A fundamental principle of sports competition is bringing your best self to the playing field. That principle applies equally to life outside of sports, and although Charles Barkley famously declared himself to be no role model, fame gives athletes a unique platform to give back to their communities, to inspire, and to help others become their best selves.

This influence takes many forms—social media commentary, endorsements, daily life choices, and so on. And, although many high-profile athletes have chosen to form nonprofit organizations, there are many options for those who wish to take a different approach to giving back. This article highlights some of these options. Later articles will explore the process of forming and operating a nonprofit organization and alternative structures for funding charitable programs across national borders.

Cash and Non-Cash Donations to Existing Charity

Charities, hospitals, and other nonprofit organizations are usually happy to accept cash donations from the philanthropically inclined. Those with a public following can sometimes also use their status to create awareness of a particular organization or cause, give in-kind donations of memorabilia (for auction, for example), or give a combination (for example, giving matching donations and dinner with the highest donor).

Restricted and Donor Advised Funds

If an unrestricted gift to an existing charity doesn’t quite fit the bill, donors can make the same (or similar) donations with “strings attached” by making a donation for a specific purpose. Such “restricted” donations are popular options for funding scholarships or similar programs. A similar concept is a “donor advised fund,” where a donor makes a donation but can make ongoing recommendations for how the organization uses the donation. Donor advised funds are very popular among wealthy philanthropists that want to direct their giving in the same (or similar) manner as they direct their investments.

Fiscal Sponsorship

In some cases, acting as a passive “donor” is not enough, but forming and operating a nonprofit organization is overwhelming or inappropriate. In those cases, a fiscal sponsorship may be the right approach. A fiscal sponsorship is essentially the “light version” of forming a nonprofit organization. It is a contractual relationship with an existing charity, under which the charity acts as the “sponsor” of a program. Fiscal sponsorships exist in many forms, including charity “incubator” programs and charity management programs.

Donations to a charity are generally tax-deductible, so fiscal sponsorships can provide a tax-incentivized way to fund the program without independently obtaining tax exemption. Even though not obtaining tax-exemption, fiscal sponsorships include a number of restrictions that apply, for example, the sponsoring organization can’t just act like a funnel for funds earmarked to the sponsored program.

For-Profit Organization

For those intrepid souls with both the willingness to undertake the operation of a legal entity and the means to fund it, forming a legal entity through which to conduct operations may be appropriate. While people often believe that charity or other beneficial work must be performed through a nonprofit organization, there is no prohibition on doing so in a for-profit entity. In fact, there are a number of states that have adopted laws authorizing specific types of mission-driven enterprises, such as benefit companies and low-profit limited liability companies (or “L3C”). There are fewer restrictions on operating for-profit entities, as opposed to the significant regulatory burden placed on tax-exempt entities. However, donors cannot deduct the value of contributions to a for-profit organization and the organization must pay tax on any profits earned each year. Of course, the organization can control its tax bill by spending enough of its revenue on ordinary and necessary business expenses to offset any income received during the year.

Private Foundation

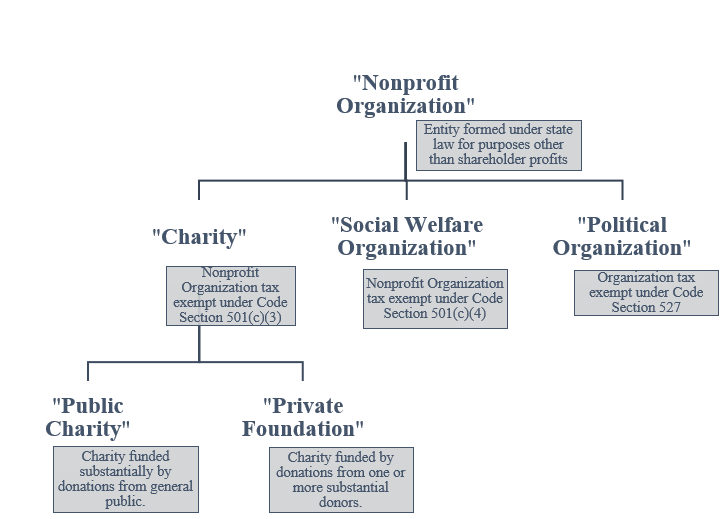

For those who may be interested in forming and operating a legal entity, but to whom tax-deductibility of donations is an important consideration, forming a private foundation may be appropriate. The terminology used in describing tax-exempt entities can be confusing. The following chart shows how to differentiate between different types of organizations at a basic level. The terms in the following chart will be used through these articles.

As noted in the chart above, a private foundation is a type of nonprofit organization that has been recognized as a tax-exempt charity under Internal Revenue Code Section 501(c)(3) and that is funded by a small group of donors rather than the general public. Private foundations are formed for the purpose of improving the lives of a charitable class of the public, usually through charity or education. Private foundations are subject to a great deal of regulations prohibiting abuse and should be staffed by a competent team that is able to shoulder the administrative and regulatory burden of operating a private foundation.

Public Charity

Like a private foundation, a public charity is a nonprofit organization that is recognized as tax-exempt under Internal Revenue Code Section 501(c)(3). Unlike private foundations, public charities are funded by donations from the general public, rather than a single funder or select group of funders. Because there is less likelihood for conflicts of interest, fraud, or abuse where an organization is not beholden to substantial donors, public charities are subject to fewer regulations and restrictions than private foundations. The other side of that coin, of course, is that the founders or major donors have less control and less say in a public charity’s operations unless those persons also occupy the role of director or officer of the organization.

There are many ways to make an impact on the world around you. The preceding options are a high-level overview of some of the more common tax-incentivized ways of doing so. But this is not the full story, the number of ways you can improve others’ lives is truly limited only by your imagination. So, while future articles will discuss a handful of the tax-incentivized options in greater detail, imagining your lasting legacy in this world remains up to you.

[View source.]