The IRS responded to rising inflation with its recent announcement regarding the limitations applicable to retirement and other benefit plans for 2023. Many limits will have significant increases compared to previous years, with some limits increasing by more than 10% compared to 2022. These increases could result in substantial additional savings opportunities for participants. If you have questions about how these limits could impact your organization, plans or employees, please contact your Warner attorney or a member of our Employee Benefits Practice Group.

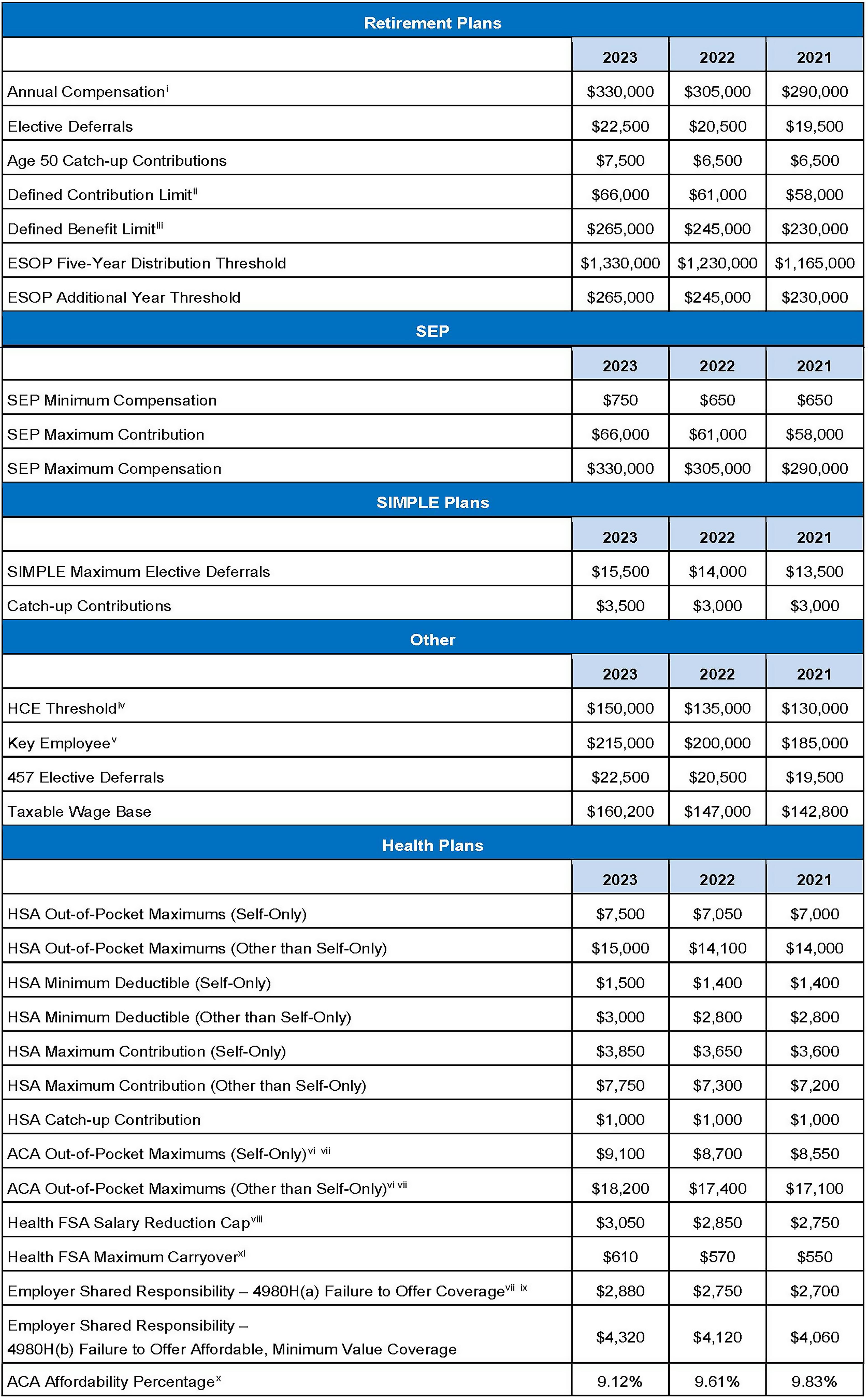

The following chart lists the common limitations. These limits are calendar year limits, except as otherwise noted.

i. The plan defines whether compensation is measured on a Plan Year or Calendar Year basis. The 2023 limit applies for the year beginning in 2023.

ii. The 2023 defined contribution limit applies to the Limitation Year, as defined by the plan, ending in 2023.

iii. The 2023 defined benefit limit applies to the Limitation Year, as defined by the plan, ending in 2023.

iv. The HCE threshold is based on prior year compensation, which can either be the preceding Plan Year or Calendar Year (“lookback year”), as elected by the plan. If the Plan Year is used, the dollar threshold is the threshold for the Calendar Year in which the Plan Year for which the compensation is measured begins. If a Non-Calendar Year plan has made a calendar year election, the lookback year is the Calendar Year beginning in the prior Plan Year.

v. The compensation used for determining whether an officer is a Key Employee is determined using the Calendar Year dollar amount in which the Plan Year begins.

vi. These limits do not apply to grandfathered or retiree-only plans.

vii. These amounts are indexed to increase based on the average per capita premium for U.S. health insurance coverage from the prior Calendar Year. The Out-of-Pocket maximum limit for self-only coverage applies to all individuals (regardless of whether the individual is in self-only or another level of coverage). For example, a family plan with an $18,200 family Out-of-Pocket limit cannot have cost sharing exceeding $9,100 for an individual enrollee in the plan.

viii. These fees apply on a Plan Year basis and are indexed for CPI-U.

ix. These fees apply on a Calendar Year basis and are assessed monthly at 1/12 of the annual amount.

x. In addition, the Patient Protection and Affordable Care Act imposes a fee to help fund the Patient Centered Outcomes Research Institute (PCORI). The PCORI fee for Plan Years ending on or after Oct. 1, 2021, and before Oct. 1, 2022, was $2.79 per person covered by the plan. The fee for Plan Years ending prior to Oct. 1, 2021, was $2.66 per person. The PCORI fee is effective for Plan Years ending before Oct. 1, 2029.

xi. The health FSA carryover maximum is indexed at 20% of the health FSA salary reduction cap.

Associate Bran Cross contributed to this eAlert.