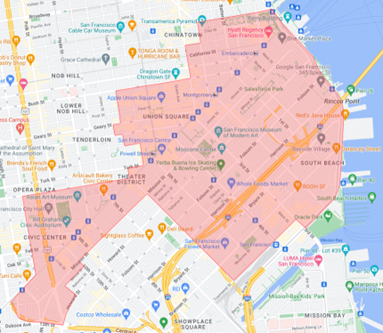

Senate Bill (SB) 1227, introduced by Senator Scott Wiener on February 15, 2024, would help speed the recovery of downtown San Francisco by creating a new CEQA exemption for qualifying commercial, institutional, student housing and mixed-use development projects in the Downtown Revitalization Zone, which includes the Financial District, Union Square, Eastern SOMA, Mid-Market, and Civic Center neighborhoods. SB 1227 would also create a new property tax exemption for moderate-income housing in the Downtown Revitalization Zone, as specified.

Map: Proposed San Francisco Downtown Revitalization Zone

NEW CEQA EXEMPTION

As currently proposed, the following requirements would need to be met to qualify for the new CEQA exemption:

- The project site must be located in the San Francisco Downtown Revitalization Zone.

- The general plan land use and zoning designations for the project site must “allow for” commercial, institutional, student housing, or mixed-uses (as specified below), as applicable to the project.

- The project must not include any hotel uses, and if residential uses are proposed, the residential square footage must be less than two-thirds the total project square footage (i.e., the project cannot be a “housing development project” already protected under the Housing Accountability Act). The foregoing square footage limitation would not apply to student housing. The residential square footage calculation must factor in (i) all projects proposed on the project site, regardless of whether they occur, and (ii) all projects developed on adjacent sites subdivided from the project site after January 1, 2024.

- To the extent that residential uses are proposed, the project must comply with applicable San Francisco inclusionary affordable housing requirements.

- The project must not require the demolition of (i) restricted affordable units, as specified; (ii) rent-controlled units, as specified; (iii) housing occupied by tenants within the past 10 years; (iv) an existing hotel that has operated within the past 10 years; or (v) a historic structure listed on the national, state, or local historic register.

- The project site must not have been used for tenant-occupied housing (i) demolished within 10 years prior to submittal of an application for the project or (ii) offered for sale to the general public by a subdivider or subsequent owner of the project site.

-

The project site must not be environmentally sensitive, e.g., a delineated earthquake fault zone, habitat for protected species, or a hazardous waste site, as defined and specified. The project site may be a prior leaking underground storage tank (LUST) site, so long as a uniform closure letter has been issued, as specified.

- The project site must not be a designated mobile home, RV or special occupancy park, as specified.

- Prevailing wage requirements would apply (unless the project consists of 10 or fewer residential units or less than 10,000 square feet), meaning that construction workers must be paid at least the general prevailing wage of per diem wages for the type of work in the geographic area (as specified), except that apprentices registered in approved programs (as specified) may be paid at least the applicable apprentice prevailing rate.

- Skilled and trained workforce requirements would apply to (i) residential projects (mixed-use or student housing) over 40,000 square feet and over 85 feet in height (as measured from grade) and (ii) non-residential projects over 40,000 square feet.

- Health care expenditure and apprenticeship requirements for construction craft employees, as specified, would apply to projects over 40,000 gross square feet.

Before making a determination that a project is exempt from CEQA under SB 1227, the lead agency must consult with California Native American tribes that are traditionally and culturally affiliated with the area, as otherwise required by CEQA.

The new CEQA exemption would remain in effect until January 1, 2035.

NEW PROPERTY TAX EXEMPTION FOR MODERATE-INCOME HOUSING

This new (welfare) property tax exemption would allow for a partial exemption equal to the percentage of the value of the property that is equal to the percentage of the number of units serving moderate-income households. As currently proposed, the following requirements would need to be met to qualify:

- The project must be located in the San Francisco Downtown Revitalization Zone.

- The project must include units “designated for use by” moderate-income households (pursuant to an enforceable and verifiable agreement with a public agency, a recorded deed restriction, or other legal document) and the rents charged must be at least 10 percent below the fair market rent for San Francisco, as determined by HUD or a market study certified by HUD.

- The project must be used exclusively for rental housing and “related facilities.”

- The project must be owned and operated by religious, hospital, scientific, or charitable funds, foundations, limited liability companies, or corporations — including limited partnerships in which the managing partner is an eligible nonprofit corporation or eligible limited liability company, meeting specified requirements — or by veterans’ organizations, meeting specified requirements.

- The funds that would have been necessary to pay property taxes must be used to maintain the affordability of, or reduce rents otherwise necessary for, the units occupied by moderate-income households.

- A building permit or site permit for the residential units on the property must be filed before January 1, 2035, and the property owner must claim the exemption within five years following the issuance of the first building permit. The new property tax exemption would also apply with respect to lien dates occurring on or after January 1, 2025.

IMPLICATIONS AND THE ROAD AHEAD

SB 1227 would be another tool in the growing toolbox available to real estate developers to encourage middle-income housing and other projects in the San Francisco Downtown Revitalization Zone. While the majority of recent local and state laws focus on housing projects, the new CEQA exemption under SB 1227 would also benefit commercial, institutional, and mixed-use developers.

As we previously reported, San Francisco recently adopted a suite of Planning Code amendments to streamline the entitlements process for housing projects and temporarily reduce applicable development impact fees and inclusionary affordable housing requirements. As we previously reported, these local efforts supplement recent state laws to facilitate housing development. Developers interested in utilizing SB 1227 (if enacted and approved by Governor Newsom) should be mindful of Assembly Bill (AB) 1287 (effective January 1, 2024), which amended the State Density Bonus Law by incentivizing the construction of housing units for the “missing middle” by providing for an additional density bonus and incentive/concession for projects providing moderate-income units, as specified. To illustrate, if the project would include 24% low-income rental units and 15% to 16% moderate-income rental units, the project would now qualify for a 100% density bonus and three to four incentives/concessions, respectively.

[View source.]