Almost anything that could go wrong in 2020 did go wrong. The year started with the Russian/Saudi oil price war and then the COVID-19 pandemic hit the U.S. and the rest of the world, which caused dramatic drops in crude demand and extreme price volatility. As a result, the confluence of these events led to an unprecedented wave of bankruptcies and restructurings throughout the upstream oil and gas industry.

As more companies contemplate bankruptcy or restructuring arrangements, could the time be right for onshore drilling rigs and assets to be snagged at bargain prices? With a known capital outlay, plus other ancillary costs and limited downside, what players are willing to acquire these assets and not leave them as paperweights? The risk-takers? The risk-averse? Oil and gas producers themselves?

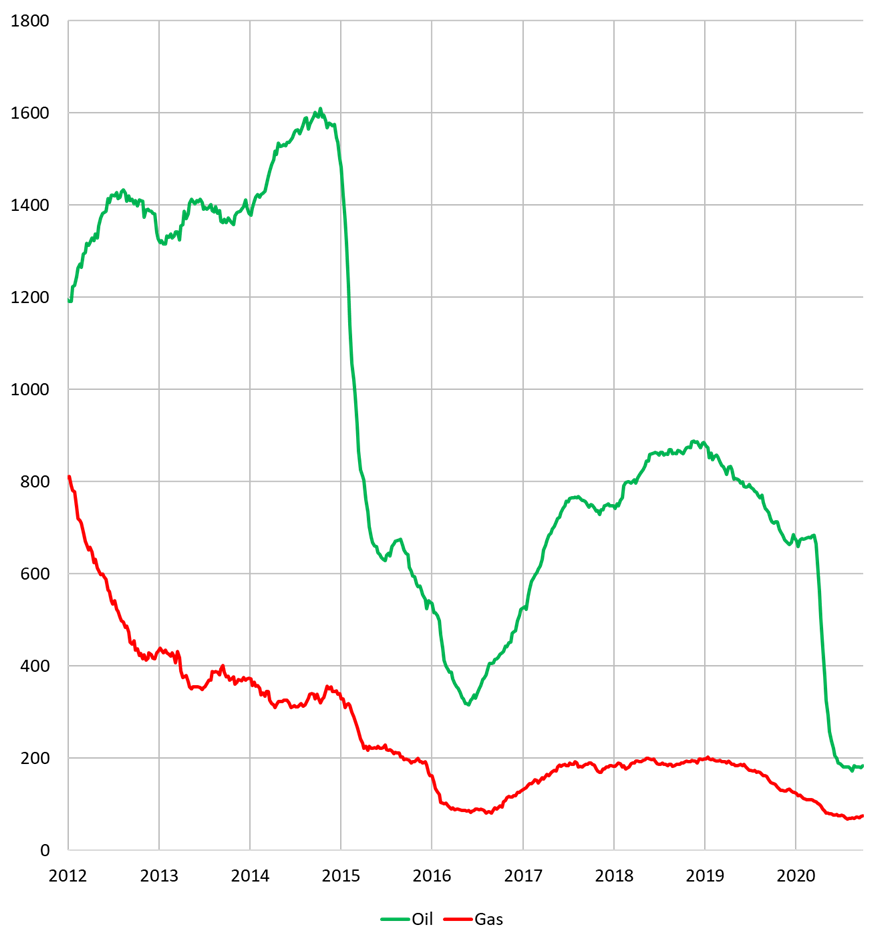

Under Pressure

Evidence of the downward pressure oil and gas producers are facing with depressed commodity pricing can be seen in the rig count. On September 25, the U.S. rig count stood at 261, an increase of six rigs from the prior week, but down 599 from last year, according to data from Baker Hughes.

Rig Activity By Product

(Source: Baker Hughes)

While an increase in the rig count isn’t expected until at least after the presidential election, a reliable vaccine for COVID-19 is mass-produced and distributed to the public and, most importantly, the economy returns to pre-pandemic levels, few signs point to clarity for crude demand and pricing going forward. This is all leading to higher financial pressure on the oil and gas industry. No matter how these near-term events play out, however, oil and gas production decline curves will continue, and physical production will slow.

Banks have already started the exit process. Recently, Hancock Whitney sold its energy loans to Oaktree Capital Management at nearly a 50% discount. Only Oaktree can say if this was a fast flip opportunity or a long-term asset purchase. Case in point: if you cannot borrow from a bank today then they’ll more than likely have oil and gas assets to sell tomorrow—even at a steep discount.

If current trends continue, it appears bankruptcies and restructurings in the oil and gas sector will likely continue into 2021 as liquidity dries up and asset-based loans are revalued at lower commodity prices. Despite receiving some protection by filing Chapter 11 or entering into other solvency arrangements, companies will still need to generate liquidity by having to sell assets (including rigs) or consider alternatives to optimize existing operations such as by reducing general and administrative (G&A) overhead costs, reducing capital expenditures, deleveraging balance sheets, reducing headcounts and/or other operational improvements to maximize free cash flow.

Who Are The Buyers?

Lowball bidders will have the most flexibility when negotiating acquisition targets. Why? They have the ability to create their own low price/bid entry point where downside can be limited and known costs can be reasonably estimated, including refurbishment cost, storage/parking costs and exit costs via scrap metal price or resale value.

For E&P companies, they may find it appealing to have their own rig(s) sitting idly on standby, possibly bringing drilling operations in-house thus removing service risk and cost volatility. E&P companies know what kind of rig(s) will be needed if their capital expenditure (or “capex”) belt loosens. We believe this could lead to a historical shift in the upstream oil and gas structure.

Time For A New Drilling Company Startup?

The time may be right for a new kind of land drilling service company with the prototype of this vision being a smaller, nimbler, specifically designed and geographically-focused service company (think along the lines of a pipeline company looking at a production basin before laying pipe). For an E&P company, this could be a new subsidiary or line of business that meets internal drilling needs for the foreseeable future.

A newly formed and capitalized, potentially debt-free vendor, could mitigate or completely remove the operational, contractual, and credit risks that current land drillers might have in the eyes of their clients. Customers may want all the risk aversion possible as they cannot afford to see a rig abandoned mid-drill if a roughneck’s paycheck bounces.

"The time may be right for a new kind of land drilling service company with the prototype of this vision being a smaller, nimbler, specifically designed and geographically-focused service company."

A new oil and gas service company startup (or E&P subsidiary) may have hit the trifecta with acquiring distressed assets via a Section 363 sale, experienced employees readily available, and shale formations with known rig and drilling requirements. With many land drillers dealing with past burdens (i.e., high debt levels and industrywide operations), would a fresh-start company with specific drilling capabilities for specific production areas be a golden child/cash cow?

A newly formed, strictly operational drilling company generating a straight return on investment (ROI) has no need to waste capital on R&D or maintain multiple operational areas. For E&Ps, this would allow for more flexibility as there wouldn’t be the responsibility of fulfilling contractual obligations to continue drilling if the current downturn extends longer in the future. In the theoretical case that things improve dramatically, price competition would be removed if drilling operations are in-house.

In addition, exchange deals with cash-starved E&P companies for drilling programs via creative non-cash day rates may offer options for value creation. This would allow capital-constrained E&Ps to continue or start new drilling programs while splitting up the risks and costs with the driller. This in turn could create a backdoor property acquisition strategy or production overrides for the driller. For investors, this might be a better option than buying properties and avoid larger capital outlays for conventional property acquisitions.

Breaking Up: It’s Not You, It’s Me

Alternatively, if oilfield service companies are becoming more like debt service companies—an example being Nabors Industries where, for the three months ended June 30, 2020, interest costs where about 9.6%, up from 6.7% year-over-year of operating revenues—should consideration be given to breaking up onshore oilfield service companies? Multinational organizations could break themselves up into specific geographies and allow truly industry-focused investors to pick their oilfield service company free agents just like shale play-specific production companies.

Current drilling companies may be dominant in certain formations and they can leverage this without being burdened by underperforming operational areas. This may be a tempting alternative to management teams and equity owners while they still have the right to do this, and before banks and bondholders take this optionality away. Management teams may want to assess their current corporate structures to see if an “escape plan” can be hatched to save some operations before they pass the point of no return and need to file for bankruptcy protection.

DOWNLOAD PDF