Guidance recently issued by the Department of the Treasury and the Internal Revenue Service (IRS) in proposed regulations (REG-117631-23) will (if held to be final) have a significant impact on green hydrogen projects in the United States. The proposed regulations include a very restrictive interpretation of what types of renewable energy must be used by a hydrogen-producing facility for the resulting hydrogen to qualify for the Section 45V hydrogen production tax credit. In short, for hydrogen produced by renewable energy to qualify for the Section 45V production tax credit, the renewable energy project must achieve commercial operation no earlier than three years before the hydrogen production facility is placed in service, and, beginning in 2028, the renewable energy generation must be hourly matched to the time period of hydrogen production.

The Section 45V production tax credit was part of an overall strategy by the Biden administration to decarbonize America’s heavy-duty transportation industry and its industrial sector (primarily chemicals, steel and refining, including through the establishment of Regional Clean Hydrogen Hubs) and ultimately achieve net-zero carbon emissions by 2050. However, the current cost of approximately $5 per kilogram (kg) to produce green hydrogen (without the production tax credit) poses a significant hurdle to the use of hydrogen in the energy transition. Accordingly, the Section 45V production tax credit (which can amount to as much as $3 per kilogram of hydrogen (H2)) is critical to reducing production costs and expanding the market to improve economies of scale in line with President Biden’s goal to ultimately reduce the cost of clean hydrogen to only $1 per kg.

However, given the restrictive rules proposed by Treasury and the IRS, there is a risk that would-be domestic hydrogen producers will decide to invest overseas in jurisdictions that have much less restrictive requirements on the types of generation that can be used to create hydrogen that qualifies as “green.” While Treasury’s strict proposed requirements may not be welcome by many producers, environmental policy critics have argued they are necessary to ensure that the tax credit does not increase the production of “clean” hydrogen while concurrently increasing net carbon emissions or create a situation where hydrogen is not truly produced by renewable means.

While this guidance does not too heavily impact developers intending to capture and sequester carbon and claim the resulting Section 45Q tax credit as part of their hydrogen production, the proposed regulations do create significant headwinds to those taxpayers that were not anticipating the need to pair their hydrogen production with new renewable generation. For developers whose projects may be hindered by these proposed regulations, now is the time to prepare focused and constructive comments to the IRS and also to start exploring opportunities to pair their planned hydrogen production with qualifying renewable generation. This article highlights the initial structure of the Section 45V tax credit, the constraints of the current guidance and a path forward to continue to advance the green hydrogen industry in the U.S.

Overview of Section 45V

The clean hydrogen production tax credit was added to the Internal Revenue Code (as new Section 45V) by the Inflation Reduction Act of 2022 (IRA, P.L. 117-169). The tax credit offsets the cost of producing clean hydrogen at a qualified clean hydrogen production facility in the U.S. Facility owners can claim the credit for their facilities’ first 10 years in service, and the credit became available for hydrogen produced in 2023 (after the excise tax credit for liquified hydrogen expired). In general, qualifying hydrogen must be produced (i) in the U.S. or a U.S. possession, (ii) in the ordinary course of a trade or business of the taxpayer and (iii) for sale or use. Additionally, a third party must verify the hydrogen’s production and sale or use. Producers can store the hydrogen before they sell or use it without disqualifying the hydrogen for tax credit eligibility.

A taxpayer cannot claim both the Section 45V credit (or the Section 48 investment tax credit in lieu of Section 45V) and the Section 45Q credit for carbon captured by equipment that is part of the hydrogen production facility. Nor can a taxpayer claim credits under both Sections 45Z and 45V for a single facility during the same taxable year. However, a taxpayer can claim both the Section 45V credit and the Section 45 production credit for clean electricity powering the hydrogen production facility. The Section 45V credit is one of three credits (along with 45Q and 45X) generally eligible for direct pay under Section 6417 for a single five-year period, and the Section 45V credit is transferable under Section 6418, allowing certain taxpayers to sell the credit for cash.

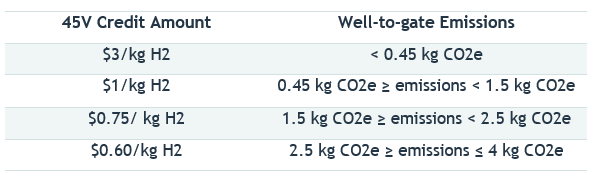

The Section 45V credit amount increases as the carbon intensity of the production process decreases, with four separate credit tiers tied to varying production emissions levels. As the chart below demonstrates, the lower the well-to-gate carbon dioxide equivalent (CO2e) per kg, the more valuable the Section 45V credit becomes.

Note: These credit amounts assume that the taxpayer meets the prevailing wage and registered apprenticeship requirements. If not, the amounts may only be one-fifth (for example, instead of a credit of $3, the credit amount would only be 60 cents). In addition, the credit amounts will be adjusted for inflation.

The well-to-gate emissions rate is determined separately for each facility that a taxpayer owns and is based on all hydrogen produced at a qualified clean hydrogen production facility during the taxable year. For example, one way to produce clean hydrogen is to use electricity to split water into hydrogen and oxygen (i.e., electrolysis). Clean hydrogen produced via electrolysis powered by renewable solar or wind electricity could potentially be eligible for the highest credit amount (given that no carbon dioxide is emitted in the process) and is generally referred to as “green” hydrogen. Clean hydrogen produced via electrolysis powered by nuclear energy is referred to as “pink” hydrogen.

However, electrolysis is not currently the most common way to produce clean hydrogen in the U.S.; most production occurs by a process known as steam methane reforming. Under this process, natural gas (or sometimes, in the case of grey hydrogen, methane) is combined with high-temperature steam to produce hydrogen. However, some carbon dioxide is also emitted as a byproduct. If the producer captures this carbon during the process and stores/sequesters it to contain the emissions, then the associated hydrogen is referred to as “blue” hydrogen. If not, and the producer instead lets the greenhouse gas byproduct into the atmosphere (as is most common in the U.S.), the associated hydrogen is referred to as grey hydrogen.

It is expected that the Section 45V credit could spur the development of new electrolyzer projects. In cases where a facility is owned by more than one taxpayer (which may be common given the capital-intensive nature of these facilities), the credit is allocated in proportion to each owner’s interest in the facility’s gross sales. This means that even if a contract manufacturer is treated as a producer for other purposes of the Internal Revenue Code, the contract manufacturer is not eligible to claim the Section 45V credit for producing qualified clean hydrogen if it does not own the facility.

Additionally, the IRA created the possibility that some producers could decide to modify an existing facility that was not previously equipped to produce qualified clean hydrogen into one that could produce hydrogen capable of maximizing the benefits of Section 45V or 45Q. Such modified facilities may still be eligible for the credit, as long as the property required to complete the modification is placed in service after 2022 and before 2033. Retrofits of existing facilities may also be eligible for the credit under the “80/20 rule,” which generally provides that as long as the fair market value of the existing property is not more than 20% of the modified facility’s total value, then the retrofitted facility may establish a new placed-in-service date for purposes of Section 45V.

Energy Attribute Certificates

Treasury and the IRS have preliminarily decided that hydrogen producers may use energy attribute certificates (EACs) to document electricity inputs and the well-to-gate emissions impacts of the produced hydrogen. However, in keeping with the restrictions on what constitutes renewable generation for purposes of Section 45V, only certain EACs meet the regulations’ criteria—one of which is that the qualifying EAC must be from a specific electricity generating facility and not merely from a regional electricity grid. The producer would need to acquire and retire such qualifying EACs per unit of electricity used to produce hydrogen to ensure that no EACs are double counted. For example, for each megawatt-hour (MWh) of electricity used in the hydrogen production, one MWh of qualifying EACs would need to be acquired and retired, as recorded and verified in a registry.

The proposed regulations define “energy attribute certificate” as “a tradeable contractual instrument, issued through a qualified EAC registry or accounting system . . . that represents the energy attributes of a specific unit of energy produced. . . . Renewable energy certificates (RECs) and other similar energy certificates issued through a registry or accounting system are forms of EACs.” The guidance contains a list of some qualified EAC registries, including Electric Reliability Council of Texas (ERCOT); Midwest Renewable Energy Tracking System, Inc. (M–RETS); North American Registry (NAR); and New York Generation Attribute Tracking System (NYGATS). Eligible EACs must detail, among other things, which technology and feedstock is used to generate the electricity at the specific electricity generating facility, the amount and units of electricity purchased and (starting in 2028) the date and hour the electricity was generated.

Three-Pillar Requirement for EACs

Only those producers that can appropriately document that they purchased and retired a qualifying EAC can claim the clean hydrogen credit. The proposal creates a three-pillar approach to determine whether an EAC qualifies. Specifically, taxpayers must detail that the clean power purchased by the hydrogen producer was:

- From a new or more recent electricity-generating facility (the “incrementality” or “additionality” pillar);

- Generated in the same calendar year or, for electricity generated after 2027, hourly time period as the hydrogen production (the “temporal matching” pillar); and

- Sourced from the same region as the hydrogen production (the “deliverability” or “locality” pillar).

Note that some of the pillars are phased in over time and each have more specific requirements, as more thoroughly defined below. As noted below, the IRS correctly implemented a transition rule requiring the EAC to be hourly matched to the hydrogen production. Given the intermittent nature of renewable energy facilities, it will take some time to determine a structure where the EAC hourly matching requirement will not cause hydrogen production to be equally intermittent unless the industry generally returns to a fixed-shape offtake agreement (which has largely fallen out of favor for renewable energy hedges after 2021’s Winter Storm Uri in Texas).

Pillar One: Incrementality

To satisfy the incrementality requirement, the electricity-generating facility that issued the qualified EAC must have begun commercial operations (note that this is not necessarily the same as a facility’s placed-in-service date) no more than 36 months before the related hydrogen production facility is placed in service. For example, a hydrogen producer that began operations on January 1, 2024, would only qualify for the Section 45V credit if it purchased and retired EACs from an electricity-generating facility with a “commercial operations date” (or COD) on or after January 1, 2021. In this case, the producer’s hydrogen facility would qualify for the full 10-year Section 45V credit period beginning January 1, 2024.

That being said, Treasury and the IRS may allow preexisting fossil fuel electricity-generating facilities (with older CODs) to sell their power to hydrogen producers and satisfy the incrementality requirement if the facilities make subsequent upgrades that reduce the emissions of their electricity (for example, by installing a carbon capture and sequestration system). In addition, the proposed regulations include an alternative test such that if an electricity-generating facility undergoes a production uprate (increasing the power—i.e., nameplate capacity—generated at such facility) within the 36 months preceding the hydrogen facility’s placement in service, the uprated electricity may also satisfy the incrementality requirement.

In the preamble to the proposed regulations, Treasury and the IRS state that they are open to ideas for relaxing the incrementality requirement in cases where “there is minimal risk of significant induced grid emissions” by adopting a demonstrated or modeled minimal-emission approach and are also considering, for example, grandfathering preexisting electricity-generating facilities if their relationship with a hydrogen production facility will help them avoid retirement while continuing to produce renewable or carbon-free electricity. In addition, Treasury and the IRS are considering an alternative, formulaic approach to the incrementality requirement. Under this approach, 5% (or possibly even as much as 10%) of the hourly generation from certain clean-electricity generators placed in service before 2023 would be deemed to satisfy the incrementality requirement. The hope is that such an approach would simplify the determination for certain facilities.

Pillar Two: Temporal Matching

To satisfy the temporal matching requirement, beginning in 2028, the electricity represented by the EAC must have been generated in the same hour that it was used in the hydrogen production facility. However, a transition rule provides that, through the end of 2027, the temporal matching requirement will be satisfied as long as the electricity represented by the EAC was generated in the same calendar year as the hydrogen in question. The transition rule is an acknowledgement that it will take time for the industry to develop tracking systems and contractual structures to support and verify hourly matching.

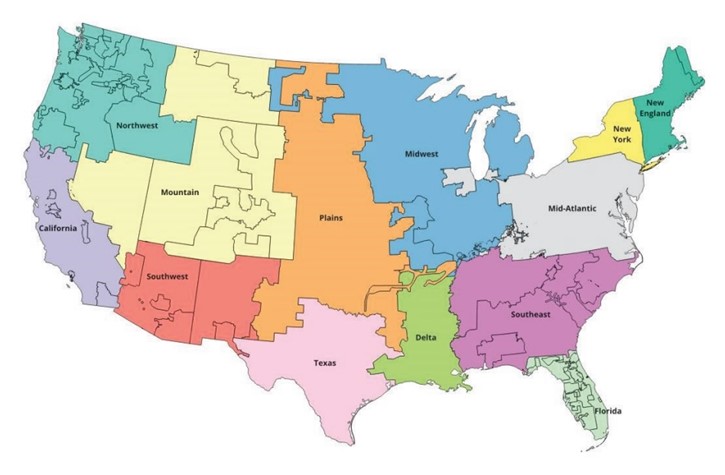

Pillar Three: Deliverability

To satisfy the deliverability requirement, the electricity represented by the EAC must have been generated by a facility that is in the same region as the hydrogen production facility. For this purpose, “region” is defined as “a region derived from the National Transmission Needs Study that was released by the DOE on October 30, 2023.” For this purpose, “Alaska, Hawaii, and each U.S. territory will be treated as separate regions.” The following map shows the various regions in the continental U.S.:

(Source: Guidelines to Determine Well-to-Gate Greenhouse Gas (GHG) Emissions of Hydrogen Production Pathways using 45VH2-GREET 2023)

Well-to-Gate Lifecycle Definition

To maximize the Section 45V credit, hydrogen producers should reduce their life cycle greenhouse gas emissions. For this purpose, well-to-gate emissions under 0.45 kg of CO2e per kilogram of hydrogen result in the maximum Section 45V credit. The proposed regulations specify that well-to-gate emissions would include those associated with: feedstock growth, gathering, extraction, processing and delivery to a hydrogen production facility; and the hydrogen production process, including emissions associated with the electricity used by the facility and any capture and sequestration of carbon dioxide generated by the facility. This calculation (and the resulting credit rate) does not account for greenhouse gas emissions associated with conditioning or transporting the hydrogen past the point of production to its ultimate use (in a fuel cell, for example). Rather, the Section 45V credit calculation incorporates emissions produced between extraction/mining of the raw source material from the ground (i.e., the well) through and including the point at which the hydrogen is actually produced (i.e., the gate). Thus, which power source is used to create the hydrogen is critical in calculating the credit. Note that the regulations defer to the most recent GREET Model (as defined below) to determine exactly where the well starts and where the gate ends.

Defining the Hydrogen Facility

Other important definitions in the proposed regulations include the definition of a qualified clean-hydrogen production facility, which is defined to include only those property components that function interdependently to produce qualified clean hydrogen. Equipment used after the hydrogen is produced (for example, to condition the hydrogen) or equipment used to produce the electricity that powers the hydrogen production (for example, to capture carbon associated with electricity production) would not be included. However, as confirmed by an example in the regulations, any carbon capture equipment that serves multiple purposes and also captures carbon oxides that are a byproduct of the hydrogen production (to ensure that its emission rate falls within the range specific to receive the credit) would be considered functionally interdependent and would be part of the facility.

The GREET Model and Provisional Emissions Rate Petitions

The Greenhouse gases, Regulated Emissions and Energy use in Technologies (GREET) Model is a method of calculating life cycle emissions (including carbon dioxide (CO2)) of a product. The model was developed by the Argonne National Laboratory, and the proposed regulations rely heavily on the GREET Model, specifically the latest version of 45VH2-GREET, to calculate life cycle emissions. For example, one of the fixed, background data assumptions in the GREET Model is the amount of emissions associated with power generation from a specific type of generator.

Treasury and the IRS are seeking comment on whether the final rules could abandon certain of these background, fixed assumptions (including, possibly, the upstream methane loss rate), assuming verification mechanisms improve to create a more complete calculation of the life cycle emissions of a relevant facility.

Note, however, that the current GREET Model only accommodates eight different types of hydrogen production: 1) steam methane reforming (SMR) of natural gas, 2) autothermal reforming (ATR) of natural gas, 3) SMR of landfill gas, 4) ATR of landfill gas, 5) coal gasification, 6) biomass gasification, 7) low-temperature water electrolysis and 8) high-temperature water electrolysis.

The life cycle emissions of any hydrogen produced by another method (or from a feedstock not included in the model) would not be determinable under the GREET Model, and the producer would instead have to petition the Secretary of the Department of Energy (DOE) for a provisional emissions rate (PER). For example, certain types of biomasses (a feedstock) are not factored into the GREET Model. Additionally, the GREET Model cannot analyze the production of hydrogen via geologic drilling. Treasury and the IRS stress that taxpayers that simply disagree with the GREET Model’s background assumptions or calculation approach but whose feedstock or production pathway is incorporated into the model cannot submit a request to DOE for a PER. We expect use of the GREET Model will be a point of contention addressed in comments.

The PER process starts with applying to DOE, and the application period will open April 1, 2024. Only those facilities that have received a front-end engineering and design (FEED) study or similar indicators of project readiness may apply. Additional guidance and procedures for applicants are expected to be released before April 1, 2024. Once a value has been obtained from DOE, the taxpayer would simply then need to attach its PER petition to its tax return for the first taxable year of hydrogen production with respect to which the Section 45V credit is claimed. The petition would include the emissions value obtained from DOE, and the value will be deemed accepted by the IRS and subject to reliance by the taxpayer at the time the related return is accepted. However, as soon as the GREET Model has been updated to include the petitioner’s actual emissions rate (the missing feedstock/production process has been incorporated), the taxpayer may no longer rely on its PER.

Credit Election Mechanics

Owners of qualified hydrogen production facilities can claim the Section 45V credit on the Form 7210, “Clean Hydrogen Production Credit,” attached to their tax return, and they must include with the form a verification report from a qualified, unrelated verifier attesting under penalties of perjury that, among other things, the taxpayer produced qualified clean hydrogen for sale or use during the taxable year.

The verifier must attest to the accuracy of not only the information on the Form 7210, but also the information entered into the GREET Model to determine the well-to-gate emissions rate (if applicable). If the hydrogen is used rather than sold, the verifiable use requirement can be satisfied either within or outside the U.S. According to the proposed regulations, “a verifiable use includes a tolling arrangement pursuant to which a service recipient provides raw materials or inputs, such as water or electricity, to a / (that is, a third-party service provider that owns a hydrogen production facility), and the toller produces hydrogen for the service recipient using the service recipient’s raw materials or inputs in exchange for a fee.” A verifiable use does not include the “[u]se of hydrogen to generate electricity that is then directly or indirectly used in the production of more hydrogen” or venting or flaring of hydrogen (which is deemed wasteful and could also subject the taxpayer to the proposed anti-abuse rule).

The proposed regulations also clarify that even though the credit is determined with respect to the amount of qualified clean energy produced in the taxable year (Year 1, for example) and claimed on that year’s tax return, the taxpayer cannot actually claim the credit until the required verification has occurred, which would happen in a subsequent year (Year 2 or even later). The preamble states that, if the verification does not occur until after the extended return filing deadline for Year 1 has passed, the taxpayer must file an amended return or administrative adjustment request to claim the credit with respect to that hydrogen. Treasury and the IRS specifically request comments on this point.

Section 45V Guidance: Next Steps

The proposed regulations were certainly not the unencumbered catalyst that many expected to jump-start hydrogen production in the U.S. However, the proposed regulations do not directly impact those intending to produce clean hydrogen from nuclear power or hydrogen that takes advantage of carbon capture processes when creating electricity. Further, those surprised by the potentially restrictive guidance are not without hope. First, the Treasury Department has an extensive comment period and is welcoming comments on any aspect of the guidance. Akin is currently helping a number of clients prepare focused and comprehensive comments to this guidance, hoping that a groundswell of support for certain revisions by the industry and across the political spectrum will provide the intended catalyst. Second, with the lengthy and deliberate time horizon during which to claim the Section 45V credit, taxpayers have time to create structures and relationships that qualify under existing guidance.

The proposed regulations would apply to taxable years beginning after December 26, 2023, and taxpayers may generally rely on the proposed regulations until final regulations are published. Comments must be received by February 26, 2024, and a public hearing has been scheduled for March 25, 2024, at 10 a.m. ET.