The UK market continues to prove a fertile hunting ground for shareholder activism, with US-based investors spearheading a significant proportion of public campaigns during 2023. These seasoned investors with a track record of success are increasingly turning their attention to UK plcs, and corporates should expect more of this activity in 2024.

Heightened shareholder activist focus can introduce significant disruption to the day-to-day management and business operations of targeted UK companies. However, proactively reviewing and enhancing activism defence strategies can bolster UK plcs’ preparedness and uncover opportunities amidst these challenges.

SUCCESS IN CROSSING THE ATLANTIC

Having taken root in the US, shareholder activism has firmly embedded itself in the UK’s corporate landscape. Nonetheless, American investors continue to lead the practice on the global stage and have effectively exported their trade across the Atlantic, achieving notable success for their campaigns in the UK market.

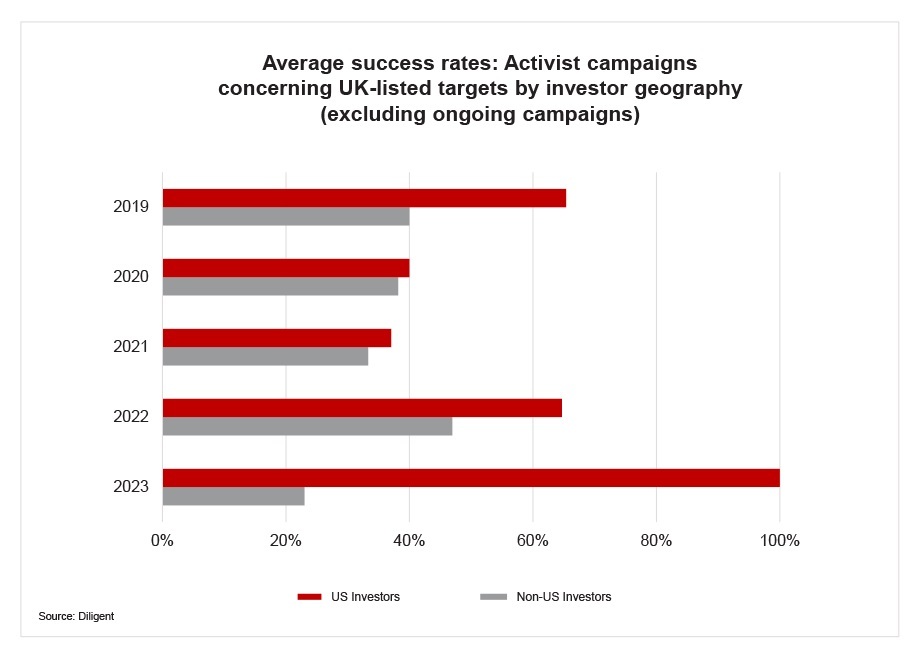

Since 2019, US-based investors have consistently outperformed their international peers in achieving higher rates of success in their public demands of UK-listed companies.

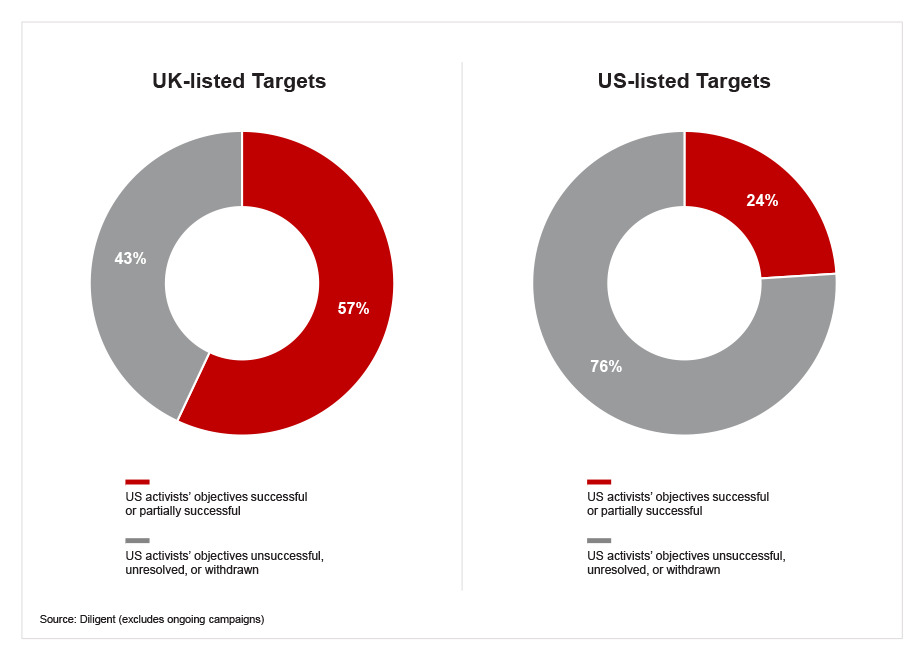

During the same timeframe, US-based investors have achieved nearly twice the success rate in their public demands of UK-listed companies compared to those listed in the US.

Numerous factors account for this, not least of which is the comparatively benign company law framework that operates in the UK and can favour shareholder activists that choose to pursue campaigns here. For example, the Companies Act 2006 equips engaged shareholders with an arsenal of tools that can facilitate the assertive and aggressive approach often favoured by US activists to publicly voice their concerns, even with relatively small shareholdings. This is most acutely felt in connection with general meetings, in which activists can utilise shareholder rights to attend meetings, pose questions of boards, and, depending on the extent of their holdings, put forward resolutions to a vote and have the target company circulate a written statement to shareholders providing context to their demands. UK public companies also do not deploy poison pills and other defensive measures that are used in the US and in a number of European countries.

The legal devices available to emboldened activist investors complement the non-legal strategies of engagement that US activists have refined over time — often in their own unique and individual styles — including conducting comprehensive press campaigns, publishing sophisticated white papers, and eliciting support from fellow shareholders.

The combination of these devices present UK plcs with novel challenges when determining how best to respond, whether through defence, negotiation, or settlement, in their interactions with US-based activists.

M&A REMAINS A DOMINANT FOCUS FOR US ACTIVISTS

Despite subdued transactional activity in the broader market during 2023, activists continued to focus on M&A-related demands as a means of unlocking value, including by agitating for company sales and divestitures of business divisions/assets, or, more frequently of late, by opposing announced deals in search of higher returns (a practice known as “bumpitrage”).

For US investors, almost a third of their public demands against UK-listed companies since 2019 have focussed on M&A objectives. This has been more pronounced recently as half of the campaigns that US investors launched against UK plcs in 2023 involved M&A-related demands. Many of these demands were coupled with complementary calls for changes at the board and management level, as part of a wider challenge on strategic direction should M&A not transpire.

Our analysis of US-led campaigns since 2019 reveals targets of varying industry and market-cap profiles. Therefore, all UK plcs should be on notice and prepare proactively for possible activist approaches from across the pond, particularly those companies with diversified portfolio businesses or which are facing depressed valuations.

Boards that are best prepared will familiarise themselves with the methods that US activists adopt in their pursuit of strategic change: using break-up valuation, conglomerate discount, and other re-rating valuation bases to push for, or oppose, transactional activity. UK plcs and their advisers can no longer wait for an activist approach before running the different analyses that show management is steering the right strategy. Boards of UK plcs must regularly consider with their management team how vulnerable they are (in particular as compared to peers) and how viable their stated strategies will be when faced with activist criticism.

BEST PRACTICE TIPS FOR UK PLCS

Ideally, shareholder activism should be addressed proactively to mitigate significant activity, including by monitoring changes in stock borrowing, trading behaviour, press coverage, investor enquiries, and website activity. Boards of UK plcs should also regularly engage with their shareholders, particularly if activists appear on their register of members, to understand the diversity of shareholder views and ensure they are being heard and considered amongst the wider interests at play. If activism does occur, preparation is crucial to effectively manage the narrative (public or private).

Many leading UK plcs undertake comprehensive activism defence reviews, including annual examination of their governance practices and evaluation of their commercial and environmental, social, and governance (ESG) vulnerabilities, considering potential lines of attack by activists. They can formulate defence manuals through these reviews, including a “break glass” action plan for a rapid response to activism, which ensures that key decisions makers understand their roles and reporting responsibilities when activists strike.

Strategic alternatives and financial implications should be regularly assessed, and plans for implementation should be developed. Importantly, strategic decisions regarding activist defence should be discussed at the full board level, as directors are likely to be the focus of any campaign. In undertaking these assessments, boards will want to demonstrate that they have been active and engaged in setting the strategic direction of the company.

Support for activism defence should extend to individual sessions with CEOs, general counsel, directors, and expert advisors to foster familiarity and confidence in dealing with activism. The ultimate goal is to align expectations and support for the company’s strategic plans, capital allocation, and earnings among principal shareholders, the board, and other key stakeholders (including institutional investors, family shareholders, and various constituents). Companies should emphasise the importance of presenting a unified voice and directing all incoming inquiries to the investor relations team to ensure a coordinated and supported response.

By implementing these strategies and maintaining a state of readiness, companies can navigate shareholder activism more effectively, protect their interests, and incorporate activism preparedness in day-to-day strategic decision-making.