Financial Industry Developments

CFTC’s Division of Market Oversight Extends Time-Limited No-Action Relief for SEFs from Certain Block Trade Requirements

On November 14, 2017, the U.S. Commodity Futures Trading Commission's Division ("CFTC") of Market Oversight extended time-limited no-action relief to swap execution facilities ("SEFs") from certain requirements under the definition of "block trade" in CFTC regulation 43.2. The time-limited relief to SEFs is extended until November 15, 2020. The extension will, among other things, provide the Division of Market Oversight more time to review and evaluate SEF trading practices and functionalities for pre-execution credit checks. To read the full press release, click here.

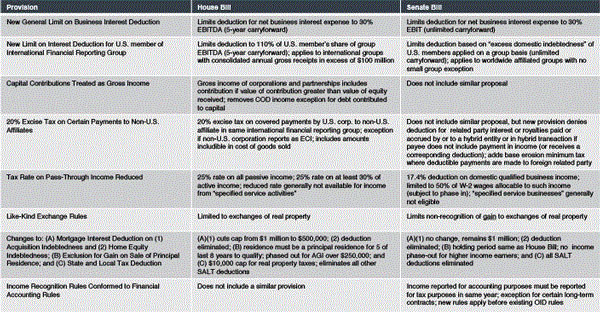

The Impact of the House and Senate Tax Bills on Financing Transactions

On November 2, 2017, House Ways and Means Committee Chairman Kevin Brady (R-TX) introduced a tax bill entitled the Tax Cuts and Jobs Act, and later proposed amendments to the bill on November 3, November 6, and November 9, 2017. The House passed the amended version of the bill on November 16, 2017. On November 9, 2017, Senate Finance Committee Chairman Orrin Hatch (R-UT) released a Senate version of the bill, and later proposed amendments to the bill on November 14, 2017. On November 16, 2017, the Senate Finance Committee approved the bill after making some last minute changes in a manager's amendment. The Senate is expected to take action on its version of the bill sometime after the Thanksgiving break. If the bill is passed by the Senate, the conference committee will attempt to reconcile the House and Senate versions of the bill. If the bill were to become law, there would be certain fundamental changes to the taxation of financing transactions.

A brief summary of the comparison of the impact of the House and Senate versions of the bill on financing transactions is available here. A more detailed version of such comparison is available here.

Impact Finance

European Commission Launches Consultation on Investors' and Managers' Duties Regarding Sustainability

On November 13, 2017, the European Commission launched a public consultation on institutional investors' and asset managers' duties regarding environmental and social sustainability. The consultation is open for responses until January 22, 2018.

The consultation is in response to a recommendation in the EU High-Level Expert Group on sustainable finance interim report published in July 2017. The interim report recommended that the Commission clarify that fiduciary duties of institutional investors and asset manages explicitly integrate material environmental, social and governance factors and long-term sustainability. The Consultation Document notes that the Commission has commenced an impact assessment process assessing how such a clarification of institutional investors' and asset managers' duties regarding sustainability could contribute to a more efficient allocation of capital and sustainable and inclusive growth.

The consultation seeks evidence from "all citizens and organizations" of how clarifications or amendments to investor duties can contribute to more efficient allocation of capital and to more sustainable and inclusive growth; of how to ensure that end investors and beneficiaries have the right information to help them make sustainable choices; and from leading responsible investors on their strategies for considering environmental, social and governance issues. Further information about the consultation, including how to respond, is available here.

OECD Development Assistance Committee Adopts Blended Finance Principles

The Development Assistance Committee ("DAC") of the Organisation for Economic Co-operation and Development ("OECD") has adopted policy guidance on the use of blended finance for development.

The guidance includes five nonbinding principles, which are described in Annex 1 to the DAC High Level Communiqué: October 31, 2017, which was published after a DAC convention on October 30 and 31, 2017. The five principles are referred to in the Communiqué as The OECD DAC Blended Finance Principles for Unlocking Commercial Finance for the SDGs. The principles are: (1) anchor blended finance use to a development rationale; (2) design blended finance to increase the mobilization of commercial finance; (3) tailor blended finance to local context; (4) focus on effective partnering for blended finance; and (5) monitor blended finance for transparency and results. The Communiqué provides additional detail with respect to each principle, including how each principle can be implemented.

In a separate publication, the OECD previously defined blended finance as "the strategic use of development finance for the mobilization of additional finance towards sustainable development in developing countries."

The Communiqué also provided guidance on how aid can be spent on refugees arriving in transit or host countries, including a list of aid-eligible and noneligible expenditures.

The Communiqué is available here.

FMO and Shell Foundation to Create Fund to Provide Capital to Social Entrepreneurs

On October 24, 2017, the Dutch development bank FMO announced that FMO and the Shell Foundation, in cooperation with the U.K. Department for International Development, will cocreate a fund to provide growth capital to social entrepreneurs.

According to a press release by FMO, FMO and the Shell Foundation signed a Memorandum of Understanding agreeing to cooperate in the field of access to energy in Sub-Saharan Africa and India. This will include investing in financial institutions with specific goals of increasing access to finance, reducing inequality, and promoting green financing and agribusiness. The growth capital fund is planned to launch in the first quarter of 2018.

The press release is available here.

Rating Agency Developments

On November 14, 2017, DBRS published its global methodology for rating finance companies. Release

On November 14, 2017, Fitch updated its U.S. RMBS seasoned, re-performing, and nonperforming loan criteria. Release

On November 13, 2017, DBRS published its methodology for rating U.S. auto lease securitizations. Release

European Financial Industry Developments

ESMA Updates MiFIR Data Reporting Q&As

The European Securities and Markets Authority ("ESMA") published an updated version on November 14, 2017, of its Q&As on data reporting under the Markets in Financial Instruments Regulation (Regulation 600/2014) ("MiFIR").

The updated version includes new answers (in section 15: transaction reporting) relating to:

-

Portfolio management

-

Swaps related to indices

-

Transaction reporting for primary issuances

-

Corporate events

ESMA Statements on ICO Risks for Firms and Investors

Following the European Securities and Markets Authority's ("ESMA") observation in rapid-growth initial coin offerings ("ICOs")s, on November 13, 2017, ESMA issued two statements on ICOs.

ESMA notes in a statement for firms that where ICOs qualify as financial instruments, it is likely that the firms involved in ICOs will be conducting regulated investment activities, whereby they need to comply with the relevant legislation, including:

-

Markets in Financial Instruments Directive (2004/39/EC) ("MiFID"). Where the coin or token qualifies as a financial instrument, the process by which a coin or token is created, distributed or traded is likely to involve some MiFID activities and services, such as placing, dealing in or advising on financial instruments.

-

Alternative Investment Fund Managers Directive (2011/61/EU) ("AIFMD"). An ICO scheme could qualify as an alternative investment fund ("AIF"), to the extent that it is used to raise capital from a number of investors, with a view to investing it in accordance with a defined investment policy.

-

Prospectus Directive (2003/71/EC) requires publication of a prospectus before the offer of transferable securities to the public or the admission to trading of such securities on a regulated market situated or operating within a member state. Also, the Prospectus Directive specifies that the prospectus should contain the necessary information that is material to an investor for making an informed assessment of the facts and that the information shall be presented in an easily analyzable and comprehensible form.

-

Fourth Money Laundering Directive ((EU) 2015/849) ("MLD4").

ESMA stresses that any failure by firms to comply with the applicable rules will constitute a breach. Firms involved in ICOs must give due consideration as to whether their activities constitute regulated activities.

A statement for investors by ESMA also alerts them of the high risk of losing all of their invested capital as ICOs are highly speculative investments. ICOs are vulnerable to the risk of fraud or money laundering.

Depending on how they are structured, ICOs may fall outside of the scope of EU law and regulations, in which case investors cannot benefit from the protection that these laws and regulations provide. Also, the price of the coin or token is typically extremely volatile, and investors may not be able to redeem them for a prolonged period.

ESMA Q&A on Trading Obligation for Shares Under MiFID II

The European Securities and Markets Authority ("ESMA") published a press release on November 13, 2017 clarifying the application of the trading obligation for shares to trade certain instruments on-venue under the MiFID II Directive (2014/65/EU).

The press release contains a Q&A about the scope of the trading obligation where there is a chain of transmission of orders. ESMA explains that Article 23(1) of the Markets in Financial Instruments Regulation (Regulation 600/2014) ("MiFIR") determines the scope of the trading obligation for shares admitted to trading on a regulated market or traded on a trading venue by requiring investment firms to ensure that trades they undertake in shares take place on a regulated market systematic internalizer, multilateral trading facility (MTF), or equivalent third-country venue.

Where there is a chain of transmission of orders concerning those shares, all EU investment firms that are part of the chain should ensure that the ultimate execution of the orders complies with the requirements under Article 23(1) of MiFIR.

The European Commission is preparing equivalence decisions for non-EU jurisdictions whose shares are traded systematically and frequently in the EU. However, the absence of an equivalence decision relating to a particular venue indicates that the Commission currently has no evidence that the EU trading in shares admitted to trading in that third country's regulated markets can be considered as systematic, regular and frequent.