the production and qualifying sale or use of clean hydrogen;

- retrofitting or modifying existing hydrogen production facilities;

- qualifying use of electricity from certain renewable or zero-emissions sources to produce qualified clean hydrogen; and

- electing in lieu of the 45V Credit to treat a clean hydrogen production facility as property eligible for the ITC.

A taxpayer can rely on the proposed regulations for taxable years beginning after December 31, 2022, and before the final proposed regulations are published, provided the taxpayer follows the proposed regulations in their entirety and in a consistent manner.

Most notably, the 45V Proposed Regulations propose rules similar to the European Union (EU)’s "three pillars” approach for the strictest method of hydrogen production using electrolysis (i.e., “renewable” hydrogen or “RFNBO”). Adoption of the three pillars means that, for hydrogen to be considered “clean” and eligible for the 45V Credit, (i) the production facility may not draw from electricity generating facilities that are more than 36 months older than the hydrogen production facility (which the 45V Proposed Regulations call “incrementality”), (ii) electricity used to make the hydrogen must be generated in the same year through 2027 and from 2028 in the same hour (“temporal matching”), and (iii) the electricity must be from the same geographic region (“deliverability”). The three pillars under Section 45V are implemented by requiring use of Energy Attribute Certificates (“EACs”) which taxpayers are required to obtain and retire unless they want to use an emissions profile for the regional electricity grid.

The incrementality and temporal matching rules will likely draw a significant amount of attention and comment. The regulatory preamble does raise the prospect that excess (and therefore not generated) low emissions energy (sometimes called curtailed energy) or even actually generated low emissions energy (such as nuclear) that would otherwise be underutilized or even unused could be deemed to meet the incrementality rule. However, the temporal matching rule in the 45V Proposed Regulations is potentially stricter than the EU’s RFNBO rule, which requires monthly matching through 2029 and moves to hourly matching in 2030 (although EU states can voluntarily adopt hourly matching from 2027). The RFNBO rule also permits some grandfathering of existing facilities, while the 45V Proposed Regulations do not.

The preamble confirms that the 45V Credit is available even if the hydrogen is sold or used outside the United States. Where hydrogen is exported to the EU and intends to qualify as RFNBO for the purpose of the EU quotas, the production of the hydrogen in the United States will also need to comply with the RFNBO rules. Notably, the RFNBO rules are stricter in some ways, particularly where grid electricity used to produce hydrogen benefits from tax subsidies.

The 45V Proposed Regulations also acknowledge the possibility of geologic hydrogen as a production pathway outside of the general framework the rules introduce and therefore eligible for a provisional emissions rate.

BACKGROUND

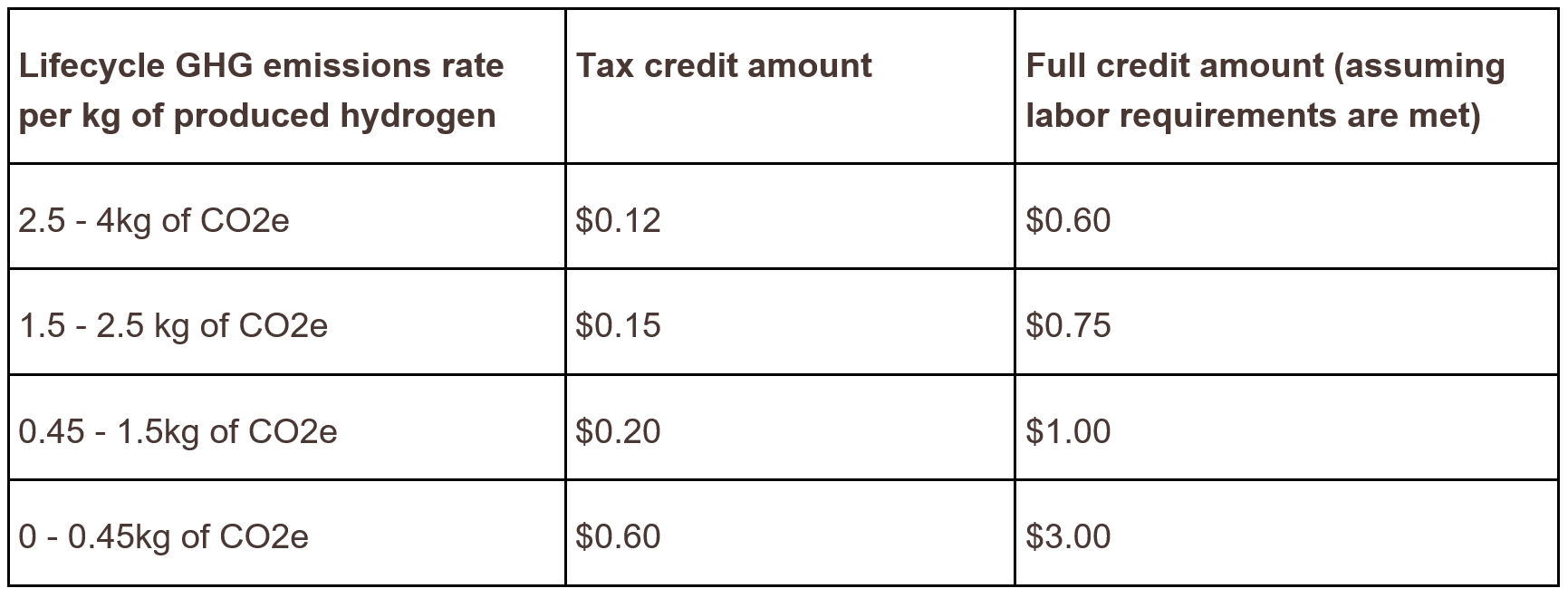

The 45V Credit, which was enacted by the IRA, provides a credit of up to $3.00 for each kg of “qualified clean hydrogen.” Any hydrogen produced at a qualified clean hydrogen production facility that has a lifecycle GHG emissions rate of 4 kg CO2e per kg of hydrogen or less is statutorily defined as clean hydrogen. The 45V Credit is generally effective for clean hydrogen produced from qualifying facilities placed in service after January 1, 2023 and before January 1, 2033. The 45V Credit is available for ten years from the date a qualifying facility is placed in service.

The 45V Credit has four tiers of credits available depending on the lifecycle GHG emissions rate of the process used to produce hydrogen, as shown in the table below.

The IRA’s definition of lifecycle GHG emissions refers to the Argonne National Laboratory’s Greenhouse gases, Regulated Emissions, and Energy use in Transportation (“GREET”) model, or a successor model as determined by the Treasury and IRS, and importantly, limits the definition to include only emissions through the point of production (“well-to-gate” emissions). The DoE issued a specific GREET model (the “45VH2-GREET”) for Section 45V along with the White Paper. Please see our Client Alert IRS Proposed Regulations and DOL Guidance Clarify Certain Aspects of the Prevailing Wage and Apprenticeship Requirements for more information regarding the prevailing wage and apprenticeship rules. Forms of the GREET model have utility beyond Section 45V, including Section 40B and California’s Low Carbon Fuel Standard.

LIFECYCLE GHG EMISSIONS RATE

Taxpayers claiming the 45V Credit must determine the lifecycle GHG emissions of their production facility for each taxable year using the latest version of the 45VH2-GREET that is publicly available on the first day of the taxpayer’s taxable year in which the qualified clean hydrogen was produced.1

The 45VH2-GREET model includes emissions associated with feedstock growth, gathering, extraction, processing, and delivery to a hydrogen production facility. It also includes the emissions associated with the hydrogen production process, including electricity used by the hydrogen production facility and any capture and sequestration of carbon dioxide generated by the facility. Moreover, the 45VH2-GREET includes a number of different hydrogen pathways, which currently include the following eight pathways:

- steam methane reforming (“SMR”) of natural gas, with potential carbon capture and sequestration (“CCS”);

- autothermal reforming (“ATR”) of natural gas, with potential CCS;

- SMR of landfill gas with potential CCS;

- ATR of landfill gas with potential CCS;

- coal gasification with potential CCS;

- biomass gasification with corn stover and logging residue with no significant market value with potential CCS;

- low-temperature water electrolysis using electricity; and

- high-temperature water electrolysis using electricity and potential heat from nuclear power plants.

The 45VH2-GREET model allows users to input data related to a hydrogen production facility, execute GREET calculations in the background, and display the well-to-gate carbon intensity of produced hydrogen in kg of CO2e/kg of hydrogen. Taxpayers must enter all requested information about their qualified clean hydrogen production facility in compliance with the most recent version of the GREET User Manual.

The initial 2023 version of 45VH2-GREET does not model every possible feedstock used by a hydrogen production facility and does not represent all hydrogen production technologies that are currently of commercial interest or that may be commercially viable in the future (e.g., technologies used to drill for geologic hydrogen). The 45V Proposed Regulations therefore allow taxpayers with an alternative hydrogen production pathway to file a petition with the Treasury and IRS to obtain carbon intensities.2

In order to receive a provisional emissions rate (“PER”), the taxpayer must attach a PER petition to its federal income tax return or information return for the first taxable year of hydrogen production ending within the 10-year credit period. A PER petition must contain the following information:

- an emissions value obtained from the DoE setting forth the DoE’s analytical assessment of the lifecycle GHG emissions rate associated with the facility’s hydrogen production pathway; and

- a copy of the taxpayer’s request to the DoE for an emissions value, including any information that the taxpayer provided to the DoE pursuant to the emissions value request process specified in the 45V Proposed Regulations.

The 45V Proposed Regulations provide that the emissions value request process and criteria will be specified by the DoE and will open on April 1, 2024. Upon the IRS’s acceptance of the taxpayer’s return containing a PER petition, the emissions value specified on such PER petition will be deemed accepted. Provided all other requirements of Section 45V are satisfied and until the lifecycle GHG emissions rate is available on the 45VH2-GREET, the taxpayer may use a PER determined by the Treasury and IRS beginning with the first taxable year in which a PER has been obtained and for any subsequent taxable year during the 10-year period beginning on the date a qualified clean hydrogen production facility was originally placed in service.

Any information, representations, or other data provided to the DoE in support of the request for an emissions value are subject to later examination by the IRS. The taxpayer’s request for an emissions value will be automatically denied if an updated version of the 45VH2-GREET includes the taxpayer’s hydrogen production pathway.

The 45VH2-GREET model helpfully allows users to allocate emissions for co-products. The hydrogen production process may generate other commercially useful products.3 The model generally uses a system expansion approach for co-products allowing for an allocation of emissions to all useful products generated during the production process. However, the model restricts the amount of co-product in circumstances the Treasury believes would incentivize generation or over production of hydrogen co-products in order to enable access to a higher tax credit value.

THE THREE PILLARS

The greatest controversy surrounding the 45V Proposed Regulations has been how to account for the emissions footprint associated with electricity inputs for hydrogen pathways using electrolyzers to extract hydrogen from water. The preamble to the 45V Proposed Regulations confirms that electricity will have a GHG emissions profile that accounts for direct and indirect emissions. As noted in our Field Guide to Clean Hydrogen, much of the controversy revolves around whether the EU’s “three pillars” of additionality, regionality and temporal matching for RFNBO production should be incorporated into the US regulatory definition for qualified clean hydrogen as a means of accounting for indirect emissions (i.e., emissions associated with the generation of the electricity).4

The 45V Proposed Regulations adopt a form of the three pillars as outlined below. This approach is implemented by requiring use of EACs to document the emissions profile for electricity inputs in certain circumstances. Failure to use EACs will mean that the taxpayer will need to use the emissions profile for the regional electricity grid as determined in the 45VH2-GREET model.

EACs include Renewable Energy Certificates (“RECs”) and other zero-emission attribute certificates, such as those associated with nuclear power generation. Qualifying EACs incorporate a three pillars approach of incrementality (i.e., additionality), deliverability (i.e., regionality or geographical correlation), and temporal matching. All three pillars limit the ability of hydrogen producers to claim that low carbon intensity electricity has been used in generating hydrogen and therefore the ability to claim the 45V Credit.

The preamble to the 45V Proposed Regulations notes that the EAC approach was adopted in consultation with the DoE and EPA. Based on this consultation, the Treasury and IRS determined that strict requirements are necessary to “ensure that hydrogen producers’ electricity use can be reasonably deemed to reflect the emissions associated with the specific generators from which the EACs were purchased and retired.” The EPA Letter concludes that it would be reasonable for the Treasury to include “induced grid emissions” (i.e., indirect emissions) when determining the lifecycle GHG emissions for electrolytic hydrogen. The preamble to the 45V Proposed Regulations concludes that qualifying EACs can serve as “a reasonable methodological proxy” to quantify indirect emissions for electrolytic hydrogen.

Each of the three elements of the “three pillars” approach is described in more detail below:

1. Incrementality

An EAC meets the incrementality requirement if the electricity generating facility that produced the unit of electricity to which the EAC relates has a commercial operations date (“COD”) that is no more than 36 months before the hydrogen production facility for which the EAC is retired was placed in service.5

The 45V Proposed Regulations provide an alternative test for establishing incrementality due to an increase in an electricity generating facility’s rated nameplate capacity and determining the facility’s uprated production.6 Under the 45V Proposed Regulations, an EAC satisfies the alternative test if the electricity represented by the EAC is produced by an electricity generating facility that had an uprate (i.e., an increase in an electricity generating facility’s rated nameplate capacity ) no more than 36 months before the hydrogen production facility with respect to which the EAC is retired was placed in service and such electricity is part of such electricity generating facility’s uprated production. An uprated electricity generating facility’s production must be prorated to each hour or year of such facility’s generation in order to determine the electricity to which the uprate relates.7

The preamble notes that there may be circumstances in which an existing higher-emitting electricity generating facility may make upgrades to subsequently deliver minimal-emitting (i.e., zero or near zero) electricity (e.g., adding CCS capability to an existing fossil-fuel electricity generating facility). The Treasury and IRS request comments on whether and how to provide alternative approaches to identifying circumstances in which there is minimal risk of significant induced grid emissions for certain existing electricity generating facilities.

The incrementality requirement, with no grandfathering for existing facilities, may make claiming the 45V Credit difficult to impossible for zero-emissions electricity sources such as nuclear energy, even though they are explicitly contemplated by the IRA. The preamble notes that the DoE has advised that there are circumstances during which diversion of existing zero or near-zero emissions power generation to hydrogen production is unlikely to result in significant induced GHG emissions. This may include curtailment scenarios or where “minimal-emitting power plants” would retire absent the ability to sell electricity for qualified clean hydrogen production. The Treasury and IRS are seeking comments on alternative approaches to identifying circumstances in which there is minimal risk of significant induced grid emissions for certain existing electricity generating facilities.

The 45V Proposed Regulations differ from the EU’s approach to the three pillars, which generally permits grandfathering of pre-existing facilities in certain circumstances.

2. Temporal Matching

An EAC meets the temporal matching requirement if the electricity represented by the EAC is produced in the same hour in which the hydrogen production facility consumes the same quantity of electricity in the production of hydrogen.8 The 45V Proposed Regulations permit annual matching before January 1, 2028 but there is no grandfathering of existing facilities.

The Treasury and IRS acknowledged that hourly tracking systems are not yet broadly available across the country and clarified that this transition rule is intended for the EAC market to develop the hourly tracking capability necessary to verify compliance with this requirement.

3. Deliverability

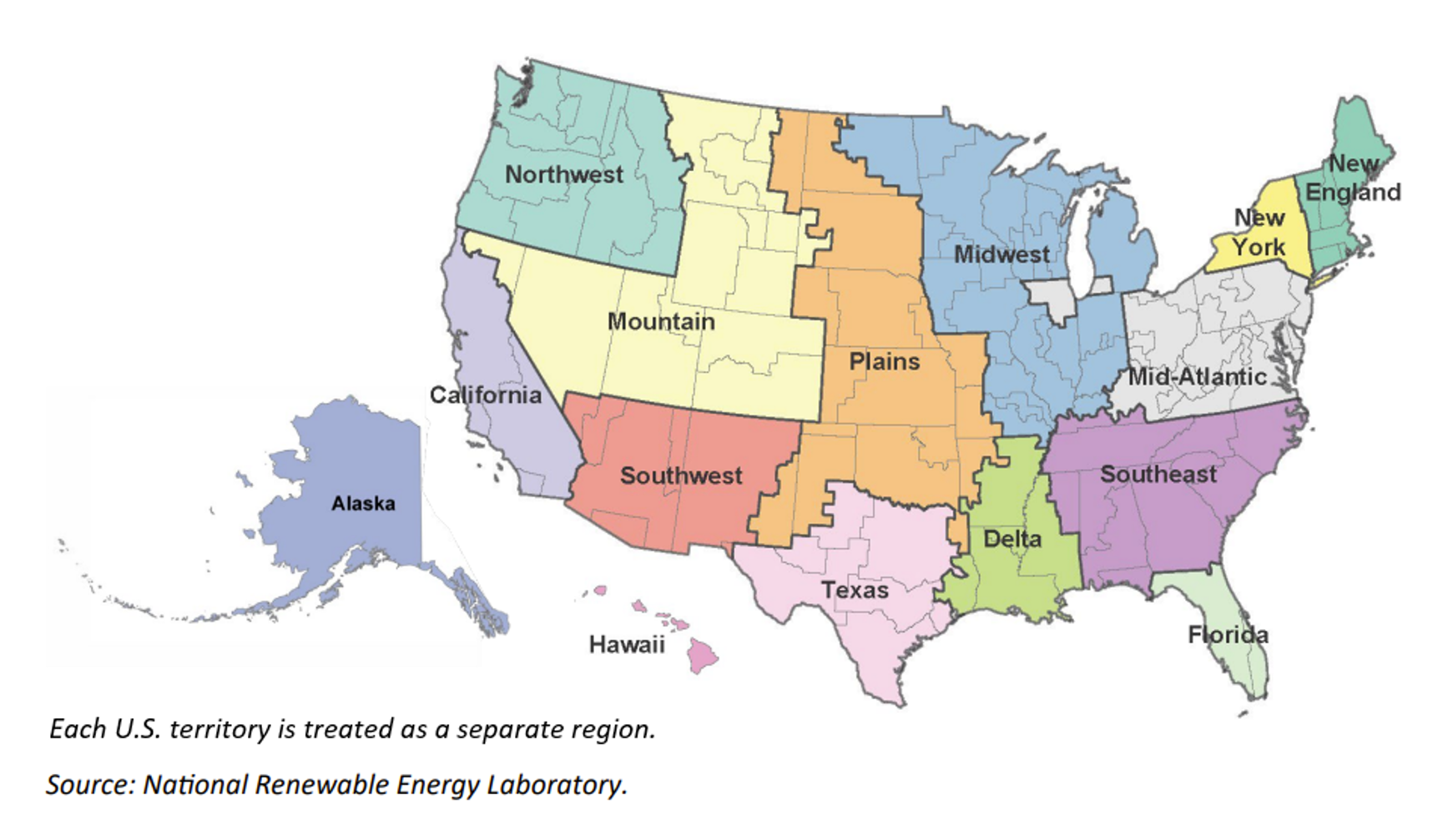

Under the deliverability requirement, qualifying EACs must represent electricity that was produced by an electricity generating facility that is in the same region as the relevant hydrogen production facility.9 The 45V Proposed Regulations provide that the following regions identified in the DoE’s National Transmission Needs Study released on October 30, 2023 will be used for purposes of the deliverability requirement:10

The Treasury Department and the IRS request comments on whether there are additional ways to establish deliverability, such as circumstances indicating that electricity is actually deliverable from an electricity generating facility to a hydrogen production facility, even if the two are not located in the same region or if the clean electricity generator is located outside of the United States.

VERIFICATION

Section 45V requires the production and sale or use of hydrogen to be verified by an unrelated party. The 45V Proposed Regulations define “production for sale or use” to mean “for the primary purpose of making ready and available for sale or use” and that post-production storage of the hydrogen is not a disqualification event.11 The 45V Proposed Regulations also clarify that a verifiable use of qualified clean hydrogen can occur within or outside the United States. This confirms the ability to claim the 45V Credit for exported hydrogen. A verifiable use, however, does not include using hydrogen to generate electricity that is then directly or indirectly used to produce more hydrogen or venting or flaring hydrogen.12

The 45V Proposed Regulations provide that a verification report must be attached to the taxpayer’s Form 7210, Clean Hydrogen Production Credit (or any successor form(s)) and included with the taxpayer’s federal income tax return or information return for each qualified clean hydrogen production facility and for each taxable year in which the taxpayer claims the 45V Credit.13

The verification report must be prepared by a qualified verifier under penalties of perjury, and must contain the following information:

- an attestation from the qualified verifier regarding the taxpayer’s production of qualified clean hydrogen for sale or use during the taxable year;

- an attestation from the qualified verifier regarding the amount of such qualified clean hydrogen sole or use;

- an attestation from the qualified verifier regarding conflicts of interest;

- certain information regarding the qualified verifier, including documentation of the qualified verifier’s qualifications;

- certain general information about the taxpayer’s hydrogen production facility where the hydrogen production undergoing verification occurred (e.g., location, method of hydrogen production, type(s) and amount(s) of feedstock(s), etc.); and

- any documentation necessary to substantiate the verification process given the standards and best practices prescribed by the qualified verifier’s accrediting body and the circumstances of the taxpayer and the taxpayer’s hydrogen production facility.

The preamble to the 45V Proposed Regulations requests comments on whether there are additional safeguards that the regulations could adopt to prevent abusive 45V Credit claims.

FACILITY DEFINITION

The 45V Proposed Regulations define “facility” as a single production line that is used to produce qualified clean hydrogen. A “single production line” would include all components of property that function interdependently to produce qualified clean hydrogen.14 Components of property (including those that have a purpose in addition to the production of qualified hydrogen) are functionally interdependent if the placing in service of each component is dependent upon the placing in service of each of the other components to produce qualified clean hydrogen. A facility does not include (i) equipment used to condition or transport hydrogen beyond the point of production and (ii) electricity production equipment used to power the hydrogen production process, including any carbon capture equipment associated with the electricity production process. A single location can technically have multiple 45V Credit facilities.

The 45V Proposed Regulations permit the modification of existing facilities to enable qualifying 45V Credit eligible production. A qualifying modification occurs for a facility originally placed in service before January 1, 2023 if it is subsequently modified to produce qualified clean hydrogen. In such case it will be deemed to have been originally placed in service as of the date the property required to complete the modification is placed in service.15 In addition, amounts paid or incurred with respect to the modification must be properly chargeable to the taxpayer’s capital account. The 45V Proposed Regulations require that the modification must be made for the purpose of enabling the facility to produce qualified clean hydrogen. For example, changing fuel inputs to the hydrogen production process, such as switching from conventional natural gas to renewable natural gas, would not qualify as a facility modification.16

With respect to retrofitting an existing facility, the 45V Proposed Regulations provide that the existing facility may establish a new placed-in-service date (i.e., the date on which the new property added to the facility is placed in service) for purposes of Section 45V provided the fair market value of the used property is not more than 20 percent of the facility’s total value (the “80/20 Rule”).17 For purposes of the 80/20 Rule, the cost of new property includes all properly capitalized costs of the new property included within the facility.

ITC ELECTION IN LIEU OF THE 45V CREDIT

Section 48 allows taxpayers to make an irrevocable election to claim an ITC with respect to their clean hydrogen production facilities placed in service after December 31, 2022 in lieu of the 45V Credit. Proposed Treasury Regulations Section 1.48-15 provides the energy percentage that is used to calculate an ITC for a clean hydrogen production facility that is “designed and reasonably expected to produce” qualified clean hydrogen through a process that results in a lifecycle GHG emissions rate of not greater than 4 kg of CO2e per kg of hydrogen. “Designed and reasonably expected to produce” means hydrogen produced through a process that results in the GHG emissions rate specified in the verification report for the taxable year in which the ITC is claimed.

For each taxable year thereafter during the 5-year recapture period, the taxpayer must obtain an annual verification report (signed under penalties of perjury) by a qualified verifier. An “emissions tier recapture event” occurs if the taxpayer (i) fails to timely obtain an annual verification report, (ii) the clean hydrogen production facility actually produced hydrogen through a process that results in a lifecycle GHG emissions rate that can only support a lower energy percentage than the percentage used to calculate the amount of the ITC, or (iii) the facility actually produced hydrogen through a process that results in a lifecycle GHG emissions rate of greater than 4 kgs of CO2e per kg of hydrogen. The recapture amount is 20 percent of the excess of the ITC allowed to the taxpayer with respect to its clean hydrogen production facility for the taxable year in which the facility was placed in service over the ITC that would have been allowed if the taxpayer had used the lower energy percentage reflecting the actual production to calculate the ITC.

STACKING CREDITS

The ability to stack tax credits for hydrogen production is a key component of the IRA. The statutory scheme expressly permits claiming the 45V Credit even if the electricity itself benefits from a clean electricity tax credit (Section 45 for renewables and Section 45U for nuclear). Further, taxpayers with eligible hydrogen storage can separately claim an ITC for the hydrogen storage property without impairing the 45V Credit. Please see our Client Alert IRS and Treasury Issue Section 48 Investment Tax Credit Proposed Regulations. However, Section 45V explicitly prohibits stacking of its tax credit with the tax credit for carbon oxide sequestration (Section 45Q).

Many taxpayers hoped that there would be a means to square the circle and claim credits under both the Section 45Q and Section 45V rules for the same hydrogen production facility. The 45V Proposed Regulations directly address this issue in an example with a facility equipped with carbon capture equipment. If carbon capture equipment is necessary to produce hydrogen through a process resulting in lifecycle GHG emissions rate falling within the eligible 45V Credit range, the equipment is treated as part of the 45V Credit facility and therefore the taxpayer cannot claim both the Section 45Q Credit and the 45V Credit. However, if the carbon capture equipment is co-located, but associated with the electricity production process, it should be ignored for this purpose.

RNG AND METHANE

The 45V Proposed Regulations do little to cover hydrogen production pathways using renewable natural gas (“RNG”) or other fugitive sources of methane (for example, from coal mine operations) for purposes of the 45V Credit.18 Instead, the preamble notes that the Treasury and IRS intend to address these issues in further guidance which would apply to all RNG used for the purposes of the 45V Credit and provide conditions that must be met before certificates for RNG or fugitive methane, and the GHG emissions benefits they are meant to represent, may be taken into account in determining lifecycle GHG emissions rates for purposes of the 45V Credit. Critically, the preamble notes that these conditions would be consistent with the three pillars approach for electricity-derived EACs, including the requirement to acquire and retire corresponding “attribute certificates”.

The preamble to the 45V Proposed Regulations generally permits taxpayers to rely upon the 45VH2-GREET or PER process to determine the associated lifecycle GHG emissions rate until the regulations are finalized for production facilities that rely on direct use of landfill gas or any fugitive methane feedstock. However, the gas being used must result from the “first productive use” of the methane from the landfill or fugitive methane source. In this context, the term “direct use” means there is a direct, exclusive pipeline connection between the hydrogen production facility and the source of the procured gas.

EFFECTIVE DATE

The 45V Proposed Regulations and Proposed Treasury Regulations Section 1.48-15 apply to taxable years beginning after December 26, 2023. Taxpayers can rely on the proposed regulations for taxable years beginning after December 31, 2022, and before the final proposed regulations are published, provided the taxpayer follow the proposed regulations in their entirety and in a consistent manner.

1Prop. Reg. § 1.45V-4(b).

2Prop. Reg. § 1.45V-4(c).

3For example, methane pyrolysis is a hydrogen pathway that splits methane from natural gas or biogas into hydrogen and a form of solid carbon that has independent commercial value.

4The EU adopted a detailed set of provisions providing a definitional framework for low or zero carbon hydrogen production, called “renewable fuels of non-biological origin” (i.e., RFNBO). This framework applies equally to production projects located in the EU as well as export projects selling to the EU seeking to qualify their production for the RFNBO quotas.

5Prop. Reg. § 1.45V-4(d)(3)(i). The COD is the date on which a facility that generates electricity begins commercial operations. The general rules for determining an electricity generating facility’s placed in service date for federal income tax purposes would not apply in determining its COD.

6Prop. Reg. § 1.45V-4(d)(3)(i)(B).

7For example, assume that a power plant undergoes an uprate that expands its rated nameplate capacity from a pre-uprate capacity of 10 megawatts (MW) to a post-uprate capacity of 12 MW. After the uprate, its generation output increases to a total of 40,000 megawatt hours (MWh) for the year. The power plant’s incremental generation capacity is 2 MW, its uprated production rate is 0.167 (2 MW divided by 12 MW), and its total uprated production for the year is 6.667 MWh (2 MW divided by 12 MW multiplied by 40,000 MWh). Two-twelfths (0.167) of each hour of the power plant’s production may be considered uprated production. Prop. Reg. § 1.45V-4(d)(3)(i)(C).

8Prop. Reg. § 1.45V-4(d)(3)(ii).

9Prop. Reg. § 1.45V-4(d)(3)(iii).

10https://www.energy.gov/sites/default/files/2023-10/National_Transmission_Needs_Study_2023.pdf.

11Prop. Reg. § 1.45V-1(a)(9)(ii).

12Prop. Reg. §1.45V-5(d)(2).

13Prop. Reg. § 1.45V-5(b).

14Prop. Reg. § 1.45V-1(a)(7)(i).

15For example, consider the following example: Facility X, a hydrogen production facility that was originally placed in service on January 1, 2018, could not produce qualified clean hydrogen. After January 1, 2023, Facility X was modified to produce qualified clean hydrogen, and all amounts paid or incurred with respect to such modifications were properly chargeable to the taxpayer’s capital account for Facility X. The property required to complete the modification was placed in service on June 1, 2023. The taxpayer will be allowed a carbon capture credit under Section 45Q with respect to carbon capture equipment included at Facility X before June 1, 2023. Under this example, although Facility X is deemed to have been originally placed in service on June 1, 2023, because the taxpayer had previously been allowed a Section 45Q Credit with respect to the carbon capture equipment included at Facility X, no 45V Credit is allowable for qualified clean hydrogen produced at Facility X. Example 2, Prop. Reg. § 1.45V-6(c).

16Prop. Reg. § 1.45V-6(a).

17Prop. Reg. § 1.45V-6(b).

18The term RNG refers to biogas that has been upgraded to be equivalent in nature to fossil natural gas. Fugitive methane refers to the release of methane through, for example, equipment leaks, or venting during the extraction, processing, transformation, and delivery of fossil fuels to the point of final use, such as coal mine methane or coal bed methane.