If your EIN will have 250 or more full-time employees in 2016 (counting each person who was full-time in any month) you’ll need next year to file your 2016 ACA Information Returns – Forms 1094-B and 1095-B or Forms 1094-C and 1095-C – electronically. But how can you know that the IRS ACA Information Returns (AIR) system will accept what you’re planning to file? That’s the subject of “Publication 5164 (Early Look), Test Package for Electronic Filers of Affordable Care Act (ACA) Information Returns (AIR) (Processing Year 2017).”

A friend once said of the javelina pigs on his south Texas ranch, “they’re ugly and stupid but, hey, they smell bad.” Similarly, Pub. 5164 is tedious and technical, but boring. If you can hire someone reliable to understand this, do. But if this falls to you, it can’t be ignored. As tough a read as it is, it’s better than last year’s and it’s absolutely essential to getting this right. Here are some highlights from its 23 pages.

The ACA Assurance Test System (AATS) will open in November 2016. The desired result of testing is to acquire a Transmitter Control Code (TCC). If you are seeking a Software Developer TCC, it will be issued in permanent testing “T” status. Issuers and Transmitters will need a Production “P” TCC. Software Developers must confirm compatibility by testing each year. As the IRS explains, “Software Developers need a new Software ID for each tax year and each ACA Information Return Type they support. The software information must be updated yearly on the ACA Application for TCC available on e-Services at irs.gov. Annual AATS testing is required for Software Developers.” Issuers and Transmitters also must test this year if you acquired for Processing Year 2016 less than all the TCC you will need for 2017. How could that happen? You might have transmitted only Forms 1094-C and 1095-C last year but this year will also need to transmit Forms 1094-B and 1095-B. If you are an Issuer or Transmitter but not a Software Developer, and if you acquired for last year all the TCCs you will need for next year, you will not need to test again; it’s optional for you. Here’s the summary table from page 8.

|

If . . .

|

And . . . |

Then

|

|

I have a completed application, but need to add a role? E.g. I am a transmitter, but I plan on developing my own software this year. |

|

Add the new role or roles to your existing application. |

|

I have a complete application with software packages for tax year 2014 or 2015. |

|

Add the new software packages for the new tax year to obtain your new Software IDs. Also update your application with any changes, e.g. new Contacts or Responsible Officials |

|

I am a commercial Software Developer creating software and selling software packages to employers and insurance issuers/carriers, |

I will transmit information for employers or insurance issuers/carriers, |

Select both the Software Developer role and the Transmitter role on your application. |

|

I am an employer or insurance issuer/carrier purchasing a software package, |

I will transmit my own information returns |

Select the role of Issuer on your application. |

|

I am an employer or insurance issuer/carrier purchasing a software package, |

I will transmit my own information returns and transmit for other employers or insurance issuer/carriers, |

Select the role of Transmitter on your application. Note: The TCC for a Transmitter can be used to transmit your own returns and others. You may not use an Issuer TCC to transmit other’s information returns. |

|

I am an employer or insurance issuer/carrier creating my own software package, or who has contracted with someone to develop a unique package for my sole use, |

I will perform the software testing with the IRS and transmit my own information returns, |

Select the role of Software Developer and Issuer on your application. |

Not so fast, though. You must register in order to apply to test. To register, you must be a Responsible Official or a Contact, which requires you to hold a position listed in this table on page 10.

|

Business Type |

Titles

|

|

Partnership and Limited Liability Partnership |

Partner, General Partner, Limited Partner, LLC Member, Manager, Member, Managing Member, President, Owner, Tax Matter Partner (TMP) |

|

Corporations, Personal Service Corporation and Limited Liability Corporations |

President, Vice President, Corporate Treasurer/Treasurer, Assistant Treasurer, Chief Accounting Officer (CAO), Chief Executive Officer (CEO), Chief Financial Officer (CFO), Tax Officer, Chief Operating Officer, Corporate Secretary/Secretary, Secretary Treasurer, Member |

|

Association, Credit Union, Volunteer Organization, State Government Agency |

President, Vice President, Treasurer, Assistant Treasurer, Chief Accounting Officer, Tax Officer, Chief Operating Officer, Chief Executive Officer (CEO), Chief Financial Officer (CFO), Executive Director/Director, Chairman, Executive Administrator/Administrator, Receiver, Pastor, Assistant to Religious Leader, Reverend, Priest, Minister, Rabbi, Chairman, Secretary, Director of Taxation, Director of Personnel, Tax Officer |

|

Sole Proprietor |

Owner, Sole Proprietor, Member, Sole Member |

You must complete the e-Services Registration online at https://www.irs.gov/tax-professionals/e-services-online-tools-for-tax-professionals. A confirmation code will be mailed to you, good for 28 days. When you get it, you log on again using that code. That gets you to the starting line.

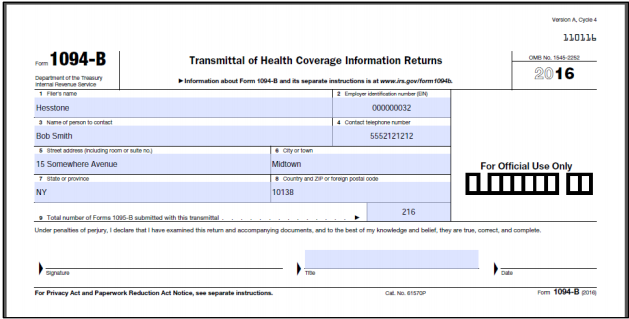

If this is all new to you, we’re not talking about an internet site for storing and sharing .pdf images of the Forms you generate and deliver to employees. The AIR system only accepts XML data. A .pdf that looks like this –

Looks like this in XML format.

Unless you’re a seasoned IT professional, you’ll need help. If you are an Applicable Large Employer Member, you should have had that help for the filing season ended June 30, 2016. If you were satisfied with that service, we still recommend that you check with your vendor about its plans and progress for Processing Year 2017 testing.

IRS CIRCULAR 230 DISCLOSURE

Thank you for your interest in our information on the current status of Affordable Care Act and its implementation. While we are happy to provide you our best information and analysis of the regulations promulgated by the Internal Revenue Service, please be advised that the contents and conclusions contained in this article and any email communication are introductory and educational in nature and do not express a formal, enforceable opinion. Nothing contained in this article and any email communication is intended to be used, or relied upon by any taxpayer for the purpose of avoiding taxation and penalties that may be imposed under the Internal Revenue Code. Any statement contained in this article and any email communication relating to any federal tax issue may not be used by any person to support the promotion, marketing of, or used to recommend any transaction for the purpose of avoiding taxation or penalties.