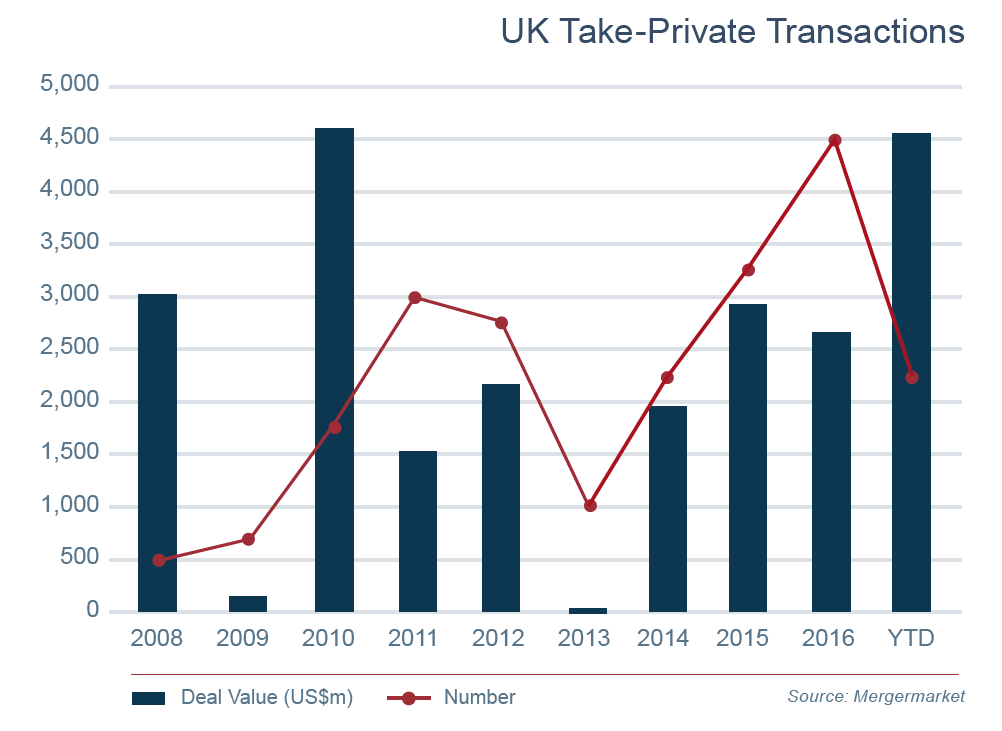

Dealmakers’ appetite for transactions involving publicly listed companies remains strong — 2016 saw an increase in deal volume, a trend which continues into 2017. However, deals remain challenging, partly due to limitations on bidder deal protections and financing requirements. In response, innovative products have been developed by the insurance industry of provide solutions. In our view, these insurance products will help some bidders or public companies overcome perceived barriers to success in the UK market.

Takeover Code Requirements

Concern over Kraft’s 2009/2010 acquisition of Cadbury prompted a strengthening of deal requirements from bidders by the Takeover panel. This new approach — which the UK Takeover Code (the Code) enshrines — includes a general prohibition on certain deal protection measures on public acquisitions, such as “break fees”. A break fee is a fee that a seller or target company agrees to pay to another party (typically the bidder), if a specified event causes the transaction to fail. Further, Code cash confirmation rules require bidders to launch offers for public companies with “certain funds” financing in place, that a financial adviser has publicly confirmed to exist.

Combined, these factors influence how prospective bidders approach takeovers. Insurance market innovation has begun to address these issues, developing new products to help de-risk deals and navigate Code requirements.

“Topping Insurance” — An Alternative to Break Fees

Insurance specialists have recently developed “topping insurance”, which reimburses a recommended bidder if a competitor successfully “tops” its offer for a UK public company (i.e. if the target’s shareholders accept the higher offer). In 2016, several UK public deals followed this fact pattern, demonstrating that in a competitive market, the risk of topping is real. Since 2012, bidders for UK public companies have generally been unable to obtain break fee protection, requiring “topped” bidders to absorb significant failed transaction costs.

Topping insurance covers all third-party deal costs and fees incurred by the unsuccessful bidder, delivering protection comparable to break fees. The ability to avoid paying costly abort fees out of corporate, or even external investors’ funds provides comfort to dealmakers. In our view, topping insurance has the potential to become a widely used substitute for break fees.

Insurance Bonds Help Bidders Satisfy Financing Requirements

The cash confirmation requirements set out in the Code have long presented challenges to UK public company bidders. Making funds available or ring-fencing funds early on in a deal increases transaction expenses and potentially ties up bidder capital. In addition, extensive due diligence is required for funding to be available on a certain funds basis (i.e. fully committed and drawable by a bidder).

Bidders can now employ another new insurance product — “cash confirmation bonds” — to simplify and expedite the cash confirmation process while respecting the certain funds requirements of the Code. Bidders can purchase a bond from a highly rated surety provider, raised against the credit of the bidder group balance sheet. The bond back-stops the bidder’s obligation to pay shareholders and is structured to take account of the financial adviser’s Code obligations. The product increases bidders’ financing flexibility, by allowing bidders to enter the acquisition finance market later during the deal timeline, and seek competitive financing terms on a more transparent basis, after the issuance of an opening “Rule 2.7 announcement”. The product also allows bidders funding the deal from existing resources to retain control over their capital. In our view, cash confirmation bonds, which were first issued this year in a Code transaction, have the potential to become a useful tool for corporate bidders looking to retain balance sheet flexibility.

“The products we have developed are driven by deal-specific circumstances, and the issues advisers bring to us. The more we can interact with and understand the issues dealmakers are facing, the more we can address those issues with bespoke insurance solutions.”

Piers Johansen, Managing Director, Aon