[co-author: Stephanie Dellosa]

Persisting political and economic uncertainty means awareness of market changes remains crucial.

The 2008 distress cycle triggered defaults and restructurings for European PE portfolio companies, as maintenance covenant defaults and balance sheet deleveraging forced refinancings and debt-for-equity swaps. While restructuring conditions for PE firms are stronger in 2019 than they were in 2008, persisting political and economic uncertainty means that awareness of market developments remains important.

Permissive Intercreditor Arrangements Impact Schemes of Arrangement

UK loan document developments have made new and more flexible tools available for sponsors to effect debtor-led restructuring processes. In response to the 2008 crisis and a sponsor-driven market, we have begun to see increasingly accommodative intercreditor documentation, reducing the need for court-sanctioned schemes of arrangement in restructuring deals. Previously, a scheme of arrangement (requiring the support of 75% in value and a simple majority in number of affected classes, e.g., lenders) was needed to restructure a company’s debt, where unanimous consent of lenders was not possible. It is now common for intercreditor agreement terms to circumvent the need for a scheme of arrangement and, therefore, the court process for certain forms of restructuring, including debt-for- equity swaps. This allows restructurings to be effected contractually with lower levels of support, such as a simple majority. In our view, this positive development for private equity firms allows portfolio companies to more easily reach agreement with lenders and effect quicker, more cost-effective, and private restructurings.

Click for larger image.

Risk of Litigation and Contentious Restructurings Is Heightened

Other loan document developments, such as the prevalence of incurrence covenants, and the combination of English law and New York law agreements in single structures, may increase the potential for disputes between lenders and borrowers. In our view, an economic downturn may lead to more complex and litigious workouts. As lenders have increasingly limited rights to control borrower and sponsor actions, we anticipate more US-style litigation in both US and UK courts, as lenders seek to assert their remaining rights against borrowers and different ranking lender groups. Firms need to be mindful of growing US influence (both US law documentation and US lenders) as these new debt structures are stress tested.

Cov-Lite Freedom Comes With Costs

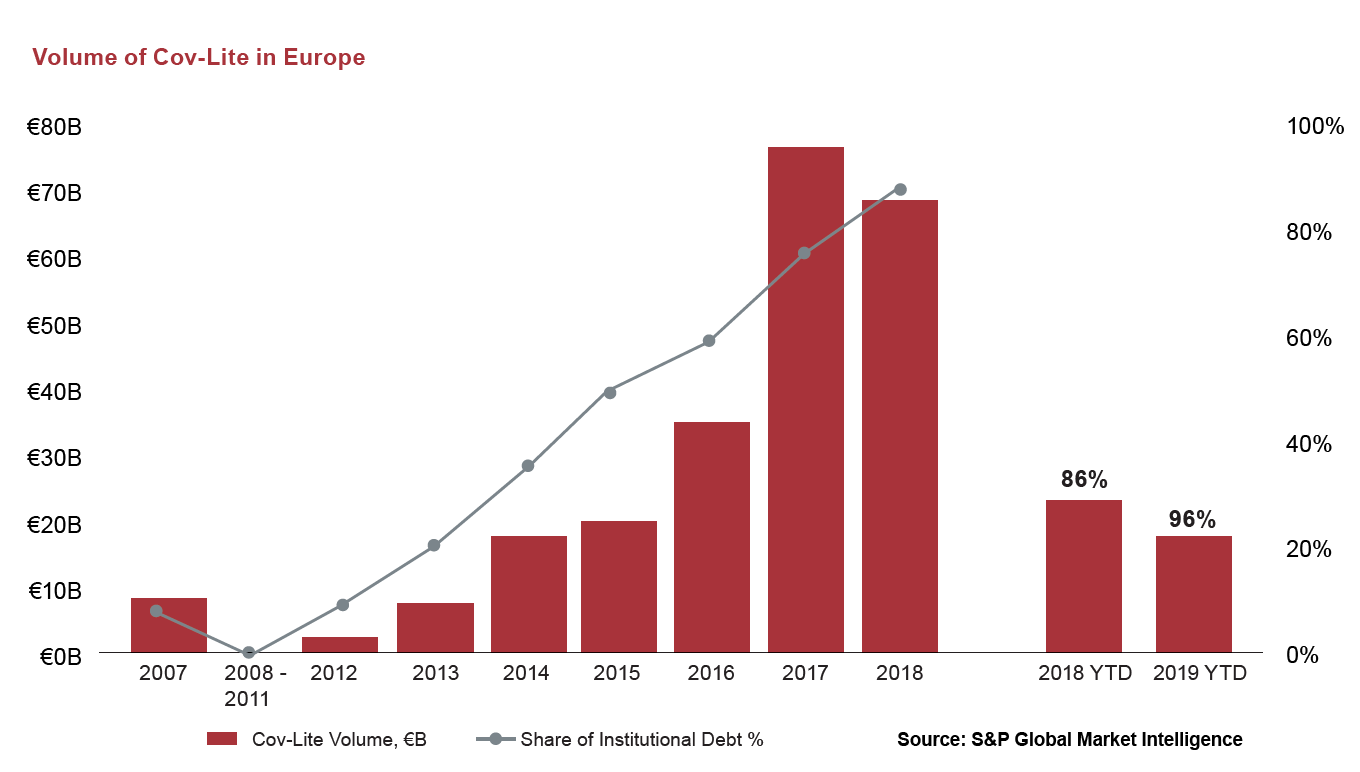

The cov-lite environment continues to favour financial sponsors, with covenant erosion an ongoing European loan market theme. In the first three months of 2019, roughly 96% of institutional volumes in Europe were completed on a cov-lite basis, compared with almost nil in 2008. European debt instruments now allow great flexibility for additional debt incurrence and rarely include maintenance covenants, amongst other features. We expect a flatter, longer default cycle in the case of any economic downturn, with fewer restructurings in total compared to the 2008 crisis. However, while the lack of covenants means the default rate is unlikely to rise in the near term, allied with the erosion of protections, if and when stakeholders are brought to the table, the residual value in the business may be diminished, heightening the risk of litigation, contentious restructurings, and formal insolvency.

Click for larger image.

Legislative Changes Are on the Horizon

Contemplated legal developments could further change the European restructuring landscape. The UK government is exploring introducing chapter 11-style bankruptcy laws, which would see the UK become more borrower-friendly, with increased flexibility for companies to work out problems. The EU is proposing similar changes for the insolvency laws of its member states. Separately, in the wake of high-profile business collapses such as BHS, the UK Department of Business, Energy & Industrial Strategy has proposed changes to make holding company directors liable in the sale of businesses that enter insolvency within a set period after the sale. Where there is a sale of a business with a heightened risk of insolvency, sponsor-appointed directors should assess the risk of personal liability and seek legal advice.