Our Securities Group breaks down how new regulations will affect special purpose acquisition companies (SPACs) and de-SPAC transactions.

- The SEC requires enhanced disclosures for SPAC IPOs and de-SPAC transactions

- Private companies entering the U.S. market through de-SPAC transactions will also face greater disclosure requirements

- SPACs may now meet the definition of “investment company” and be subject to the Investment Company Act

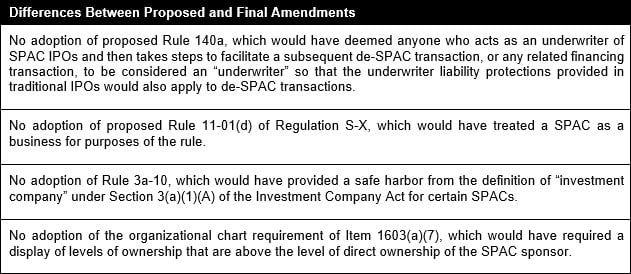

On March 30, 2022, the Securities and Exchange Commission (SEC) proposed amendments to the rules governing disclosures and investor protections in initial public offerings (IPOs) by special purpose acquisition companies (SPACs) and in subsequent business combination transactions between SPACs and target companies (de-SPAC transactions). On January 24, 2024, the SEC considered and adopted the proposed amendments to the enhanced SPAC and de-SPAC disclosures.

New Subpart 1600 of Regulation S-K

As part of the amendments, the SEC added new Subpart 1600 of Regulation S-K, which relates to enhanced disclosure requirements for SPAC IPOs and de-SPAC transactions. The final rules require more extensive disclosures such as more information about SPAC sponsors, conflicts of interest, and sources of dilution.

Overall, the new amendments resemble the disclosure requirements and legal obligations companies incur during a traditional IPO.

Prospective cover page, summary, and other disclosures – Item 1604

Registrants will now be required to include certain disclosures on the cover page and in the prospectus summary of registration statements. These disclosures include sponsor compensation, conflicts of interest, dilution, runway to complete a de-SPAC transaction, and others.

Sponsors – Item 1603

According to the final rules, registrants will now be required to provide further information about the SPAC’s sponsors, affiliates, and promoters. This disclosure must include the name, form of organization, and general character of the SPAC’s sponsor’s business.

Conflicts of interest – Item 1603

Under Item 1603(b), registered offerings by SPACs and in de-SPAC transactions will require disclosure of any actual or potential material conflicts of interest. This requirement applies to any conflict of interest that may arise in a company’s determination of whether to proceed with a de-SPAC transaction or if one may arise because of the manner the SPAC compensates its directors and officers. Each director and officer will also now be required to disclose the fiduciary duty each owes to other companies.

Dilution – Items 1602(a)(4), (c); 1604(a)(3), (b)(5), (b)(6), (c)

The new amendment will require all SPAC registration statements other than for a de-SPAC transaction to include a description of all material potential sources of dilution following a SPAC IPO per Item 1602(c). Registrants will also be required to provide a tabular disclosure of possible redemption scenarios of the amount and offering price, the nature and amounts of each source of dilution used to determine the net tangible book value per share, as adjusted, and any adjustments made to the number of shares used when determining the per-share component of net tangible book value per share, as adjusted.

De-SPAC transaction background – Item 1605

De-SPAC transactions will now require further disclosure of certain information in plain English on the cover page of the prospectus or proxy. Registrants must now disclose the background, material terms, and effects of the transaction. The summary of the background of the de-SPAC transaction must include a description of “contacts, negotiations, or transactions that have occurred concerning the de-SPAC transaction.”

Board determination about de-SPAC transactions – Item 1606

Additional disclosure is required in de-SPAC transactions involving any determination by a board of directors or management on whether the de-SPAC transaction is advisable and in the best interests of the SPAC and its shareholders.

Reports, opinions, appraisals, and negotiations – Item 1607

Registrants must also disclose any external report, opinion, or third-party appraisal received by the SPAC or SPAC sponsor and projections relating to the SPAC or target company that were disclosed in filings in connection with the de-SPAC transaction.

Enhanced projections disclosure – Item 1609

The company is required to disclose the purpose of the projections disclosed in the filing and the party that prepared the projections, the material bases, all material assumptions, any factors impacting those assumptions, and whether the projections reflect the view of the board of directors or management of the SPAC or target company.

Structured data requirement – Item 1610

SPACs are required to tag all information disclosed pursuant to Subpart 1600 of Regulation S-K in Inline XBRL once the new amendments come into effect.

Disclosures and Liability in De-SPAC Transactions

In light of the increased reliance on de-SPAC transactions for private operating companies to access the U.S. securities markets, the SEC adopted rules and amendments to more closely align the treatment of private companies entering the public markets through de-SPAC transactions with that of companies conducting traditional IPOs.

Nonfinancial disclosures

If target companies in de-SPAC transactions are not subject to the reporting requirements of Section 13(a) or 15(d) of the Exchange Act, target company disclosure would be required in the registration statements or schedules filed in connection with the de-SPAC transactions.

Minimum dissemination period

Prospectuses, proxies, or information statements filed in connection with de-SPAC transactions are required to be distributed to shareholders at least 20 calendar days before a shareholder meeting, or the maximum period permitted by governing law.

Private operating company as co-registrant

The target company in a de-SPAC transaction will be considered a registrant and required to appear on the cover page and sign the registration statement filed in connection with the transaction so that the target company will be subject to liability.

Redetermination of smaller reporting company status

Following the closing of a de-SPAC transaction, the combined company is required to reevaluate its smaller reporting company status and to reflect the redetermination of status in any filing made 45 days after the closing.

Private Securities Litigation Reform Act of 1995 safe harbor

“Blank check company” is now defined to include SPACs, which makes the safe harbor under the Private Securities Litigation Reform Act unavailable to SPACs. The SEC noted that the determination of whether a SPAC is an “investment company” depends on many factors and is duration-sensitive, so it will continue to be determined on a case-by-case basis.

Business Combinations Involving Shell Companies

Rule 145a

The new rules provide that any business combination of a reporting shell company (except for a business combination related shell company) involving another entity that is not a shell company is deemed to involve a “sale” of securities within the meaning of Section 2(a)(3) of the Securities Act.

Financial statement requirements – Article 15 of Regulation S-X

The requirements under new Article 15 of Regulation S-X are designed to make the financial statement requirements in de-SPAC transactions more similar to those required in a traditional IPO.

Enhanced Projections

Items 10(b) and Item 1609 of Regulation S-K Item

10(b) applies to a target company’s projections when presented to investors through the registrant’s filings and is revised to include:

- Any projected measures not based on historical financial results or operational history should be clearly distinguished from project measures based on historical financial results or operational history.

- Generally, it is misleading to present projections based on historical financial results or operational history without presenting those results or operational history with equal or greater prominence.

- Projections that include non-GAAP measures should include a definition of the measure, a description of the most closely related GAAP measure, and an explanation of why the non-GAAP measure was used instead.

Item 1609 of Regulation S-K requires enhanced disclosure requirements related to projections in de-SPAC transactions, including information about the material bases of those projections and the underlying material assumptions.

Status of SPACs Under the Investment Company Act

Depending on the facts and circumstances, a SPAC may meet the definition of “investment company” under Section 3(a)(1)(A) or (C) of the Investment Company Act, which would require the company’s compliance with the Act.

Next Steps

The final rules will become effective 125 days after the rules are published in the Federal Register. Companies will have 490 days after publication to comply with the structured data requirement.

To best prepare for the new rules, companies should:

- Review disclosure controls and procedures to ensure that they comply with the enhanced SPAC and de-SPAC disclosure.

- Plan to make public more enhanced disclosures than previous SPAC IPOs and de-SPAC transactions.

- Understand the enhanced requirements for target companies in a de-SPAC transaction to become a co-registrant with the SPAC and therefore assume responsibility for disclosures in the registration statement.

- Review the SEC guidance to determine whether their SPAC is an investment company and therefore must comply with the Investment Company Act.

Download PDF of Advisory

[View source.]