A forward sale of common shares is an offering that is agreed upon today with a settlement date in the future. Forward sale agreements allow companies to capitalize on current trading prices by locking in a price at which it can sell shares to a forward purchaser – typically an investment bank – in the future. The delayed issuance provides flexibility to the issuer without a “drag on” performance measures (e.g., funds from operations) or shareholders incurring immediate economic dilution (i.e., dividends and earnings per share). These agreements are typically used to fund transactions where the timing of the closing or capital need is uncertain, including funding a transaction over time, as yet unidentified acquisitions, or future development opportunities. The transactions can also be structured to permit repayment of borrowings and for general corporate purposes. In addition to the variety of ways to use a forward sale, these agreements have a number of benefits that may be particularly attractive for REITs. These benefits are particularly useful for REITs, where the need to fund capital expenditures usually takes place over time, as opposed, for example, to a onetime acquisition cost. Additionally, these agreements protect REIT shareholders by mitigating share dilution during periods in which the capital associated with the issuance would not otherwise be put to work.

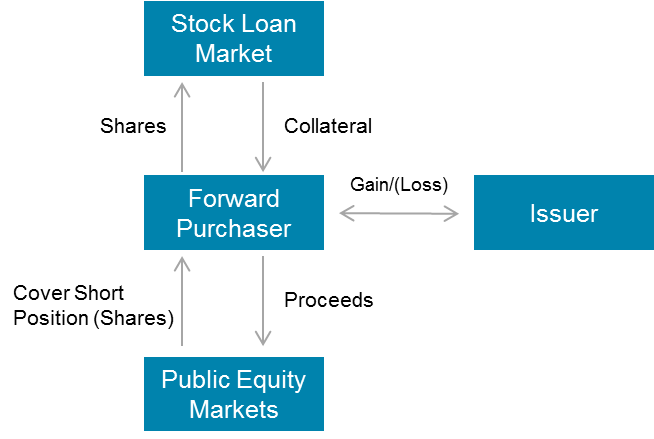

A forward sale transaction is typically structured as a public offering that is a registered transaction with the Securities and Exchange Commission. The public offering closes “regular way,” with purchasers of shares settling with the underwriters on the usual T+2 schedule. If the transaction is not paired with a simultaneous primary issuance by the issuer, no shares are actually issued by the company at the time of closing. Instead, the forward purchasers in the transaction go into the market and borrow shares to be delivered to purchasers in connection with the registered public offering.

The forward contract can then be closed out in one of two methods that allow the forward purchaser to close out its borrowing position.

1. If the company elects physical settlement, it exercises the right to sell shares to the forward purchaser at the purchase price contemplated by the contract. The forward purchaser then uses those shares to close out its borrowing position.

2. If the company elects cash or net share settlement, then there is no issuance of shares by the company and, instead the forward purchaser covers the borrowing position by making purchases in the public equity markets. If the share price at that time is greater than the purchase price fixed in the contract, then the company pays the difference to the forward purchaser. If the share price is less than the purchase price fixed in the contract, the forward purchaser pays the difference to the issuer.

Importantly, from a tax perspective it seems clear that REITs will not recognize any nonqualifying gross income under any form of settlement of a forward sale agreement. In the simplest case, where the REIT physically issues shares to the underwriter to settle the forward, no gain or loss would be recognized under section 1032 of the Code, which provides that no gain or loss is recognized on a corporation’s issuance of stock in exchange for cash or property. Even if the shares issued by the REIT have a value at delivery less than the amount paid under the forward contract, this provision should prevent any gross income from being recognized. The same result should apply if the forward contract is settled for cash. The IRS has consistently taken the view that the net cash settlement of a derivative contract with respect to an issuer’s shares should be taxed the same as physical settlement under section 1032. Accordingly, no gain or loss should result, even if no shares are issued.

Including a forward component as part of an equity strategy provides REITs with security that the equity need created by a potential investment is not only funded, but also that the need for the proceeds will match the timing for the issuance of the shares. To avoid market uncertainty, mitigate share dilution and gain flexibility, REITs may consider adding forward sale agreements to their overall capital plan.