UPDATES AT A GLANCE — AUGUST 2022

MARKET TRENDS

LBO FINANCING CONSIDERATIONS

M&A TRANSACTION CONSIDERATIONS

ESG INVESTMENT STRATEGY DISCLOSURES

Market Overview — Q2 2022[1]

Downturn in Credit Markets: In its continued effort to combat rising inflation, the Federal Reserve Bank raised its benchmark interest rate in each of March, May, June and July of this year by 25 bps, 50 bps, 75 bps and 75 bps, respectively. The impact of rising interest rates, together with global supply chain issues, geopolitical tensions and investors pulling funds from leveraged loan funds, has reverberated throughout the leveraged loan and high-yield bond markets. As a result, PE sponsors and their portfolio companies initially looked to private credit lenders to fulfill their acquisition and portfolio company financing needs, but the private credit market has not been immune to the larger macroeconomic factors affecting the syndicated loan market and, with the exception of certain sectors like technology, the private credit market has similarly cooled off.

M&A Activity: U.S. PE deal activity slowed from the record levels set in Q3 and Q4 of 2021, but it remains above the historical average on both a deal count and deal value basis. Given the complex deal environment, a slow-down in deal activity moving into second half of 2022 is anticipated as many of the deals in the first half of 2022 were signed in late 2021 or early 2022.

PE Tech Activity: IT deals are making up an increasing portion of U.S. PE Deal activity by deal value (up from 22% in 2021 to 28.7% in H2 2022). However, IT deals remain fairly stable as a percentage of U.S. PE deal activity by deal count, suggesting IT valuations are proving to be more robust to the changing economy than other sectors.

Add-Ons: There has been an uptick in the percentage of buyout activity attributable to add-ons (up from 72.4% in 2021 to 78.2% in H2 2022 ) despite increased scrutiny of private-equity healthcare deals by the FTC.

Exit Activity: U.S. PE exit activity drastically slowed in H2 2022, falling slightly below the five year historical average in part due to valuation uncertainty and the weakened public markets, which has continued to drive a robust GP-led secondaries market. The proportion of exits to strategic buyers in Q2 was one of the highest figures since 2009, driven by high levels of cash on the balance sheet and the search for acquisitions to position strategic buyers for growth. Sponsor-to-sponsor exits declined compared to Q1 as Sponsors held on to assets in light of valuations.

As the challenges of Q1 have continued into Q2, deal- makers are navigating a complex environment on multiple fronts, which may result in a “wait and see” approach to new platform investments. Given the fast pace of capital deployment in 2021 where deal making values nearly doubled previous highs and concerns of LPs with respect to over-allocation to private equity in their portfolios, sponsors may seek to implement slower deployment schedules.

To view a larger version, please click here.

LBO Financing

Debt Issuance Overview Q2 2022

May and June saw less new debt issuances in the public and broadly syndicated markets and overall pricing ratcheted up. The tightening of the debt financing markets seemingly marks an end to the LBO-boom we saw in 2021 now that cheap debt is scarce. As more traditional bank lenders slowed their volume of issuances for fear of not being able to syndicate the loans they have underwritten, the private credit markets initially stepped in to backstop issuers’ loss of access to the syndicated loan market, but have lost steam in recent weeks in light of the same macroeconomic conditions affecting the syndicated loan market, coupled with a high volume of capital already deployed this year in light of the increased prevalence of mega unitranche facilities in excess of $1 billion, once a novel facility size in the private credit market but gaining in traction until the recent slowdown.

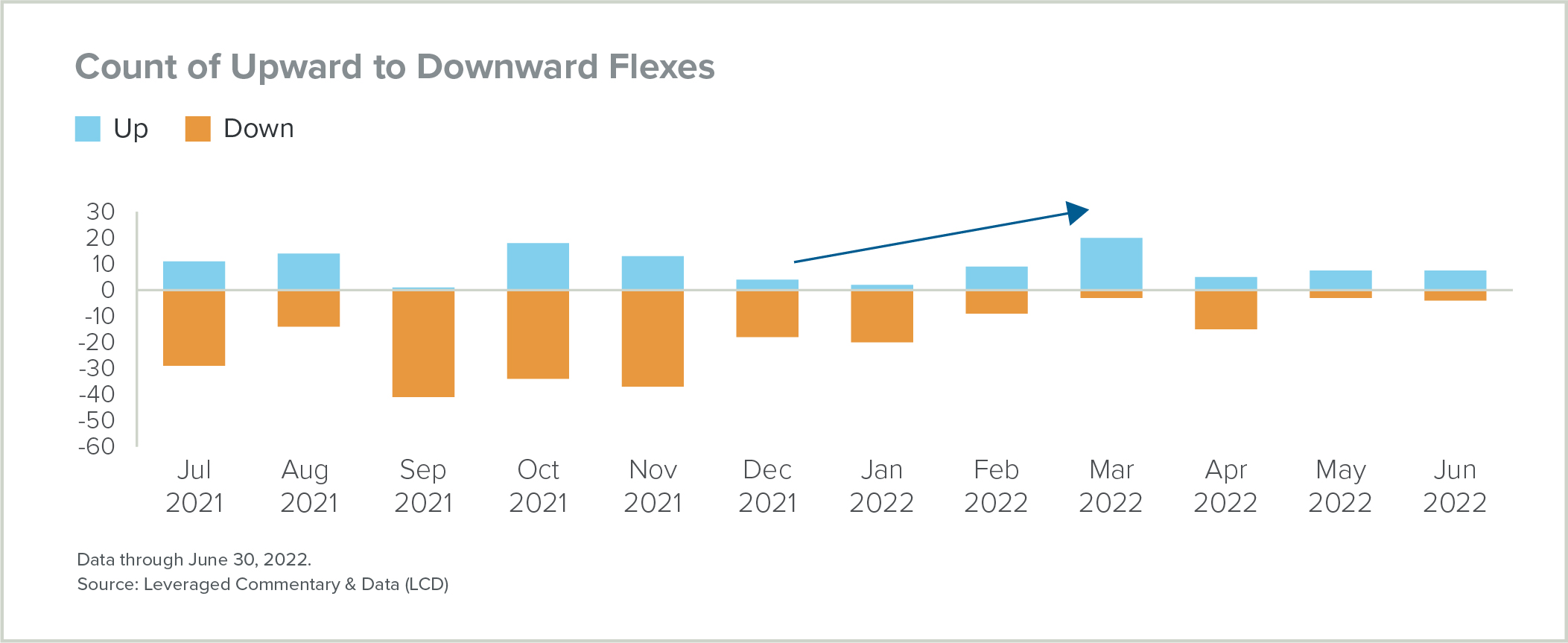

Private Credit — Pricing Certainty/No Flex

One of the many benefits of using private lenders is that, because there is no syndication process, there is no ability to “flex” the pricing to a higher rate through increased margins or increased original issue discount in order to syndicate the deal.

In Q2 2022, syndicated lenders increasingly “flexed” pricing to clear deals[2] (see chart). As a result, PE firms and their portfolio company borrowers have been increasingly using the private credit markets to gain more certainty as to their pricing and other terms.

Securing Lower Pricing: Several PE firms in recent months have obtained large delayed draw term loan facilities for existing portfolio companies to use under lower pricing levels before certain interest rate hikes and with limited conditionality, all of which have helped finance add-on acquisition transactions.

To view a larger version, please click here.

Considerations for Existing Financings and Future Financings

Interest Coverage Ratios: In addition to actually paying higher interest as the benchmarks rise, sponsors should be aware of the impact of rising rates on any interest-coverage ratios or fixed-charge coverage ratios in their existing financing deals, since these ratios require borrowers to maintain the ability to cover their interest expense (and, in the case of fixed-charge coverage ratios, other fixed-charges) as compared to EBITDA.

The impact of rising rates on financial covenants, borrowers’ ability to keep up with interest payments when due and the availability of financing for new deals are just some of the issues that would arise if the current situation tilts into a recession, which economists predict is now more likely (predicted to be between 19% to 30% likelihood)[3] as we come closer to entering a bear market and the Fed commits to continuing interest rate hikes as needed to curb inflation. PE firms should carefully consider how these situations may impact their existing credit facilities and be thoughtful about structuring new credit facilities to best position themselves and their portfolio company borrowers to weather any potential storm and maintain liquidity.

Increase in use of PIK Toggle Provisions: For new debt financing deals, PE firms should consider the need for flexibility in payment options. We are seeing an increase in the amount of PIK toggle provisions being requested or negotiated, giving borrowers the option to make at least a portion of interest payment obligations by either paying in cash or electing to “pay-in-kind,” with the ability to “toggle” between those options as desired.

M&A Transaction Considerations

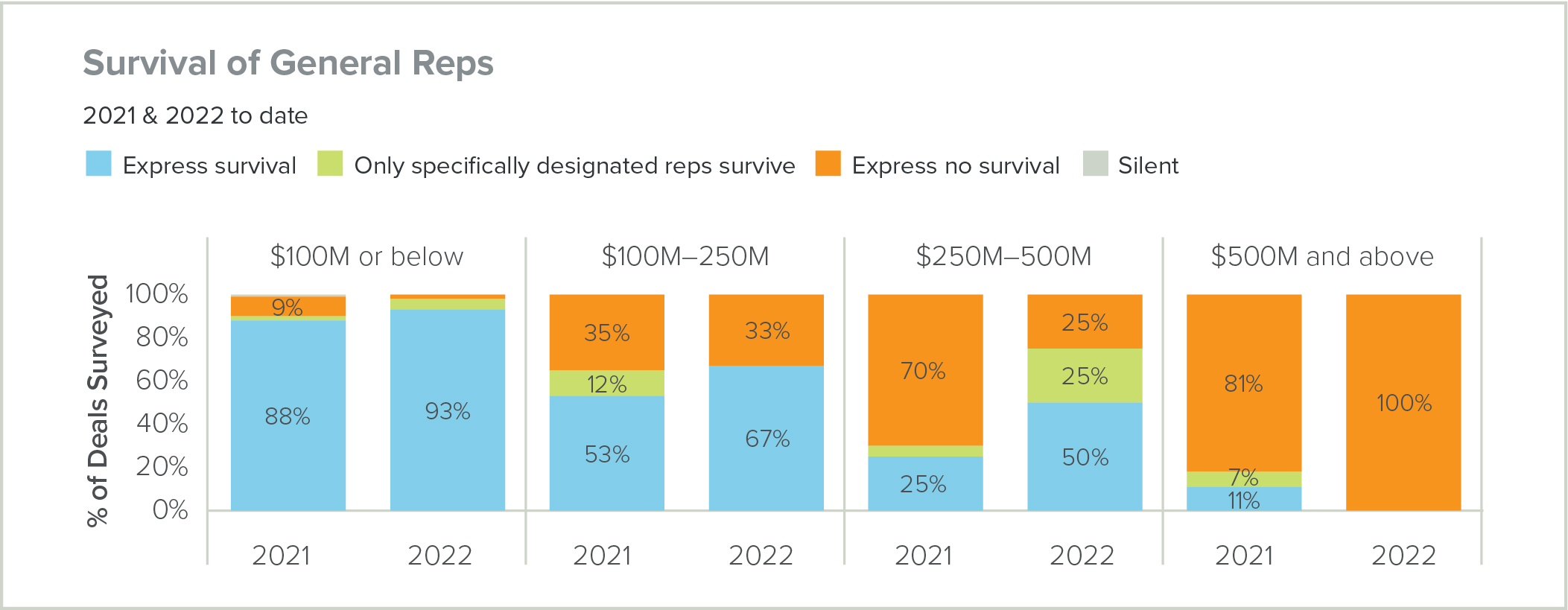

Private Equity Deal Database — Market Insights on Indemnification Trends

In 2021, it was rare to see a seller standing behind company representations and warranties in a deal with a transaction size over $500 million, with the buyer instead self-insuring or relying on third-party representation and warranty insurance. In the seller-friendly 2021 market, this trend trickled down into the middle market, and we saw a number of transactions valued between $50 million to $500 million following suit.

Now that we are entering a somewhat less-seller friendly market in 2022, what (if any) impact has there been on the appetite for buyers to agree to such seller-friendly terms? We explored this question using our Private Equity Deal Database, a comprehensive, proprietary value-adding database which provides unparalleled insights into the current state of markets and deal-making at all valuation levels.

- There has been a shift towards buyers requiring sellers to stand behind company representations in deals under $500 million. The use of express survival provisions has increased by the greatest amount (25%) in deals with enterprise values between $250 million to $500 million.

- There has been a shift in the opposite direction for deals with enterprise values above $500 million, where sellers are not being required to stand behind company representations. This likely indicates the assets within this valuation range are still considered attractive and competition for them is still strong.

To view a larger version, please click here.

R&W Insurance

Pricing and Capacity: Now mid-year into 2022, the market conditions for R&W insurance have continued to improve. The rate on line (premium divided by the policy limit) has been trending down to around 4%, and we are seeing rates dip below 4% more regularly.

Healthcare Deals: Healthcare deals are seeing better options and competition in the R&W insurance market compared to last year. While “healthcare” includes a wide range of businesses, some attracting more insurer interest than others, it was not uncommon in 2021 to see zero to one quote for healthcare deals when the volume of M&A deals seeking R&W insurance surpassed the R&W underwriters’ bandwidth. Since the beginning of the year, buyers are seeing greater options between new market entrants and existing insurers who have increased their appetite for healthcare deals.

Beware of “Other Insurance” Expectations: One of the trends and a point of contention in recent years has been the interplay between R&W insurance and the company’s insurance, especially with respect to cyber and professional liability insurance.

- Buyers should look out for words like “excess” and “excess no broader than” in R&W quotes and discuss its appropriateness and implication with advisors. These words reflect the expectation for a particular type of underlying insurance and whether or not the scope of the R&W insurance would be restricted by the scope of such underlying insurance.

- Buyers should proactively investigate whether to procure any required insurance coverage for the pre-closing period through the company’s existing insurance (typically using “tail” or “runoff” coverage) or, if available, as an add-on to the buyer’s insurance with the inclusion of “prior acts” coverage.

- It is important to discuss this early on as part of the deal negotiation, as M&A agreement forms often contemplate a D&O insurance tail only, and obtaining these insurance options can take time due to the parties needing to allocate whether the buyer or seller will acquire the insurance.

- Absence of requisite underlying coverage may cause the R&W insurer to propose a higher deductible for certain types of losses under the R&W policy, which needs to be carefully reviewed and negotiated.

Private Equity Healthcare

Enforcement Trend: PE Firms on the hook for portfolio company conduct

ESG Investment Strategy Disclosures

Objective of Proposed ESG Disclosures: As a result of continued greenwashing concerns on May 25th 2022, the SEC proposed new rules (“Proposed ESG Disclosure Rules”) to enhance disclosures by registered private equity funds that incorporate or consider ESG factors as part of their investment strategy.

Applicability of the Proposed ESG Disclosures: The proposed rules would apply to registered investment advisors, certain exempt advisers, registered investment companies, and business development companies. Such firms that incorporate or consider ESG factors into their investment strategy and objectives will be required to make ESG disclosures based on the type of ESG strategy being pursued (briefly summarized below).

Considerations: PE firms that are not implementing an ESG strategy would not be subject to the Proposed ESG Disclosures Rule; however this may adversely affect the ability to launch ESG products.

Implementation: The deadline for comments is August 16, 2022. Given the SEC’s current agenda, determining the final scope and timeline of the proposed rules is difficult to determine.

Misleading Fund names — Proposed Names Rules Amendments

Current Names Rule: To address fund names that are likely to mislead an investor about the fund’s investments and risks, the SEC adopted the Names Rule in 2001. The Names Rule currently requires a registered fund (but not private funds) whose name suggests that is has a focus on a particular type of “investment, industry, country or region” to adopt a policy to invest at least 80% of the value of its net assets in the “investment, industry, country or region” corresponding to its fund name.

Proposed Amendments to the Names Rules: The proposed amendment to the Names Rules would:

- Prohibit a fund from using ESG or similar terminology in its name where the fund is following an ESG “integration” investment strategy (as mentioned above). This element of the proposal is one example of the SEC’s general view on what constitutes misleading marketing practices for funds including private funds.

- Enhance a fund’s prospectus disclosure to require it to define the terms used in its name, including the criteria the fund uses to select the investments that the term describes. Terms used in a fund’s name that suggest an investment focus (e.g., an ESG focus) would need to be consistent with those terms’ plain English meaning or established industry use.

Timeline: If implemented, sponsors would have one year to comply with the amendments from the date that the final amendments are published in the Federal Register.

[1] Source: PitchBook data; Goodwin analysis.

[2] Source: S&P./LSTA Leveraged Loan Index, LCD.

[3] Source: Wall Street sees higher probability of U.S. recession next year | Reuters

[4] Source: U.S. ex rel. Martino-Fleming v. South Bay Mental Health Center, Civ. Action No. 15-13065 (D. Mass. May 19, 2021).

[View source.]