Introduction

The year 2023 witnessed a recovery in the cryptocurrency and digital assets market corresponding with fewer crypto-related securities class action litigation actions than in 2022. Despite this decrease, the nature of the allegations made by plaintiffs in 2023 remains similar to those in previous years. The fallout from the collapse of several major market players in late 2022 also featured prominently in some cases. This article explores the key trends in 2023’s crypto-related securities class action litigation, including the decrease in the number of cases filed, the geographical distribution of the cases, the types of defendant companies and allegations, the impact of stock or asset price drops, and remaining legal questions.

2023 Decrease in Cases Filed Correlates with Crypto Market Recovery

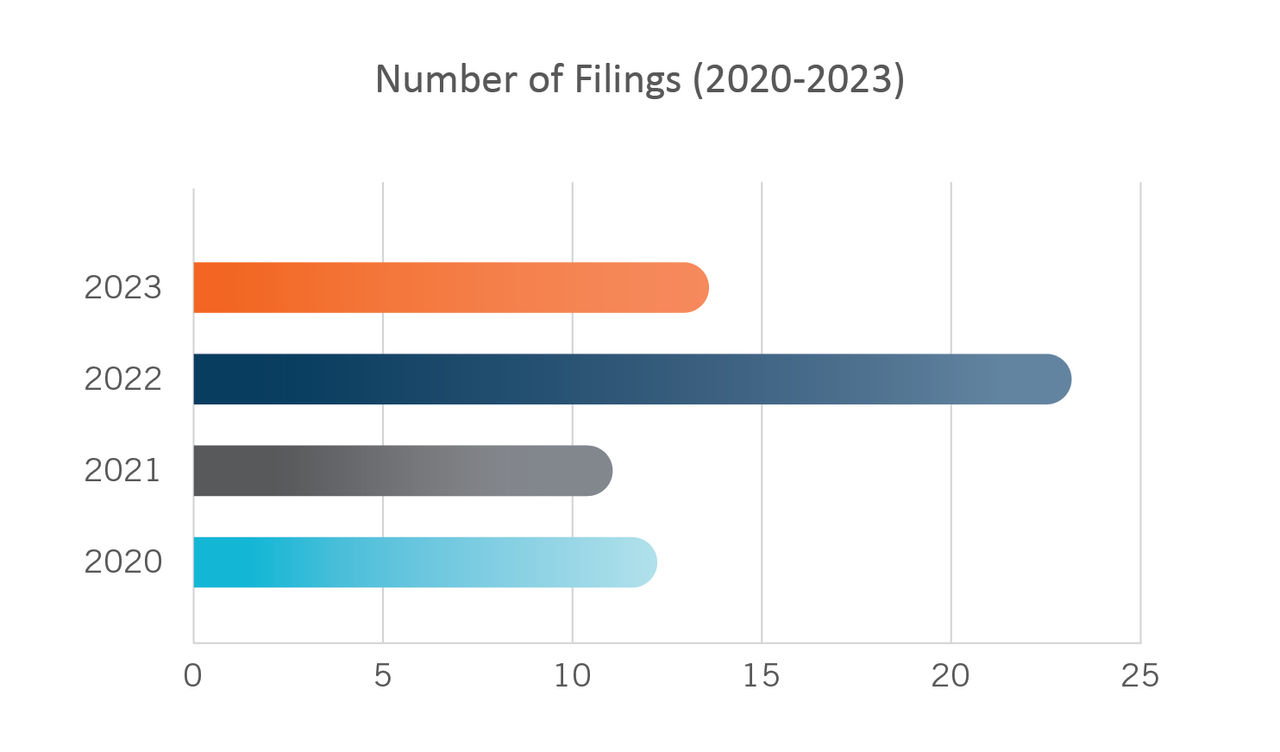

In 2023, there was a significant drop in crypto securities class action filings, a stark contrast to the record-breaking surge in 2022. Amidst the turbulence of the crypto market in 2022— which ended with the collapse of FTX, one of the world’s largest cryptocurrency exchanges—a total of twenty-three class actions were filed. This was a substantial increase from the thirteen and twelve cases filed in 2020 and 2021, respectively.1 However, with the recovery of the crypto market in 2023, the number of class action filings fell to fourteen, which is consistent with the trends observed prior to the 2022 bear market. The 2023 decrease in litigation likely corresponds to the recovery of the crypto market in 2023 after months of uncertainty in 2022.2

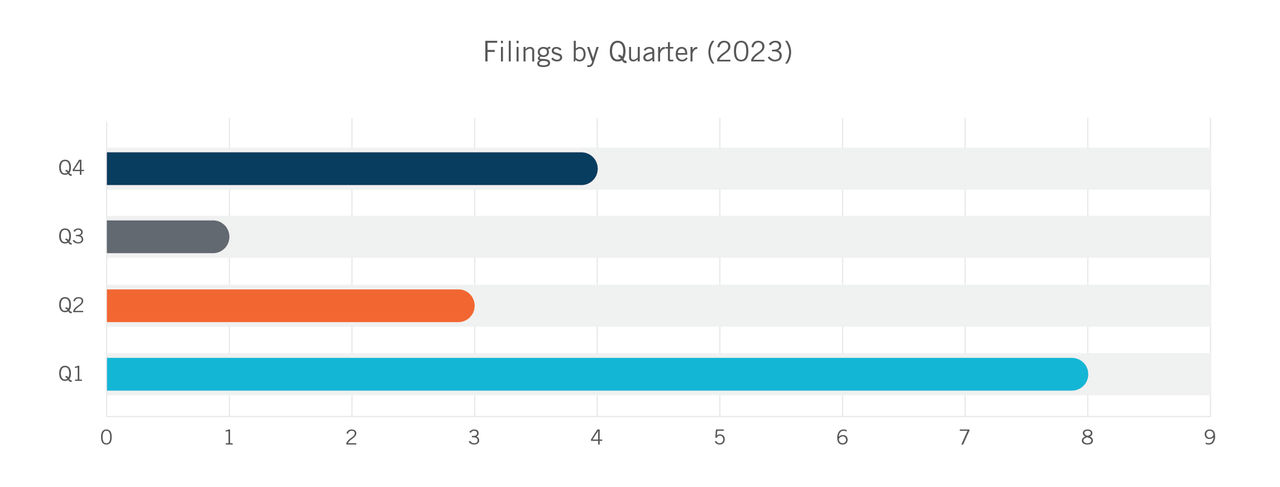

Of the fourteen securities class action cases filed in 2023, most were filed in Q1 of the year. Quarterly, the cases included:

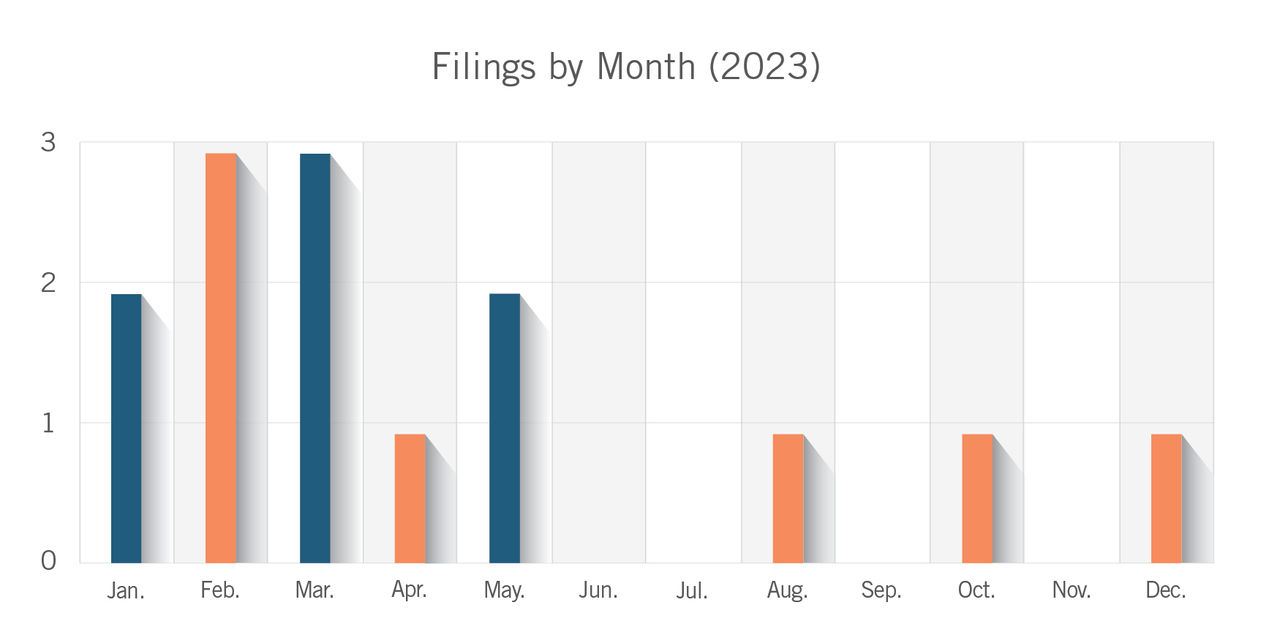

While most actions were filed at the beginning of the year, no one month predominated over all the others. The month-by-month breakdown includes:

- January: 2

- February: 3

- March: 3

- April: 1

- May: 2

- June: 0

- July: 0

- August: 1

- September: 0

- October: 1

- November: 0

- December: 1

Interestingly, most of the crypto securities class action litigation for 2023 occurred in the aftermath of the late 2022 crypto meltdown, with a decrease in such litigation as crypto prices rallied in late 2023.3

Four of the complaints from 2023 involved allegations concerning companies that either themselves collapsed in the aftermath of FTX’s failure in November 2022 or were alleged to have hastened FTX’s collapse. These complaints involve Binance, BlockFi, Eqonex, and Genesis Global Capital. Two of these complaints were filed in Q1 2023, one was filed in Q2, and one was filed in Q4.

Jurisdiction of First Filed Cases

In 2023, crypto securities class action litigation cases were filed across more jurisdictions than in years past, and the Southern District of New York (S.D.N.Y.) became a particularly less-favored forum.

In previous years, such cases have predominantly been filed in federal court in California and New York.4 For instance, of the twenty-three total cases filed in 2022, almost two-thirds (fifteen total) were filed in either California or New York, and almost a quarter (five total) were filed in the S.D.N.Y. alone.

However, of the fourteen cases filed in 2023, only seven were filed in federal court in California or New York. Specifically, California had three cases filed in the Northern District of California and one case filed in the Southern District of California. New York had two cases initially filed in the Eastern District of New York while only one was filed in the S.D.N.Y.—a marked decline for the S.D.N.Y. compared to years past.5

No other single jurisdiction saw multiple crypto securities class action filings: Connecticut, Delaware, Florida, Massachusetts, Nevada, New Jersey and Texas each served as the jurisdiction for only one such case.

Of the companies that are either defendants in or central to the allegations of these fourteen cases:

- one is headquartered in the United Kingdom (Argo Blockchain)

- one is headquartered in the Cayman Islands (Binance)

- one is headquartered in Switzerland (BProtocol Foundation)

- one was headquartered in Singapore prior to its bankruptcy (Eqonex)

- one has an unknown location for its headquarters (Lido, a general partnership).

The other nine companies are or were headquartered in the United States. This may represent a modest return to litigants outside of the United States, particularly towards Asia. Crypto class action defendants in 2021 saw a similar breakdown as in 2023: in 2021, nine of twelve defendants were headquartered in North America and three of twelve defendants were headquartered in China. However, the explosion of crypto litigation in 2022 largely involved American defendants, with twenty-one of twenty-three headquartered in the United States, one in Australia, and one in Singapore. The location of defendants’ headquarters in 2022 may be an aberration, as defendants in 2023 reverted to around three-quarters U.S. headquarters, just as in 2021.

Many of the crypto securities cases filed in 2023 are still in early stages of litigation. In ten cases, class counsel and the lead plaintiff have been appointed, but in two others, the plaintiffs have made a motion for class counsel and lead counsel which the court has not yet approved. Eight pending cases have had amended complaints filed, while five pending cases have only the original complaint filed. Defendants filed a motion to dismiss in eight of the cases. Only one case from 2023 has been resolved: the complaint against Pollen Mobile,6 which was filed on August 9, 2023, and voluntarily dismissed by the plaintiff on September 15, 2023.

Types of Crypto Allegations and Defendants

Crypto securities class actions were brought against a variety of defendants in 2023, including crypto exchanges, staking platforms, lending or trading platforms, token or NFT issuers, cryptocurrency miners, and financial services companies servicing the crypto industry. As in previous years, the most common issues raised in the complaints were (1) the sale or offering of unregistered securities (i.e. those not registered with the U.S. Securities & Exchange Commission), in violation of §§ 5, 12, and 15 of the Securities Act of 1933; and/or (2) false and/or misleading statements and/or omissions/failures to make proper disclosures, resulting in alleged financial losses for purchasers or investors.

As in years past, the most common defendants in crypto-related securities class actions filed in 2023 were crypto exchanges, staking platforms, and/or lending or trading platforms (or the parent companies thereof).7 These defendants include Binance (a cryptocurrency trading platform),8 BlockFi (an offeror of high-yield accounts on crypto deposits),9 BProtocol Foundation (which controls an automated platform for trading crypto assets),10 Genesis Global Capital (a digital currency prime brokerage for qualified institutional investors),11 Eqonex (a digital assets financial services company that operated, among other product lines, a crypto brokerage and exchange),12 and Lido (an Ethereum staking platform).13 A complaint against the sports betting website DraftKings also alleged that the secondary market platform that DraftKings operated for the purchase and sale of DraftKings NFTs was an unregistered securities exchange and brokerage.14

The case against the BProtocol Foundation (the “Foundation”) is typical of complaints against crypto exchanges and similar entities. The Foundation controlled BProtocol, a crypto exchange which required liquidity to facilitate crypto transactions.15 To acquire this liquidity, the Foundation’s leadership advertised that its platform protected against loss through “impermanent loss protection,” which the Foundation’s leadership represented would allow liquidity providers to invest crypto into BProtocol and generate interest without taking on any risk.16 However, BProtocol’s platform functioned by guaranteeing payouts to investors in the form of BNT, BProtocol’s native token.17 BProtocol was always in deficit for the actual currencies invested by liquidity providers into the platform, and if too many investors tried to withdraw their liquidity at once, BProtocol was at risk of a “run” that would cause BProtocol to crumble.18 In June 2022, such a “death spiral” occurred: as more and more investors sought to withdraw their liquidity from BProtocol, BProtocol paid out more and more BNT, resulting in a collapse in value of the BNT token.19 This led the Foundation’s leadership to suspend impermanent loss protection, leading to further collapse of BNT.20

In the class action against the Foundation, the plaintiffs allege that the investments by liquidity providers into BProtocol were investment contracts within the meaning of a “security” under the Securities Act, and thus that the Foundation’s failure to register these securities violated Sections 5 and 12(a)(1) of the Securities Act.21 The plaintiffs also allege, inter alia, that the guarantees the Foundation made about the impermanent loss protection program violated Section 10(b) of the Exchange Act and Rule 10b-5 thereunder.22 Finally, the plaintiffs allege that BProtocol operated as an unregistered securities exchange and securities brokerage in violation of Sections 5, 15(a)(1), and 29(b) of the Exchange Act.23 The plaintiffs also advance certain theories of control person liability and violation of state securities law. Since first filing in May 2023, the plaintiffs in the BProtocol case have filed an amended complaint and successfully appointed class counsel and a lead plaintiff, and defendants have moved to dismiss. As of February 2024, this last motion is still pending.

Cryptocurrency mining companies were another common category of defendant for crypto securities class actions in 2023. These defendants include Argo Blockchain (a blockchain technology company focused on large-scale mining of Bitcoin and other cryptocurrencies),24 Marathon Digital Holdings (a company that mines digital assets with a focus on the blockchain ecosystem),25 and VBit Technologies (a company that offers hardware and hosting services for Bitcoin mining).26

The lawsuit filed against Argo Blockchain exemplifies a securities class action against crypto miners. Argo is a blockchain technology company focused on large-scale mining of Bitcoin and other cryptocurrencies.27 In March 2021, Argo began the process of constructing a large cryptocurrency mining facility in rural Texas, the “Helios Facility,” for a projected total cost of around US$80 million.28 In August and September 2021, Argo filed its offering documents with the SEC in advance of its September 2021 IPO.29 On September 27, 2021, after an IPO which raised approximately US$114.80 million, Argo was listed on the NASDAQ under the ticker symbol “ARBK.”30 But on October 7, 2022, less than one month after the IPO, Argo faced an imminent “cash crunch” and began selling off its recently-acquired mining machines and issuing additional stock.31 The plaintiffs allege that this caused Argo stock to drop by almost 86% from its value at the IPO.32

In the present action, a plaintiff class of purchasers of Argo securities before or around the time of the Argo IPO alleges that the offering documents contained untrue statements and material omissions, especially regarding the operation of the Helios Facility.33 They allege that Argo and certain members of its leadership are strictly liable for the misrepresentations in those documents pursuant to Sections 11 and 15 of the Securities Act.34 They also allege that Argo and certain of its leadership knowingly or recklessly misrepresented Argo’s financial position in the Offering Documents and in other capacities prior to the IPO, and that they are liable pursuant to Sections 10(b) and 20(a) of the Exchange Act and Rule 10b-5 thereunder.35 Since filing the initial complaint, the Argo plaintiffs have filed an amended complaint and successfully appointed class counsel and a lead plaintiff, and defendants have moved to dismiss. As of February 2024, this last motion is still pending.

Other securities class action litigation targeted offerors of NFTs or token issuers with allegations relating specifically to those NFTs or tokens. These defendants include DraftKings (whose DraftKings NFTs were alleged by the plaintiffs to be unregistered securities),36 Lido (whose LDO governance token was alleged by the plaintiffs to be an unregistered security),37 and Pollen Mobile (whose PCN token was alleged by the plaintiffs to be an unregistered security).38

For example, plaintiffs filed an action against the sports betting website DraftKings for claims related to the issue of the website’s DraftKings NFTs.39 These NFTs, representing images of various football, golf, and mixed-martial arts athletes, were made available for purchase and resale exclusively on the DraftKings Marketplace, DraftKings’ platform for transactions for their NFTs.40 The plaintiffs allege that these NFTs are unregistered securities, and that the DraftKings marketplace is an unregistered exchange and brokerage.41 They assert that the sale of the DraftKings NFTs violates Sections 5 and 12(a)(1) of the Securities Act, and that the operation of the DraftKings Marketplace violates Sections 5, 15(a)(1), and 29(b) of the Exchange Act.42 Since this complaint was filed, an amended complaint has been filed, a lead plaintiff and class counsel have been appointed, and defendants have moved to dismiss. As of February 2024, this last motion is still pending.

A few actions were filed in 2023 regarding financial services companies who offered services relating to cryptocurrencies. These companies include Ryvyl (a crypto company that develops, markets, and sells blockchain-based payment solutions)43 and Signature Bank (a full-service commercial bank that the plaintiffs allege recklessly expanded its liquidity risks by taking on billions of dollars of deposits in crypto).44

Finally, one case from 2023 had a unique defendant: Shaquille O’Neal.45 A group of plaintiffs allege that certain tokens and NFTs promoted and sold by O’Neal were unregistered securities, and that the sale of those tokens and NFTs violated federal securities laws.46 The first version of this complaint was filed against O’Neal alone,47 but the amended complaint also targets a group of companies of which O’Neal is alleged to be “one of the founders, main promoters, [and] main stars.”48

Stock or Crypto Asset Price Declines

In 2022, cryptocurrency securities class action litigation cases were characterized by stock or crypto asset price drops that were generally more dramatic than those seen in other securities litigation cases. This trend held true into 2023 as well, but with a twist: while many complaints alleged specific price drops in tokens or securities (as in 2022), others now involve a complete loss of value as a result of high-profile bankruptcies from November 2022 involving the collapse of FTX.49

In 2022, eleven cases – almost half of the twenty-three filed that year – alleged stock or crypto asset price drops of at least 75%, with seven of these alleging price drops of at least 90%.50 But in 2023, only five complaints – slightly more than a third of the fourteen filed last year – alleged a stock or crypto asset price drop of at least 75%. These include the Argo complaint, which alleged that Argo shares fell by almost 86%;51 the Binance complaint, which alleged that defendants’ conduct resulted in the decline of rival exchange FTX’s cryptocurrency token by 86%, causing FTX to declare bankruptcy;52 the Eqonex complaint, which alleged that defendants’ actions over the course of the class period caused Eqonex’s share price to decline from a high of US$2.15 to a low of US$0.093;53 the Pollen Mobile complaint, which alleged that the PCN token went from a secondary market value of almost 40 cents per token to being “effectively worthless;”54 and the Signature Bank complaint, which alleged that Signature Bank’s stock declined 99.81%.55

However, two additional crypto securities class actions from 2023 involve bankrupt non-parties. In the wake of the collapse of FTX, both the crypto exchange BlockFi and the crypto broker Genesis Global Capital are now bankrupt, and the suits against their officers and/or parent or related companies do not allege any specific decline in the value of any of their securities; instead, they allege complete loss of assets invested for at least some investors.56 If the complaints involving BlockFi and Genesis Global Capital are read to allege a similarly dramatic decline in the value of a security as the complaints against Argo, Binance, Eqonex, Pollen Mobile, and Signature Bank, then slightly over half of all complaints filed last year allege dramatic price drops, which is in line with the proportion of actions filed in 2022.

The remaining complaints allege either comparatively mild price drops of around 50% or less, or allege unspecified damages suffered without any particularized dollar amount for price drops of any security.

Legal Questions Remain

As in 2022, the key legal question that remains for cryptocurrency securities class action litigation is when a cryptocurrency or digital asset can be considered a security. The S.D.N.Y. attempted to provide an answer in SEC v. Ripple Labs, Inc. et al.,57 when it ruled that sales of the cryptocurrency XRP to retail investors through secondary trading platforms did not generally constitute securities transactions, but direct sales to institutional investors did. According to the court in Ripple, the nature of institutional sales themselves, as well as Ripple’s marketing of XRP and the means by which Ripple pooled the proceeds of those institutional XRP sales, contributed to the court’s classification of the institutional sales as securities transactions. By contrast, the court concluded that retail sales of XRP to public buyers were not securities transactions because the investors did not know from whom they purchased the XRP and did not have reason to be aware that they were investing in Ripple. Some commentators noted that this decision could make it much harder to bring crypto securities class actions, as the differentiation of potential plaintiffs between retail and institutional investors could make it much harder to certify a class.58 However, it is unclear whether the principle in Ripple will be followed in future cases: in SEC v. Terraform Labs, et al.,59 issued just eighteen days after Ripple, another judge in the S.D.N.Y. departed from the approach in Ripple when it declined to universally exclude cryptocurrencies sold on a public marketplace to retail buyers from being classified as securities. Instead, the Terraform court observed that the distinction that determines when a cryptocurrency sale is or is not a securities transaction should consider the totality of the circumstances surrounding the sale and not the manner of sale, institutional or retail, alone. Whether, and how, cryptocurrencies are securities thus remains an open question.

Other cases decided in the S.D.N.Y. in 2023 dodged this issue. For instance, in Underwood v. Coinbase Glob., Inc., et al., a plaintiff class alleged, among other claims, that defendant Coinbase was selling unregistered securities in violation of the Securities Act.60 Coinbase moved to dismiss on the grounds that it was not a “seller” within the meaning of the Securities Act. The court agreed, finding that Coinbase was not a “seller” because Coinbase never held title to the cryptocurrencies in the relevant transactions. In so doing, the court in that case avoided deciding whether cryptocurrencies are indeed securities.61

Conclusion

As the crypto market recovered in 2023 from its 2022 decline, the number of crypto securities class actions filed has decreased. Nevertheless, numerous actions were filed in 2023 against a variety of defendants; particularly notable are the four complaints relating to the failure of major crypto firms in November 2022. Notably, fewer cases were filed in California and New York, especially in the S.D.N.Y. As in previous years, most actions focus on allegations of sales of unregistered securities or misrepresentations in disclosure documents; the former area of law in particular remains very unsettled.

The authors would like to thank Philadelphia law clerk Jack Foley for his contributions to this report.

Footnotes

1 This article depends primarily on data from the Stanford Law School Securities Class Action Clearinghouse. Current Trends in Securities Class Action Filings, Stanford Law School Securities Class Action Clearinghouse (last accessed Feb. 14, 2024).

2 Olga Kharif and Yueqi Yang, Crypto Hedge Funds Gear Up for ‘Token Mania’ After 2023 Rebound, Bloomberg (Dec. 27, 2023).

3 Andrew Hecht, Bitcoin- Will Cryptos Continue to Rally?, Barchart (Nov. 10, 2023); Teresa Xie, Bitcoin ETF Exuberance Drives Four-Week ‘Nothing for Sale’ Rally, Bloomberg (Nov. 10, 2023).

4 According to data from 2020-2023 for filings of cryptocurrency securities class actions. Current Trends in Securities Class Action Filings, supra note 1.

5 Richard Hawes, et al. v. Argo Blockchain plc, et al. (“American Depositary Shares Securities Litigation”), 23-CV-07305 (S.D.N.Y. Jan. 26, 2023), was originally filed in E.D.N.Y. and was transferred to S.D.N.Y. on August 18, 2023.

6 Layer Zero, et al. v. Pollen Mobile LLC, et al. (“Pollen Coin Securities Litigation”), 23-CV-04023 (N.D. Cal. Aug. 9, 2023).

7 Securities Class Action Filings 2023 Year in Review, Cornerstone Research 2 (2023), “Filings involving allegations against cryptocurrency exchanges – including all five filings with multiple cryptocurrency classifications – accounted for 7 of the 14 (50%) total cryptocurrency-related filings in 2023.”

8 Nir Lahav, et al. v. Binance Holdings Limited, et al. (“Cryptocurrency Securities Litigation”), 23-CV-05038 (N.D. Cal. Oct. 2, 2023), CAC at ¶ 1. Please note that herein “CAC” refers to the “Class Action Complaint,” “ACAC” refers to “Amended Class Action Complaint,” “FACAC” refers to the “First Amended Class Action Complaint”, and “CCC” refers to the “Corrected Consolidated Complaint” for the corresponding citations.

9 Trey Greene, et al. v. Zac Prince, et al. (“BlockFi Interest Accounts Securities Litigation”), 23-CV-01165 (D.N.J. Feb. 28, 2023), CAC at ¶¶ 2, 3. BlockFi is bankrupt, so this suit is brought against, inter alia, its former executives and members of its board of directors.

10 Mislav Basic, et al. v. BProtocol Foundation, et al. (“BNT tokens Securities Litigation”), 23-CV-00533 (W.D. Tex. May 11, 2023), FACAC at ¶ 1.

11 William McGreevy, et al. v. Digital Currency Group, Inc., et al. (“Digital Asset Loans Securities Litigation”), 23-CV-00082 (D. Conn. Jan. 23, 2023), Am. Compl. at ¶ 3. Genesis Global Capital is bankrupt, so this suit is brought against, inter alia, its parent company and former executives.

12 Louis Zhao, et al. v. Eqonex Limited et al. (“Eqonex Limited Securities Litigation”), 23-CV-03346 (S.D.N.Y. Apr. 20, 2023), ACAC at ¶ 5. Eqonex is bankrupt and present in the suit as a non-party defendant; this suit is brought against, inter alia, its former executives and members of its board of directors.

13 Andrew Samuels v. Lido DAO et al. (“LDO tokens Securities Litigation”), 23-CV-06492 (N.D. Cal. Dec. 17, 2023), Compl. at ¶ 1.

14 Justin Dufoe, et al. v. DraftKings Inc., et al. (“NFTs Securities Litigation”), 23-CV-10524 (D. Mass. Mar. 9, 2023), Am. Compl. at ¶ 1.

15 BNT tokens Securities Litigation, FACAC at ¶ 4.

16 Id. at ¶¶ 6, 12.

17 Id. at ¶ 59.

18 Id. at ¶¶ 7, 91.

19 Id. at ¶¶ 180, 181.

20 Id. at ¶¶ 182, 184.

21 Id. at ¶¶ 224-227.

22 Id. at ¶¶ 235-237.

23 Id. at ¶¶ 243-245, 251-254.

24 American Depositary Shares Securities Litigation, ACAC at ¶ 23.

25 Jaime R. Moreno, et al. v. Marathon Digital Holdings, Inc., et al. (“Marathon Digital Holdings, Inc. Securities Litigation”), 23-CV-00470 (D. Nev. Mar. 30, 2023), CAC at ¶ 2.

26 Parker Pelham, et al. v. VBit Technologies Corp., et al. (“VBit Mining Contracts Securities Litigation”), 23-CV-00162 (D. Del. Feb. 13, 2023), CAC at ¶ 34.

27 American Depositary Shares Securities Litigation, ACAC at ¶ 40.

28 Id. at ¶ 63

29 Id. at ¶¶ 64-65.

30 Id. at ¶ 114.

31 Id. at ¶¶ 77-78.

32 Id. at ¶ 79.

33 Id. at ¶¶ 67, 76, 278.

34 Id. at ¶¶ 81, 92.

35 Id. at ¶¶ 257, 269.

36 NFTs Securities Litigation, Am. Compl. at ¶ 1.

37 LDO tokens Securities Litigation, Compl. at ¶¶ 104-14.

38 Pollen Coin Securities Litigation, Compl. at ¶¶ 114-20.

39 NFTs Securities Litigation, Am. Compl. at ¶ 1.

40 Id. at ¶¶ 26, 33, 34, 63.

41 Id. at ¶ 1.

42 Id. at ¶¶ 158-169, 176-196.

43 Mark Cullen, et al. v. Ryvyl Inc., et al. (“Ryvyl Inc. Securities Litigation”), 23-CV-00185 (S.D. Cal. Feb. 1, 2023), ACAC at ¶ 31.

44 Matthew Schaeffer, et al. v. Signature Bank, et al. (“Signature Bank Securities Litigation”), 23-CV-01921 (E.D.N.Y. Mar. 14, 2023), CCC at ¶¶ 10, 40. Regulators seized Signature Bank, so this suit is brought against, inter alia, its former executives and members of its board of directors.

45 Daniel Harper, et al. v. Shaquille O'Neal, et al. (“ASTRALs NFTs Securities Litigation”), 23-CV-21912 (S.D. Fla. May 23, 2023), ACAC at ¶ 18.

46 ASTRALs NFTs Securities Litigation, ACAC at ¶¶ 1, 4, 140-43.

47 ASTRALs NFTs Securities Litigation, CAC at ¶ 2.

48 ASTRALs NFTs Securities Litigation, ACAC at ¶¶ 1, 7, 19.

49 Cf. Securities Class Action Filings 2023 Midyear Assessment, Cornerstone Research 2 (2023), “As a result of last year’s cryptocurrency market turmoil and high-profile bankruptcies (e.g. FTX, Celsius Network, Voyager, BlockFi, and Genesis), cryptocurrency has come under heightened scrutiny by U.S. regulators.” (emphasizing the effect on the crypto market from several high-profile bankruptcies discussed in this article).

50 Dechert LLP, Cryptocurrency Securities Class Action Litigation 2022 Year Review 5 (March 27, 2023).

51 American Depositary Shares Securities Litigation, ACAC at ¶ 79.

52 Cryptocurrency Securities Litigation, CAC at ¶ 2.

53 Eqonex Limited Securities Litigation, ACAC at ¶ 17, 55.

54 Pollen Coin Securities Litigation, Compl. at ¶¶ 63, 72.

55 Signature Bank Securities Litigation, CCC at ¶ 25.

56 Digital Asset Loans Securities Litigation, Am. Compl. at ¶¶ 13-14; BlockFi Interest Accounts Securities Litigation, CAC, Certification Pursuant to the Federal Securities Laws, ¶ 5 (“Plaintiff’s assets are frozen and unavailable and their worth is indeterminate and being valued at zero for the purposes of estimating plaintiff’s losses here.”).

57 20-CV-10832, 2023 WL 4507900 (S.D.N.Y. July 13, 2023).

58 See, e.g. Alison Frankel, ‘Ripple’ effect from ruling in SEC crypto case could be game-changer for class action defendants, Reuters (July 14, 2023).

59 23-CV-1346, 2023 WL 4858299 (S.D.N.Y. July 31, 2023).

60 654 F. Supp. 3d 224 (S.D.N.Y. 2023).

61 See also Risley v. Universal Navigation Inc, et al., 22-CV-2780, 2023 WL 5609200 (S.D.N.Y. Aug. 29, 2023) (A case with similar facts to Underwood, which cited Underwood to conclude that the defendant was also not a seller within the meaning of the federal securities laws, thus allowing the court to avoid deciding whether or not cryptocurrencies are securities).