The current focus of the international tax community is on the United States, and for good reason. In the midst of a contentious political landscape, months of anticipation, and a decidedly clandestine drafting process, U.S. tax reform was enacted in legislation referred to as the Tax Cuts and Jobs Act of 2017 (the "Act"), effecting the most sweeping and monumental changes to the U.S. international tax system in over three decades.

With respect to non-U.S. based (inbound) investments, the most groundbreaking changes under the Act are as follows:

-

The lowering of the U.S. corporate tax rate to 21%

-

The implementation of new net operating loss deduction and carryforward rules

-

New, more stringent, interest expense deduction limitations

-

The denial of interest expense deductions arising from hybrid instruments and entities

-

A new base erosion and anti-abuse tax

In addition to the above, various new rules under the Act have moved the United States much closer to a territorial tax system. That is to say, prior to the Act, under the United States' historical worldwide system, U.S. corporations were taxed on all income, including dividends from non-U.S. subsidiaries, irrespective of where that income was earned. Under the Act, dividends paid to U.S. corporations out of foreign earnings will no longer be taxable to the U.S. corporate recipient.

This alert focuses on "inbound" issues confronting corporate investments into the United States (i.e., the taxation of foreign persons with respect to their U.S. corporate investments). For completeness, we also discuss the new mandatory inclusion provision for offshore earnings and the exemption for dividends from foreign sources, as well as several other ancillary provisions, including certain changes with respect to the determination of a foreign subsidiary's status as a controlled foreign corporation. For a discussion of all of the international tax considerations affecting U.S. corporations under the Act, including outbound issues and changes to the general anti-deferral system, click here.

Lowering of U.S. Corporate Tax Rate

Under prior U.S. law, a corporation was subject to graduated federal income tax rates of 15%, 25%, 34%, and 35% based on the amount of its taxable income. Under the Act, these four brackets are replaced by a single 21% bracket for all income levels, effective for tax years beginning on or after January 1, 2018 (a blended tax rate applies for most fiscal year taxpayers). Effectively, this means a reduced income tax rate for the vast majority of U.S. corporations.

Most existing international structures are premised on the overarching principle that the United States had one of the highest corporate tax rates in the world. A high U.S. corporate tax rate created a strong incentive for businesses to shift earnings from the United States into jurisdictions with lower tax rates by making deductible payments to affiliates in such lower-tax jurisdictions, and a strong disincentive for such businesses to repatriate cash to the United States. This new corporate tax rate reduction instantly removes the efficacy of such fund flows, which now create unnecessary tax leakage within many international structures. Taxpayers will now have to seriously consider whether such structures make sense on a continued basis.

Moreover, the balance sheet impact of the corporate tax rate cut is striking. Companies that have booked deferred tax assets ("DTAs") place on their balance sheet the tax savings that will arise from future tax deductions (or exclusions from taxable income), whereas deferred tax liabilities ("DTLs") reflect taxes that will be due on future taxable amounts. With the corporate tax rate drop, both the value of a DTA and the exposure from a DTL will be reduced. Companies with sizeable DTAs will record an earnings loss when they write down the value of those assets. Companies with sizeable DTLs will report a one-time earnings gain as they write down the amount of their liabilities. Numerous recent earnings reports have illustrated this impact from the rate change on companies of all sizes. For companies that have valued DTAs in their earnings multiples for acquisition-pricing purposes, the write-down will not be positive news. However, it may be mitigated by the benefit of the ongoing lower tax rate on earnings. Some multinational companies will also need to report the impact of the mandatory inclusion (discussed below).

The effect of the new rate is illustrated in the example below. The example presumes a multinational group structure involving a parent company organized in a hypothetical European Union jurisdiction (a jurisdiction we will simply call "E.U.") and a U.S. subsidiary. In the examples, the following assumptions apply:

-

The pre-tax reform effective corporate rate is 40%, reflecting a federal statutory rate of 35% and deductible state and local taxes at an assumed rate of approximately 8% (.08*65 = 5% + 35% = 40%)

-

The post-tax reform effective corporate tax rate is 27%, reflecting a federal statutory rate of 21% and deductible state and local taxes at approximately 8% (.08*79 = 6% + 21% = 27%)

-

All interest expense is deductible under applicable interest expense limitations

-

Benefits are available under a tax treaty between the United States and E.U.

-

In E.U., the corporate tax rate is 30%

-

E.U. has a participation exemption under which dividends from an eligible foreign subsidiary (including USCO below) are taxed by E.U. at a reduced corporate tax rate of 5%

Example 1

In this example, assume all earnings are paid from USCO to Foreign Parent in E.U. as taxable dividends.

Pre-Tax Reform

Pre-Tax Reform

-

USCO has taxable income of $100.

-

USCO's taxable income of $100 is subject to tax at 40%, resulting in U.S. corporate tax of $40.

-

A dividend of $30 is then paid to Foreign Parent, where it is subject to 0% withholding tax in the United States under the U.S.-E.U. treaty, and subject to 5% tax in E.U. under the E.U. participation exemption. This dividend therefore results in additional E.U. tax of $1.50.

-

The total tax burden is $41.50, yielding an overall effective tax rate of 41.5%.

Post-Tax Reform

-

Income is now taxed at a higher rate in E.U. (30%) than in the United States (27%).

-

USCO has taxable income of $100.

-

USCO's taxable income of $100 is subject to tax at 27%, resulting in U.S. corporate tax of $27.

-

A dividend of $30 is then paid to Foreign Parent, where it is subject to 0% withholding tax in the United States under the U.S.-E.U. treaty, and subject to 5% tax in E.U. under the E.U. participation exemption. This dividend therefore results in additional E.U. tax of $1.50.

-

The total tax burden is $28.50, yielding an overall effective tax rate of 28.5%.

-

As illustrated above, the overall effective tax cost drops from $41.50 to $28.50. Post-reform United States is a significantly lower-cost tax environment than before.

Example 2

In Example 2, assume Foreign Parent lends to USCO, which yields annual interest expense payments of $30.

Pre-Tax Reform

Pre-Tax Reform

-

USCO has taxable income of $100 and interest expense of $30, payable to Foreign Parent.

-

USCO's taxable income of $70 (net of interest expense) is subject to tax at 40%, resulting in U.S. corporate tax of $28.

-

The $30 of interest expense is subject to 0% withholding tax under the U.S.-E.U. treaty and is subject to corporate tax of 30% in E.U., yielding an additional tax of $9.

-

The total tax burden is $37, yielding an overall effective tax rate of 37%.

Post-Tax Reform

-

Income is now taxed at a higher rate in E.U. (30%) than in the United States (27%).

-

While not addressed in this example, the more restrictive interest expense limitations and the Base Erosion Minimum Tax (discussed below) could provide a further disincentive to the implementation of these structures.

-

USCO has taxable income of $100 and interest expense of $30, payable to Foreign Parent. USCO's taxable income of $70 (net of interest expense) is subject to tax at 27%, resulting in U.S. corporate tax of $19.

-

The $30 of interest expense is subject to 0% withholding tax under the U.S.-E.U. treaty and is subject to corporate tax of 30% in E.U., yielding an additional tax of $9.

-

The total tax burden is $28, yielding an overall effective tax rate of 28%.

-

Note that if the $100 of the gross income earned by USCO simply remained in the United States, the effective rate would be only 27%. Therefore, unlike the pre-tax reform example, introducing deductible base eroding payments into the United States has the effect of increasing, rather than decreasing, the overall tax leakage in the group.

A brief summary chart of the above examples is below. As can be seen, with respect to effective corporate tax rate, post-Tax Reform, the United States is a far more attractive environment, and introduction of leverage into the United States no longer provides the same level of benefits as in the past.

|

|

Pre-Reform

Assumed Combined U.S. Federal and State/Load Rate |

Pre-Reform Effective Rate in Group Structure |

Post-Reform Assumed Combined U.S. Federal and State Local Rate |

Post-Reform Effective Rate in Group Structure |

|

No Leverage |

40% |

41.5% |

27% |

28.5% |

|

Leverage |

40% |

37% |

27% |

28% |

New Net Operating Loss Deduction Rules

Under current law, a net operating loss ("NOL") is the amount by which a taxpayer's current-year business deductions exceed its current-year gross income. Under previous law, NOLs could not be deducted in the year generated but could be carried back two years and carried forward 20 years to offset taxable income in such years.

For tax years beginning after 2017, the Act limits the deduction for NOLs to 80% of the taxpayer's taxable income. The Act also repeals the two-year carryback (except in the case of certain farming losses) and provides for an indefinite carryforward of unused NOLs. Importantly, the Act limits only NOLs generated on or after January 1, 2018 (as opposed to carryforwards of NOLs generated prior to that date).

Prior to the Act, most businesses generating losses were still subject to the corporate alternative minimum tax ("AMT") by virtue of only being able to offset 90% of AMT income with NOLs in a given year. The Act will therefore have the effect of applying this general principle, albeit at a lower threshold, even though the Act otherwise repeals the corporate AMT.

New Interest Expense Limitations

Under prior law, net interest expense paid by a U.S. corporation to a foreign related party was limited under the earnings stripping rules (Code section 163(j)) if (1) the U.S. corporation's debt-to-equity ratio exceeds 1.5 to 1.0 and (2) net interest expense of the U.S. corporation exceeds the sum of 50% of the adjusted taxable income (roughly, EBITDA) of the corporation for such year.

Under the revised Code section 163(j), the interest expense deduction is now limited to an annual amount equal to 30% of adjusted taxable income and the limitation applies to interest payments to all lenders, not just foreign affiliates. Businesses with average gross receipts of $25 million or less for the prior three tax years are not subject to the limitation. For tax years beginning after December 31, 2017, but before January 1, 2022, adjusted taxable income is calculated without regard to deductions for interest, taxes, depreciation, amortization or depletion (i.e., adjusted taxable income would approximate EBITDA); in taxable years beginning on or after January 1, 2022, it would change to EBIT (i.e., earnings reduced by depreciation and amortization), making it more likely that interest would be disallowed under this provision.

Disallowed interest expense would be permitted as an unlimited carryforward and would be a tax attribute that could be carried over in certain corporate acquisitions and other reorganizations.

It should be noted that the recent Code section 385 provisions were not repealed. These regulations provide highly detailed and complex standards for distinguishing between debt and equity of certain corporations, as well as stringent documentation requirements with which corporations must adhere in order to ensure that certain instruments will be respected as bona fide indebtedness for U.S. tax purposes.

Denial of Deductions in Hybrid Arrangements

Under a special anti-hybrid provision, a U.S. corporation would be denied a deduction for certain "disqualified related party amounts" paid (1) pursuant to a "hybrid transaction" or (2) by, or to, a "hybrid entity." For these purposes, a disqualified related party amount would be any interest or royalty paid to a foreign person to the extent that under local law (1) there is no corresponding income inclusion to the related party, or (2) such related party is allowed a deduction with respect to such amount. The term "related party" means a related person as defined in Code section 954(d)(3). A hybrid transaction is any transaction or series of transactions, agreement, or instrument with respect to which one or more payments are treated as interest or royalties for U.S. tax purposes and which are not so treated for purposes of the tax law of the foreign country of which the recipient of such payment is resident for tax purposes or is subject to tax. This could include payments made by or to an entity that is disregarded for U.S. tax purposes.

This provision would implement certain initiatives discussed under the OECD's Base Erosion and Profits Shifting ("BEPS") plans (specifically, BEPS Action Plan Number 2) designed to prevent taxpayers from creating "stateless income" through manipulation of discrepancies in the treatment of entities and instruments under the laws of different jurisdictions to create windfalls from associated tax savings.

Base Erosion and Anti-Abuse Tax

The Act provides for a new Base Erosion and Anti-Abuse Tax ("BEAT") designed to provide a further disincentive to corporate taxpayers to "erode" the U.S. tax base by making deductible payments (including interest expense and royalties) to foreign related parties. The BEAT applies only to large corporate taxpayers earning an average of at least $500 million in gross receipts and with a "base erosion percentage" of at least 3% (2% in the case of certain banks) during the three-year period immediately preceding the applicable tax year.

The BEAT will be equal to the excess of 10% (5% for 2018 and increasing to 12.5% beginning in 2026) of the "modified taxable income" of a taxpayer over the taxpayer's regular tax liability, subject to certain adjustments (such as, for example, those pertaining to certain U.S. tax credits). For these purposes, modified taxable income would mean the taxable income of the taxpayer computed under the usual rules but determined without regard to any "base erosion tax benefit" or the "base erosion percentage" of any net operating loss deduction.

The "base erosion percentage" is calculated by dividing the corporation's base erosion tax benefits (e.g., deductible "base erosion payments") by the corporation's total deductions. A "base erosion payment" would generally mean any deductible payment made by the U.S. person to a foreign related person, including payments made or accrued to acquire depreciable or amortizable property. Base erosion payments would not include: (i) any amount that constitutes reductions in gross receipts including payments for costs of goods sold; (ii) any amount paid or accrued by a taxpayer for services if such services meet the requirements for eligibility for use of the "services cost method" under the transfer pricing rules, but without regard to the requirement that the services not contribute significantly to fundamental risks of business success or failure and only if the payments are made for services that have no markup component; and (iii) any qualified derivative payment, if certain requirements are met. Under the business-judgment rule, a service cannot constitute a covered service unless the taxpayer reasonably concludes in its business judgment that the service does not contribute significantly to key competitive advantages, core capabilities, or fundamental risks of success or failure in one or more trades or businesses of the controlled group. In other words, for those services that qualify, no markup would be permitted.

Services that qualify for the "services cost method" requirement under these rules must be (i) a "covered service" for (ii) something that is not an "excluded activity" and (iii) for which adequate books and records are maintained. Such covered services include those identified under IRS revenue procedure as support services common among taxpayers across industry sectors and which generally do not involve a significant markup on total service costs. Excluded activities ineligible for this method include manufacturing, production, extraction exploration or processing of natural resources, construction, reselling and distribution activities, R&D, engineering or scientific activities, activities performed in connection with financial transactions, and insurance. Conversely, some specific examples of activities that could potentially qualify for the services cost method include data entry, recruiting services, credit analysis services, data verification services, and legal services.

The BEAT statute treats certain related (i.e., "controlled") groups of companies as one taxpayer, provided there is a greater than 50% vote or value relationship held between such entities. This is referred to as the aggregation rule. Read literally, it is possible to interpret the aggregation rule as effectively disregarding base erosion payments made between members of the same controlled group for purposes of calculating the base erosion percentage, as the rule treats the group as a single taxpayer for this purpose. This, however, appears to be an error in the drafting of the statute. Similarly, payments to foreign affiliates that constitute effectively connected income are considered base erosion payments. That is, payments to the U.S. branch of a foreign affiliate that are treated as effectively connected income of the foreign affiliate are treated as base erosion payments, even though such payments are fully taxable in the United States. This is consistent with the treatment of payments that constitute subpart F income (i.e., such payments are also subject to the BEAT even though they are subject to current U.S. tax). Both provisions seem to reflect the fact that the BEAT serves the purpose of being both a base erosion prevention mechanism and a minimum tax.

While partnerships are not subject to the BEAT, there is also substantial ambiguity as to how partnerships should be analyzed in applying the BEAT. It would seem inappropriate to excuse corporations from the application of the BEAT when they happen to be members of a partnership. Instead, it seems that each corporate partner should make its own BEAT determination. Further, there is also the question of how to apply the BEAT when payments are made to a partnership because it is unclear whether the partnership or the partner should be treated as the recipient of the payment.

For example, when a deductible payment is made by a U.S. person to a partnership, it is not clear whether a partnership is treated as a separate entity (the "entity approach") or merely as an aggregate of its various partners (the "aggregate approach"). Consider a case in which a U.S. person makes a deductible payment to a foreign partnership that has only U.S. partners. An entity approach would result in a payment that is subject to the BEAT notwithstanding the fact that the only persons taking income into account on the payment would be U.S. persons, while an aggregate approach would exempt the payment from the BEAT altogether. In an inverse fact pattern (i.e., when the payee is a U.S. partnership with foreign partners), an entity approach would result in an exemption from the BEAT while an aggregate approach would bring the BEAT back into play.

While the BEAT is largely aimed at inbound companies, it will apply to any corporation that makes payments to related foreign corporations, with a decidedly broad standard of relatedness (generally, a 25% common ownership standard instead of the usual 50%). As a result, it could apply to U.S. corporations making payments to foreign subsidiaries. Many U.S.-based multinationals will need to restructure their operations in response to this tax. Moreover, it remains to be seen how this tax will apply in both a consolidated return situation and in the case where multiple U.S. persons are related to one another but are unable to file a U.S. consolidated return (such as would be the case in a so-called "expanded affiliated group").

Example

The BEAT operates as a minimum tax. Consider the example below, again involving a multinational group including an E.U. parent and its U.S. subsidiary. Note that the example is set in tax year 2019 to reflect the more permanent 10% BEAT rate (rather than the special 5% rate, which applies only for 2018). While there is currently some ambiguity in how to apply the applicable provisions of the BEAT, we believe the example below reflects the best understanding of those rules:

|

|

2019 Regular Tax |

2019 BEAT |

|

Gross Income |

$1,500 |

$1,500 |

|

Base Eroding Payments |

($1,000) |

|

|

Other Deductions |

($200) |

($200) |

|

Net Income |

$300 |

$1,300 |

|

Tentative Tax (Regular Tax and BEAT Minimum Tax) |

$63

($300 X .21) |

$130

($1,300 X .1) |

|

BEAT |

|

$67

($130 - $63) |

Developments in the Outbound Sphere

Although outbound taxation of U.S. persons (i.e., the taxation of U.S. residents on income from investments outside the United States) is not the focus of this alert, there are certain outbound developments under the Act that will have a significant and counterintuitive impact on foreign corporations. As a result, tax practitioners outside the United States will want to be aware of such considerations.

CFC Status and Anti-Deferral

Certain anti-deferral rules have long applied to U.S. persons who hold, directly or indirectly, at least 10% of the stock of so-called "controlled foreign corporations" ("CFCs"). For these purposes, a CFC exists if more than 50% of the stock of a foreign corporation is held by U.S. persons who each hold at least 10% of such stock. To the extent a CFC exists, the 10% U.S. shareholders must pay tax on certain income of the CFC, called "subpart F income." Subpart F income, in turn, includes most types of passive income as well as income sold or produced by related parties that is not taxable in the CFC's resident jurisdiction. A new income category, global intangible low-taxed income ("GILTI"), would be subject to rules similar to the subpart F rules if the income of the CFC both (1) exceeds a routine return on investment and (2) is considered to be "low taxed."

The rules governing CFC status are complicated, and different rules apply for purposes of determining whether a CFC exists versus which members of a CFC must pick up subpart F income once the CFC is identified. Constructive ownership (i.e., ownership through attribution by or for shareholders) applies for purposes of identifying a CFC, whereas only direct and indirect ownership applies for purposes of having subpart F income.

Prior to the Act, there was an important limitation on constructive ownership—specifically, a U.S. corporation could not be treated as constructively holding stock held by a non-U.S. corporation. Under the Act, this rule has been removed, and as a result, CFC status will exist in many cases that are less than obvious.

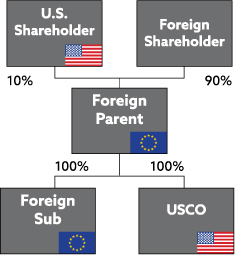

Example

The example below shows a situation in which CFC status will apply after the Act, although it would not have under prior law. Assume Foreign Parent and Foreign Sub are both E.U. companies treated as corporations for U.S. tax purposes and that Foreign Parent holds 100% of the stock of both USCO and Foreign Sub.

-

Pre-tax reform: USCO is not treated as holding the stock held by Foreign Parent because Foreign Parent is not a U.S. person. Therefore neither Forent Parent nor Foreign Sub is a CFC.

-

Post-tax reform: USCO is treated as holding all of the shares held by Foreign Parent for purposes of identifying CFC status. Therefore, Foreign Sub (but not Foreign Parent) is a CFC.

-

USCO will not have subpart F inclusions with respect to Foreign Sub, but if there are any 10% U.S. shareholders in Foreign Parent (such as U.S. Shareholder), such shareholders could unwittingly have subpart F inclusions in the future by virtue of indirect ownership in Foreign Sub, a CFC.

Where CFC status exists, direct and indirect U.S. owners may have subpart F income inclusions.

Mandatory Inclusion

As a toll charge for transitioning to a more territorial system, the Act imposes a one-time mandatory inclusion for certain so-called deferred foreign income corporations ("DFICs"), which includes both CFCs and certain foreign corporations held by at least one 10% (or greater) U.S. corporate shareholder. Under the provision, the subpart F income of the applicable DFIC is increased by the greater of (1) accumulated post-1986 deferred foreign income of such corporation determined as of November 2, 2017, or (2) the accumulated post-1986 deferred foreign income of such corporation determined as of December 31, 2017.

There can be little doubt that the central focus of this provision was to address the widely publicized issue in the United States of trapped offshore earnings and profits, under which the prohibitively high U.S. corporate rate incentivized U.S. multinationals to leave earnings in offshore lower-tax subsidiaries, thereby gaining a deferral benefit rather than paying current U.S. tax. It was widely reported that this issue has led to as much as almost three trillion dollars being "locked out" of the U.S. tax base. The mandatory inclusion has impacted the recently reported earnings of many large U.S. corporations.

Since the enactment of this rule, many of these U.S. multinationals (such as Apple, for example) have already announced that they will repatriate billions of dollars to the United States and, in a many cases, use these funds to increase compensation of employees or for capital investment in U.S. operations. Recognizing that the tax on the repatriation is mandatory, once paid, there is little reason to keep the cash outside the United States.

Exemption for Dividends from Foreign Sources

Under new Code section 245A, the United States introduces its own participation exemption, similar to many of the participation exemption regimes undoubtedly familiar to tax practitioners in the European Union. Under the new participation exemption regime, 10% (or greater) corporate shareholders of DFICs are exempt from U.S. corporate tax on dividends from such DFICs to the extent such dividends are paid out of foreign-sourced earnings. Similarly, capital gains on the sale of stock in DFICs that are also CFCs may also qualify for the exemption to the extent the amount of capital gain does not exceed the amount of the undistributed earnings of such subsidiaries.

No foreign tax credits are permitted with respect to dividends eligible for the participation exemption. Similarly, dividends that give rise to a deduction in jurisdiction of the foreign payor will not qualify.

Other Miscellaneous Points

Non-U.S. taxpayers dealing with the United States may also want to note the following additional points with respect to the Act:

Retention of the Popular "Check-the-Box" Entity Classification Election

The uniquely American entity classification election procedure known as the "check-the-box election" survives the Act unscathed. The check-the-box election allows taxpayers to determine whether certain entities not otherwise treated as "per se corporations" under U.S. law are to be treated as fiscally transparent (i.e., a partnership or disregarded entity) or as fiscally opaque (i.e., a corporation) for U.S. tax purposes. The election survives notwithstanding some pointed criticism it has received during recent years—namely, that the election can be used as a mechanism for tax avoidance. For example, check-the-box elections have been used in the past to prevent the application of the subpart F income rules (discussed above) in certain cases, or to generate stateless income through the creation of so-called "hybrid" entities.

The Act seems to reflect a determination that with the advent of the BEAT and GILTI income categories as a backstop to prevent some of these perceived abuses, as well as the limitations on the dividend exemption, there was no need to dispense with the popular election and the certainty it provides taxpayers as to entity classification status. In any event, taxpayers can continue to check the box into the future.

No Border Adjustment Tax (BAT)

The initial version of U.S. tax reform advanced by the House of Representatives on November 2 proposed a "border adjustment tax" ("BAT") as a special excise tax on payments by U.S. corporations to related foreign parties. Under this provision, payments (other than interest expense) from a U.S. corporation to a related foreign corporation that are deductible, includible in cost of goods sold, inventory, or includible in the basis of depreciable or amortizable assets, would be subject to a 20% excise tax unless the related foreign entity elected to treat such payments as income effectively connected with a U.S. trade or business. To the relief of many, the BAT was not adopted in the Act. It appears that the BEAT, discussed above, encompasses much of what the original BAT intended to accomplish.

Conclusion

U.S. tax reform is here, and tax advisors in the United States have only begun to scratch the surface of its wide-ranging effects. Simply put, non-U.S. taxpayers will need to carefully review their international organizational structures to ensure that they are optimally positioned for continued tax-efficient inbound investment into the United States.