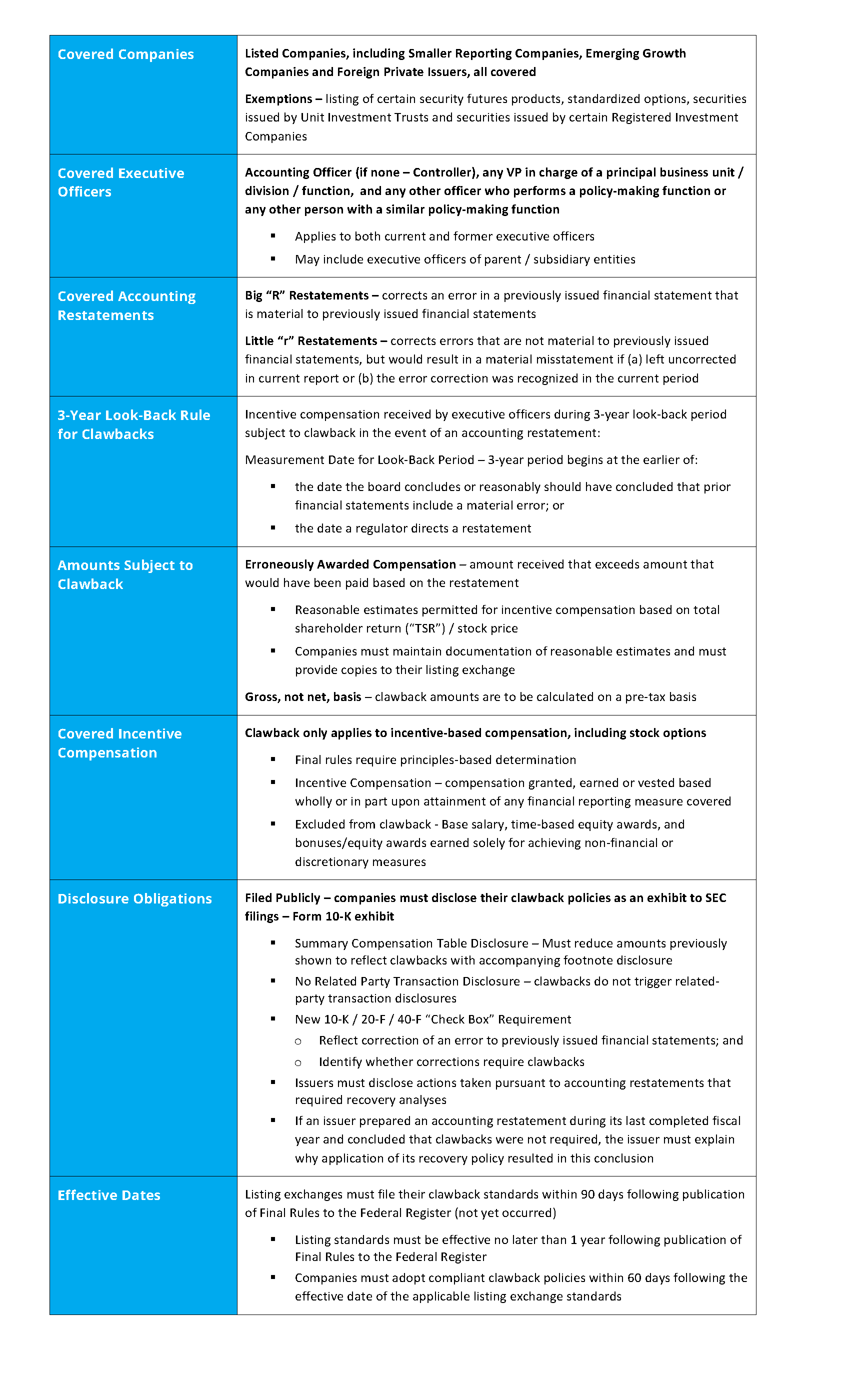

On October 26, 2022, the Securities and Exchange Commission (“SEC”) adopted its final “clawback” rules requiring securities exchanges to mandate listing standards that require listed issuers on securities exchanges (“Issuers”) to implement a policy providing for the recovery of erroneously awarded incentive-based compensation under certain circumstances (the “Final Rules”).

The Final Rules require Issuers to adopt and enforce a compensation recovery policy that will: require recovery of incentive-based compensation from executive officers when an accounting restatement due to the material non-compliance with any financial reporting requirement under the securities laws is required. The Final Rules use a 3-year look-back period and specific disclosure requirements, including the filing of the policy with the issuer’s Annual Report on Form 10-K.

Under the Final Rules, an Issuer would be subject to delisting if it does not adopt and comply with its compensation recovery policy. The Final Rules apply to virtually all Issuers, including emerging growth companies (“EGCs”), smaller reporting companies (“SRCs”), foreign private issuers (“FPIs”), and controlled companies.

The Final Rules are found in new Rule 10D-1 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”). The Final Rules set forth the directive that exchanges and associations listing securities establish standards that Issuers need to meet with respect to clawback policies.

Summary of Final SEC Clawback Rules

Disclosure of Issuer’s Policy on Recovery of Incentive-Based Compensation

The Final Rules direct national securities exchanges and associations to establish listing standards that require an Issuer to:

- adopt and comply with a written policy for recovery of erroneously awarded incentive-based compensation, as described in this advisory; and

- disclose the compensation recovery policy in accordance with SEC rules, including providing the information in tagged data format (Inline XBRL).

The Final Rules require (i) specific disclosure of the Issuer’s policy on recovery of incentive-based compensation and information about actions taken pursuant to such recovery policy, (ii) the policy be filed as an exhibit to the Issuer’s Annual Report on Form 10-K (new Exhibit 97), and (iii) new check boxes on Form 10-K indicating whether the financial statements included in such filings reflect correction of an error to previously issued financial statements and whether any of those corrections give rise to a recovery analysis.

Definition of Executive Officers

The Final Rules define “executive officer” as an Issuer’s president, principal financial officer, and principal accounting officer (or if there is no such accounting officer, the controller), any vice-president of the issuer in charge of a principal business unit, division, or function, any other officer who performs a policy-making function, or any other person who performs similar policy-making functions for the issuer, which is consistent with the term “officer” as defined in Rule 16a-1(f). The Final Rules are not intended to cover rank-and-file employees; the intent was to include persons who were responsible for the errors necessitating the accounting restatement.

Restatements Triggering Recovery Policy

The Final Rules cover both types of restatements:

- Those that correct errors that are material to previously issued financials (“Big R” restatements); and

- Those that correct errors that are not material to previously issued financials, but would result in a material misstatement if: (a) the errors were left uncorrected in the current period or (b) the error correction was recognized in the current period (“little r” restatements).

The SEC acknowledged that a correction of an error that is recorded in the current financials where the error is immaterial to both the previous and current financials, an “out-of-period adjustment,” would not constitute an accounting restatement.

Incentive-Based Compensation

For purposes of Rule 10D-1, the Final Rules define “incentive-based compensation” to be “any compensation that is granted, earned, or vested based wholly or in part upon the attainment of any financial reporting measure.”

Specific examples of award types that could constitute “incentive-based compensation” include, but are not limited to:

- Non-equity incentive plan awards;

- Bonuses;

- Other cash awards

- Restricted stock, restricted stock units, performance share units, stock options, and stock appreciation rights (“SARs”); and

- Proceeds received upon the sale of shares acquired through an incentive plan that were granted or vested based wholly or in part on satisfying a financial reporting measure performance goal.

Calculating 3-Year Lookback Period

The 3-year look-back period for the recovery policy will consist of the three completed fiscal years immediately preceding the date the Issuer is required to prepare an accounting restatement for a given reporting period. Under the listing standards, the date on which an Issuer is required to prepare an accounting restatement is the earlier to occur of:

- The date the Issuer’s board of directors, a committee of the board of directors, or the officer or officers of the issuer authorized to take such action if board action is not required, concludes, or reasonably should have concluded, that the issuer is required to prepare an accounting restatement due to the material noncompliance of the issuer with any financial reporting requirement under the securities laws as described in the Final Rules; or

- The date a court, regulator or other legally authorized body directs the issuer to prepare an accounting restatement.

Calculation of Erroneously Awarded Compensation; Board Discretion

The erroneously awarded compensation under an Issuer’s recovery policy is “the amount of incentive-based compensation received by the executive officer or former executive officer that exceeds the amount of incentive-based compensation that otherwise would have been received had it been determined based on the accounting restatement,” computed without regard to taxes paid. Such incentive-based compensation may be in the form of cash or equity awards. The Final Rules provide guidance about calculating the recoverable amounts.

The Final Rules provide boards with limited discretion, subject to certain reasonable restrictions, regarding the calculation of the amount to be recovered and the means of recovery; however, the Final Rules do not permit boards to settle for less than the full recovery amount unless they satisfy the conditions that demonstrate recovery is impracticable. The Final Rules provide circumstances under which recovery could be impracticable.

Effective Dates

The Final Rules will become effective 60 days following publication of the adopting release (available

here) in the Federal Register.

Exchanges will be required to file proposed listing standards no later than 90 days following publication of the release in the Federal Register, and the listing standards must be effective no later than one year following such publication.

Issuers subject to such listing standards will be required to adopt a recovery policy no later than 60 days following the date on which the applicable listing standards become effective.

[View source.]