Key Takeaways

- On March 6, the Securities and Exchange Commission (SEC) adopted final rules in Release No. 33-11275 (Final Rules) requiring registrants to disclose certain climate-related information in registration statements and annual reports, including with respect to governance; the material impacts of climate-related risks on business, strategy, outlook and financial statements; risk management processes and mitigation; and climate targets and goals.

- The Final Rules require the disclosure of Scope 1 emissions and Scope 2 greenhouse gas (GHG) emissions metrics by large accelerated and accelerated filers, on a phased-in basis, if such emissions are material. Non-accelerated filers, including smaller reporting companies and emerging growth companies, will not be required to report on Scope 1 or 2 GHG emissions.

- Only large accelerated filers will phase in to filing independent attestation reports regarding Scopes 1 and 2 GHG emissions disclosures at the reasonable assurance level, and accelerated filers will only need to provide limited assurance.

- New financial footnote disclosure is required (1) when severe weather or other natural occurrences are a significant contributing factor in incurring a capitalized cost, expenditure expensed, charge, loss or recovery reflected on the registrant’s income statement or balance sheet and (2) when carbon offsets or renewable energy credits (RECs) are included in a registrant’s disclosed climate-related targets or goals.

- The Final Rules scale back rules proposed by the SEC, notably by (1) eliminating Scope 3 GHG emissions reporting, (2) generally conditioning disclosures on materiality, and (3) eliminating the requirement to report material changes to climate-related disclosures on Form 10-Q.

- Compliance phases in first for large accelerated filers from 2025 through 2033, then for accelerated filers from 2026 through 2031, and then to a limited degree for other filers from 2027 through 2028.

- An administrative stay order granted by the Fifth Circuit Court of Appeals briefly stayed the Final Rules as of March 15, pending appeal in Liberty Energy v. SEC, No. 24-60109, and attorneys general from more than 10 states have filed petitions in the Sixth and 11th Circuit Courts of Appeals seeking that the Final Rules be declared unlawful on both procedural and substantive grounds.

- The Fifth Circuit’s administrative stay was dissolved on March 22 in consideration of a consolidation order issued by the U.S. Judicial Panel on Multidistrict Litigation (MCP No. 180), which randomly selected the Eighth Circuit Court of Appeals in which to consolidate nationwide petitions to review the Final Rules, including those mentioned in this client alert. On March 26, Liberty Energy requested that the Eighth Circuit reinstate the prior administrative stay during pendency of the consolidated petitions to review the Final Rules.

- The Final Rules are slated to become effective on May 27, 2024.

Overview

Nearly two years after the SEC released proposed rules regarding the standardization of climate-related disclosures, and after more than 24,000 public comments, the SEC adopted the Final Rules by a 3-2 vote on March 6. The Final Rules add a new Subpart 1500 to Regulation S-K and Article 14 to Regulation S-X and reflect a few notable differences from the proposed rules.

How the Final Rules Differ from the Proposed Rules

- Disclosures are generally less prescriptive than in the proposed rules (e.g., climate-related risks, board oversight, risk management, etc.).

- Climate-related disclosures are further qualified based on materiality (e.g., impacts of climate-related risks, use of scenario analysis, maintenance of an internal carbon price, etc.).

- Disclosure of Scopes 1 and 2 GHG emissions are limited to large accelerated and accelerated filers (i.e., not required for non-accelerated filers), following an extended phase-in, only when material, and with the ability to provide disclosure on a delayed basis.

- Assurance levels covering Scopes 1 and 2 for accelerated filers are scaled back to limited assurance, and large accelerated filers will have an extended phase-in period before being required to provide reasonable assurance.

- Scope 3 GHG emissions disclosures are not required.

- No description of a board members’ climate expertise will be required.

- The proposed requirement to disclose the impact of severe weather events and other natural occurrences on each line item of the financial statements has been replaced by more discrete financial footnotes disclosures for specific impacts exceeding 1% of the registrant’s income for the relevant period.

- Material disclosure requirements for strategy, transition plans, and targets and goals have been moved from Regulation S-X to Regulation S-K.

- The safe harbor from private liability for forward-looking statements has been extended to transition plans, scenario analysis, internal carbon pricing, and targets and goals.

- The proposed requirement for a private company party to a business combination registered on Form S-4 or F-4 to provide disclosures was excluded from the Final Rules.

- The proposed requirement to provide material changes to climate-related disclosures in quarterly reports was not included in the Final Rules.

Summary of Final Rules

Domestic registrants must present climate-related information required under Regulation S-K, including GHG emissions, in Item 6 of Form 10-K, or in another appropriate section of the filing (e.g., risk factors, MD&A, etc.). Foreign private issuers must present it in a new Item 3.E of Form 20-F. All registrants will need to disclose material impacts of severe weather events or other natural occurrences under Regulation S-X in footnotes to the financial statements, subject to certain thresholds.

The Final Rules will generally require all registrants to disclose the following:

- Oversight of climate-related risks by the board of directors as well as management’s role in assessing and managing such material risks.

- Climate-related risks that have materially impacted, or are reasonably likely to have a material impact on, the registrant, its strategy, results of operations or financial condition, addressing whether they are physical or transition risks and the actual and potential impacts, any transition plans, and any material use of internal carbon pricing to manage such risks.

- Processes for identifying, assessing and managing material climate-related risks.

- Climate-related targets or goals that are material to the registrant’s business, financial condition, or operational results, as well as associated use of carbon offsets or RECs.

- Financial footnote disclosures, when severe weather events or other natural occurrences are a significant contributing factor impacting the registrant’s income statement or balance sheet by more than 1% of income for the relevant period.

Large accelerated and accelerated filers that are not smaller reporting companies or emerging growth companies will disclose their Scope 1 and Scope 2 GHG emissions, to the extent material, accompanied by an independent attestation providing limited or reasonable assurance about such GHG emissions disclosures. Annual reports and registration statements filed by such larger registrants will include an attestation report issued by an independent GHG emissions attestation provider. After phase-in of the Final Rules, attestation reports must provide limited assurance regarding the accuracy of an accelerated filer’s GHG emissions disclosures, and they must provide reasonable assurance for a large accelerated filer’s GHG emissions reporting.

Generally Applicable Climate-Related Disclosures (Items 1500-1504 of Regulation S-K)

The Final Rules provide definitions in a new Item 1500 that applies to both new Article 14 of Regulation S-X and new Subpart 1500 of Regulation S-K. Certain items of new Subpart 1500 to Regulation S-K will apply to all registrants, including non-accelerated filers such as smaller reporting companies and emerging growth companies.

Climate-Related Governance Disclosures (Item 1501)

All registrants will disclose the board’s oversight of climate-related risks, identifying any board committee with such responsibility and describing the processes by which the board or such committee is informed about such risks. If there is a climate-related target or goal disclosed pursuant to Item 1504 or transition plan disclosed pursuant to Item 1502, the registrant will also need to describe whether and how the board oversees progress against the target or goal or transition plan. In addition, all registrants will disclose management’s role in assessing and managing material climate-related risks.

Registrants will need to make clear which management positions are responsible for such activities and the relevant expertise of the individuals in these roles and the processes involved. Such disclosure could include internal reporting structures for climate-related disclosures that the registrant may have in place (e.g., a climate-risk committee reporting to the full board or an employee group reporting to an executive), including the nature and frequency of that reporting.

Climate-Related Strategy Disclosure (Item 1502)

All registrants will need to provide a discussion of any climate-related risks that have materially impacted or are reasonably likely to have a material impact on the registrant, identifying particularized climate-related risks both in the short and long term, whether such risks are physical or transition risks, and future details on the nature of such risks. The discussion must also address specifically how such risks have impacted or may impact the registrant’s strategy, results of operations, financial condition, business model and outlook, including any mitigation activities or adaptations, such as new technologies or processes, and whether and how the registrant considers these impacts in planning and capital allocation. For any mitigation or adaptation activities, the registrant must further describe quantitatively and qualitatively the material expenditures incurred and material impacts on financial estimates and assumptions that directly result from these activities.

If a registrant has adopted a transition plan to manage a material transition risk, the registrant must describe this plan along with providing (1) updated information each year to describe any actions taken during the year under the plan, including how such actions have impacted the registrant’s business, results of operations or financial condition, and (2) quantitative and qualitative disclosures of material expenditures incurred and material impacts on financial estimates and assumptions as a direct result of the transition plan.

Certain information about any scenario analysis or internal carbon price used to assess or manage a material climate-related risk must also be disclosed.

Climate-Related Risk Management Disclosures (Item 1503)

The Final Rules call for a detailed discussion of a registrant’s processes for identifying, assessing and managing material climate-related risks. The discussion should explain how a registrant identifies such risks, assesses their materiality, prioritizes them among various other risks, decides whether to mitigate, offsets or otherwise addresses the risks and whether and how any of these processes have been integrated into the registrant’s overall risk management system.

Climate-Related Targets and Goals (Item 1504)

Disclosure of the registrant’s climate-related targets and goals is required under the Final Rules when such targets or goals have materially impacted or are reasonably likely to have a material impact on the registrant’s business, results of operation, or financial condition. This disclosure may be incorporated into the strategy and risk management disclosures required under Items 1502 and 1503 discussed above and includes actions such as conservation of energy or water, and use of low-carbon products. A registrant’s disclosure of a target or goal that includes carbon offsets or RECs will trigger the separate financial footnote disclosures discussed below.

The disclosure about targets and goals must discuss information necessary to understand the actual or potential material impact, including the following as applicable:

- Scope of activities included in the target.

- Baseline for assessment and how it will be tracked.

- How goals are intended to be met.

Registrants will need to disclose progress made and actions taken toward interim or ultimate goals, with annual updates, including (1) any material impacts to the registrant’s business, results of operations, or financial condition and (2) quantitative and qualitative disclosure of any material expenditures and material impacts on financial estimates and assumptions as a direct result of the target or goal or the actions taken.

Finally, this item also requires information about carbon offsets and RECs if they are used as a material component of the registrant’s plan to achieve disclosed targets or goals.

Climate-Related Disclosures Only for Larger Filers (Items 1505-1506 of Regulation S-K)

Unlike the disclosures discussed above, which apply to all registrants, disclosure about Scopes 1 and 2 GHG emissions apply only to large accelerated and accelerated filers, and only if such filers deem such information to be material. The SEC indicated in the adopting release for the Final Rules that materiality should be determined not merely by the amount of the emissions but by a consideration of whether a reasonable investor would consider disclosure of the information important when making an investment or voting decision. For example, factors that may weigh in favor of materiality could include a company’s expected additional regulatory burdens or penalties for complying with reporting requirements in various jurisdictions or whether they reflect progress toward achieving a target or goal or a transition plan that is to be disclosed under the Final Rules. This Scope 1 and 2 information will be required for the registrant’s most recently completed fiscal year and, to the extent previously disclosed in an SEC filing, for the historical fiscal year(s) included in the consolidated financial statements in the filing. Non-accelerated filers need not provide such disclosures, but a non-accelerated filer that expects to become an accelerated filer should prepare for becoming subject to additional GHG emission reporting requirements.

Scopes 1 and 2 GHG Emissions Disclosures (Item 1505)

Large accelerated and accelerated filers will disclose material Scope 1 and Scope 2 GHG emissions on a carbon dioxide equivalent (CO2e) basis. Because the Final Rules define GHG as the total of seven different greenhouse gases,[1] those seven gases should be tracked pursuant to internal reporting controls and procedures. Such gases can be reported in the aggregate if the sum is material on a CO2e basis, but specific gases must be reported separately to the extent individually material. Emissions from manure management systems receiving federal funds are excluded from reportable GHG emissions.

Scopes 1 and 2 GHG emissions will be disclosed on a gross basis before considering offsets. Scope 1 emissions are direct GHG emissions from operations owned or controlled by the registrant, which the Final Rules refer to as its organizational boundaries. Scope 2 emissions are indirect GHG emissions from the generation of purchased or acquired electricity, steam, heat or cooling consumed within the registrant’s organization boundaries.

The emissions information must be accompanied by a description of the methodology, significant inputs and significant assumptions used to calculate such emissions. A registrant may use reasonable estimates so long as it also describes the underlying assumptions and its reasons for using the estimates.

Attestation of Scope 1 and Scope 2 Emissions Disclosure (Item 1506)

Following a phase-in period discussed below, the Final Rules require large accelerated and accelerated filers to provide an attestation covering their Scope 1 and Scope 2 emissions disclosures. An attestation report will need to be provided by an independent expert qualified in GHG emissions, and the report must make specific statements that can carry liability for misstatements. After a further phase-in period, the attestation’s reliability level will increase from limited assurance to reasonable assurance for large accelerated filers only (as shown in the table about compliance dates below). Limited assurance corresponds with the current treatment of unaudited (reviewed) financial statements, and reasonable assurance corresponds with the current treatment of audited financial statements.

Financial Footnote Disclosures (Article 14 of Regulation S-X)

New Article 14 of Regulation S-X will require financial footnote disclosures about how a registrant’s financial statements were impacted by severe weather events or other natural occurrences (e.g., hurricanes, tornadoes, flooding, drought, wildfires, extreme temperatures, sea level rise, etc.), including (1) expenditures expensed as incurred and losses resulting from severe weather events and other natural conditions, (2) capitalized costs and charges resulting from severe weather events and other natural conditions, (3) certain disclosures regarding recoveries, and (4) financial estimates and assumptions materially impacted by severe weather events and other natural conditions or disclosed targets or transition plans.

The thresholds for providing these disclosures are as follows:

- Attribution: Severe weather or other natural occurrences were a significant contributing factor to the registrant incurring a capitalized cost, expenditure expensed, charge, loss or recovery.

- Expensed Costs: Expenditures expensed as incurred and losses, excluding recoveries, incurred during the fiscal year as a result of such events or conditions if the aggregate amount of such expenditures and losses equals or exceeds 1% of the absolute value of income or loss before income tax expense or benefit for the relevant fiscal year, unless the aggregate amount of such expenditures and losses for the relevant year is less than $100,000.

- Capitalized Costs: Capitalized costs and charges, excluding recoveries, incurred during the fiscal year as a result of such events or conditions if the aggregate amount of the absolute value of such capitalized costs and charges recognized equals or exceeds 1% of the absolute value of stockholders’ equity or deficit at the end of the relevant fiscal year, unless the aggregate amount of the absolute value of such capitalized costs and charges for the relevant year is less than $500,000.

In addition, if carbon offsets and RECs have been used as a material component of the registrant’s plans to achieve its disclosed climate-related targets or goals, disclosure is required of (1) the aggregate amount of carbon offsets and RECs expensed, (2) the aggregate amount of capitalized carbon offsets and RECs recognized, (3) the aggregate amount of losses incurred on the capitalized carbon offsets and RECs, during the fiscal year, and (4) the beginning and ending balances of capitalized carbon offsets and RECs on the balance sheet for the fiscal year.

Contextual information is to be provided regarding policy decisions, inputs, assumptions and judgments involved in presenting financial statement impacts to further the understanding of the financial statement impacts.

Notably, placing this climate-related information in footnotes to the financial statements subjects it to auditor review.

Applicability and Timing of Disclosures

All domestic and foreign registrants, except for asset-backed issuers, must provide the disclosures required by the Final Rules. Smaller reporting companies, emerging growth companies and other non-accelerated filers are exempt from the Scope 1 and Scope 2 GHG emissions disclosures, as well as from providing related attestations, but they must provide all other disclosures.

Registrants must generally provide climate-related disclosures in annual reports at the time of filing, but such disclosures may be provided on a delayed basis. They may be incorporated by reference to a quarterly report for the second-quarter report of the year after that to which the emissions disclosures relate or by filing an amended annual report before such second-quarter report becomes due. Registration statements must disclose any required GHG emissions for the fiscal year most recently completed as of 225 days before effectiveness of the registration statement. Climate-related disclosures under Regulation S-X must also cover the same historical period for which consolidated audited financial statements are included in the filing. It is important to note that the Final Rules supplement and do not limit information, including financial statements, that are otherwise required by the form in question (e.g., Form 10-K, Form S-1).

All filers will need to ensure that the customary interactive iXBRL data is present for all climate-related disclosures in the same way that currently applies to SEC filings generally.

The Final Rules include safe harbor protection for certain disclosures other than historic facts regarding transition plans, scenario analysis, internal carbon pricing, targets and goals. Additionally, certain other disclosures and statements may fall within the definition of “forward-looking statement” and thus receive safe harbor protection.

Phase-in Periods

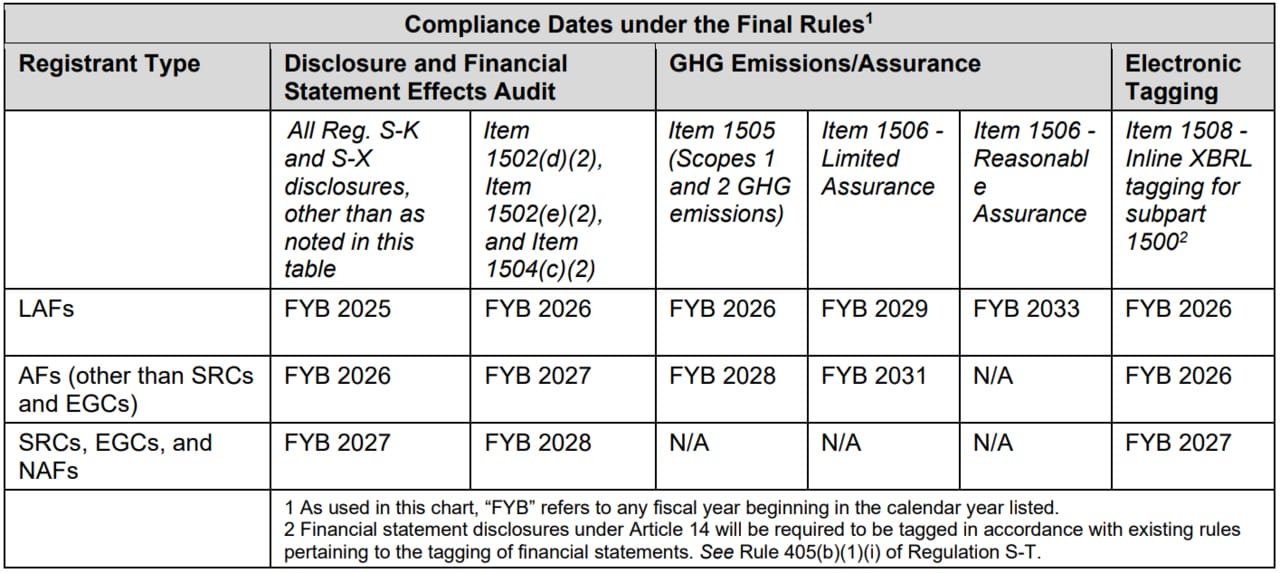

Compliance dates for the Final Rules phase in depending on the registrant’s filer status, as shown below:

SEC Fact Sheet – The Enhancement and Standardization of Climate-Related Disclosures: Final Rules

As shown above, the Final Rules begin to apply to large accelerated filers, accelerated filers and non-accelerated filers in 2025, 2026 and 2027, respectively. The first compliance year for each filer type (first column in the chart above) will require compliance with all portions of the Final Rule other than items that are subject to phase-in. The second compliance year for each filer type (second column in chart above) will require disclosure of material expenditures for activities and plans to mitigate or adapt to climate-related risks, as well as disclosure of expenditures on targets, goals and related activities. Large accelerated filers will also start reporting Scopes 1 and 2 GHG emissions, if material, in their second compliance year. Nothing further phases in after the second compliance year of 2027 for non-accelerated filers. Accelerated filers will begin reporting material Scopes 1 and 2 GHG emissions in their third compliance year of 2028. Limited assurance attestations will not be required until three years after Scopes 1 and 2 become required. For large accelerated filers only, reasonable assurance regarding Scopes 1 and 2 GHG emissions must be provided starting in 2033. Accelerated filers are not required to provide reasonable assurance.

Challenges to the Final Rules

The Final Rules were promptly challenged by 10 states (West Virginia, Alabama, Alaska, Georgia, Indiana, New Hampshire, Oklahoma, South Carolina, Virginia and Wyoming) in the U.S. Court of Appeals for the 11th Circuit on the same day the Final Rules were released. The 10 states, led by West Virginia, filed a petition seeking to have the court declare the Final Rules unlawful and find that the SEC exceeded its statutory rulemaking authority. In a similar case before the Fifth Circuit Court of Appeals, Liberty Energy v. SEC, the court granted per curiam an administrative stay of the Final Rules on March 15. The Fifth Circuit dissolved its stay on March 22, in consideration of an order by the U.S. Judicial Panel on Multidistrict Litigation, which randomly consolidated nationwide petitions for review of the Final Rules into the U.S. Court of Appeals for the Eighth Circuit. On March 26, Liberty Energy requested that the Eighth Circuit reinstate the administrative stay while it reviews petitions regarding the Final Rules.

While not directly cited, the so-called major questions doctrine may provide a basis for challenge to the Final Rules under the 2022 Supreme Court decision in West Virginia v. EPA, which was initiated by the same attorney general currently challenging the Final Rules with nine other attorneys general. SEC Commissioner Mark T. Uyeda expressed his concerns about the major questions doctrine in his dissenting statement to the Final Rules, asserting that the SEC has not cited a clear congressional authorization for its authority to promulgate the Final Rules. He also notes that the Final Rules were not in their current form reproposed and subject to public comment. The House Financial Services Committee is separately set to hold two hearings on the impact of the Final Rules on March 18 and April 10.

What to Expect Going Forward

The Final Rules are expected to prompt conversations in boardrooms and among executives at public companies throughout the United States and beyond. While reporting companies have for years been involved in establishing and enforcing policies, controls and procedures to help ensure the accuracy of SEC reporting, these processes will now need to be further extended to gather and report reliable climate-related information. Reporting companies should plan to integrate climate-related disclosures into disclosure and risk management processes as well as materiality assessments. These efforts are expected to involve a significant increase in costs and lead to expanded use of climate-related board and management committees and greater consideration of the regulatory burdens associated with steps a company may take to address climate-related risks and impacts.

Advance planning will be instrumental to companies navigating these rules, both directly through their application and indirectly by efficiently working with auditors and attestation providers to ensure compliance with the Final Rules.

[1] Those seven GHGs are (i) carbon dioxide, (ii) methane, (iii) nitrous oxide, (iv) nitrogen trifluoride, (v) hydrofluorocarbons, (vi) perfluorocarbons, and (vii) sulfur hexafluoride.

[View source.]