To our clients:

We have prepared this guide to assist our clients as they prepare to implement the SEC’s new “Pay Versus Performance” (“PVP”) Rules. On Aug. 25, 2022, after a twelve-year delay, the SEC adopted rules implementing Section 953(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank Act”),[1] which added a new paragraph (v) to Item 402 of Regulation S-K. On Oct. 11, 2022, the PVP rules became effective for all companies other than emerging growth companies, registered investment companies, or foreign private issuers. Companies must begin to comply with the PVP rules in proxy and information statements that are required to include compensation disclosures under Regulation S-K Item 402 for fiscal years ending on or after Dec. 16, 2022. Smaller reporting companies (“SRCs”) also are subject to the new PVP Rules, but with certain accommodations that lessen their reporting burden compared to larger companies.

Overview

The PVP rules have three components:

- A standardized table (the “PVP Table”) that contains five years (three for SRCs) of historical compensation information as well as certain performance measures against which compensation information can be compared;

- A tabular list of the three to seven “most important” financial performance measures that are tied to executive compensation – the most important of which must be included in the PVP Table; and

- Disclosure, which can be narrative or in a graph, that describes the relationship between (a) compensation “actually paid,” which is a number that is derived pursuant to a formula in the PVP rules and listed in the PVP Table and (b) the performance measures reported in the PVP Table.

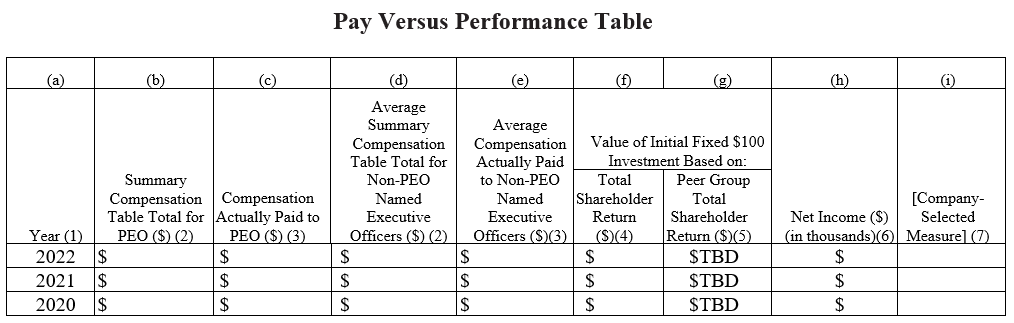

The Pay Versus Performance Table

The PVP Table must be in the required format set forth below, modified as follows:

- Although the specified table includes five fiscal years, the PVP Rules provide transitional relief that allows non-SRCs to present only three years of information in the first year of compliance, with an additional year added in each of the two subsequent years of compliance. SRCs are required to provide only two years of information in the first year of compliance, with an additional year added in the subsequent year of compliance.

- SRCs are not required to provide the information that would otherwise be included in Column (g) (Peer Group Total Shareholder Return) or Column (i) (Company Selected Measure) of the PVP Table.

The following template for the PVP Table and related disclosure contains our explanatory footnotes and/or template disclosure where appropriate.

(1) Column (a): Years Required. Subject to the transition provisions described above, non-SRCs will be required to provide information for the prior five completed fiscal years. SRCs will be required to provide information for the prior three completed fiscal years. Additionally, a company is only required to provide information for years during which it was an Exchange Act reporting company.

(2) Columns (b) and (d): Summary Compensation Table (“SCT”) Information.

- Column (b) shows the amounts for the PEO in the SCT for the applicable year.

- Column (d) shows the average amounts for the non-PEO Named Executive Officers (NEOs) in the SCT for the applicable year.

If a company has more than one PEO during a year, the company must add additional columns (b) and (c) in the PVP Table for each PEO. Also, each NEO (including the PEO) for each year must be identified in a footnote to the PVP Table.

The required footnote, depending on executive turnover, could consist of one (or a combination) of one of the following examples:

- Example 1 – no turnover: In all the years in question, XXX was our Chief Executive Officer and our remaining NEOs consisted of [list].

- Example 2 – turnover: During 2022, our Chief Executive Officers were [CEO #3 and CEO #2]. During 2021, our Chief Executive Officer was [CEO #2]. During 2020, our Chief Executive Officers were [CEO #2 and CEO #1]. During 2022, our remaining NEOs consisted of [list]. During 2021, our remaining NEOs consisted of [list]. During 2020, our remaining NEOs consisted of [list].

(3) Columns (c) and (e): Determining Compensation “Actually Paid”. Columns (c) and (e) represent the total compensation paid to NEOs for the applicable year adjusted by changes in equity award and pension plan values. These adjustments must then be disclosed in a footnote to the PVP Table. A proposed template for that footnote is set forth below.

First, the compensation “actually paid” to the PEO and the non-PEO NEOs for each year is determined by starting with the amounts set forth in the SCT’s “Total Compensation” column for the applicable year (average of those amounts for the non-PEO NEOs) and adjusting them as follows:

Pension Plan Adjustments:

Equity Award Adjustments:

- Deduct the amounts that were set forth for that year in the SCT’s “Stock Awards” and “Option Awards” columns.

- Include amounts (which could be positive or negative) for such stock awards and option awards during that year, determined as follows:

- For any awards granted during that year that, as of the end of that year, remain outstanding and unvested, add an amount equal to the fair value of those awards as of the end of that year.

- For any awards granted during that year that vested in the same year, add an amount equal to the fair value of those awards as of the vesting date.

- For any awards granted at any time before that year that, as of the end of that year, remain outstanding and unvested, add (or subtract, if negative) an amount equal to the change in fair value of those awards as of the end of the year (measured from the end of the prior year).

- For any awards granted at any time before that year for which all applicable vesting conditions were satisfied at the end of or during that year, add (or subtract, if negative) an amount equal to the change in fair value of those awards as of the vesting date (measured from the end of the prior year).

- For any awards granted at any time before that year that failed to meet the applicable vesting conditions during that year (i.e., were forfeited), subtract an amount equal to the fair value of those awards as of the end of the prior year.

- For any unvested awards on which dividends or other earnings were paid during that year that were not otherwise included in the SCT’s “Total Compensation” column for that year, add the amount of such dividends or other earnings.

- Modified Awards – If at any time during the last completed fiscal year, the exercise price of options or SARs held by a NEO has been amended or adjusted, whether through amendment, cancellation or replacement grants, or by any other means, or the award has otherwise been materially modified, the changes in fair value included pursuant to the adjustments described above must take into account the excess fair value, if any, of any such modified award over the fair value of the original award as of the date of such modification.

- “Fair value” is determined under ASC Topic 718.

- For option awards, the company must use a model consistent with the fair value methodology used to account for share-based payments in the company’s financial statements in accordance with GAAP.

- For performance awards, the company must take into account the probable outcome of the performance conditions as of the measurement date.

- Vesting Date Determination – For a time-based award, the vesting date simply is the date on which the award vests. For performance-based awards, the vesting date will depend upon whether continued service is required beyond the end of the performance period. If continued service is required, the vesting date will be after the performance period. If continued service is not required, the vesting date will be the last date of the performance period, which will be 12/31 for performance periods tied to a calendar year. Deferred awards are treated as vested in the year of vesting rather than the year of payment. For awards with retirement vesting, the vesting date should be confirmed following a review of the applicable award agreement.

Footnote Disclosures to PVP Table – As mentioned above, the rules require that the PVP Table be accompanied by footnote disclosure of the adjustments described above that are made to arrive at compensation “actually paid” to the NEOs for each year represented in the PVP Table. The footnote, with respect to the amounts added relative to stock and option awards, must disclose material changes (including changes in the probability of achievement of performance awards from year to year) in assumptions made in the calculation of fair value from those disclosed as of the grant date of such equity awards.

For clarity, a separate table may be required. Such a footnote could appear as follows [NOTE - omit rows with respect to adjustments that are not applicable to a particular company]:

[FN] The following tables set forth the adjustments made during each year represented in the PVP Table to arrive at compensation “actually paid” to our NEOs during each of the years in question:

(4) Column (f): Company Total Shareholder Return (“TSR”). These returns are calculated in a similar – but not identical – manner to how they are calculated in the performance graph that is required by Item 201(e) of Regulation S-K and generally found in the company’s annual report to shareholders required by Exchange Act Rule 14a-3(b) or the company’s Annual Report on Form 10-K (the “Performance Graph”). The calculation for each year is based on a fixed investment of $100 from the beginning of the earliest year in the PVP table through the end of each applicable year in the table, assuming reinvestment of dividends. For most companies, the calculation will begin at Dec. 31, 2019 and extend through Dec. 31, 2022. In subsequent years, 2023 and 2024 will be added so that for all companies other than SRCs, the PVP Table will include five years of data. Thereafter, each year, the oldest year will drop off and the most recent year will be added.

(5) Column (g): Peer Group TSR. In this column, which is not required for SRCs, a company may use either the same peer group or published industry line of business that it uses in presenting the Performance Graph or the one it uses in its CD&A for purposes of disclosing benchmarking practices in compensation – and note, that to use the one that is used in the CD&A, it must be used for “benchmarking” – not merely for comparison.

The company must make the calculation in the same manner as that used in Column (f) for Company TSR (i.e., beginning with an initial $100 investment). The company must also use the same methodology in calculating both the company’s TSR and that of the peer group. Also, companies may not use the broad equity market index (i.e., S&P 500) used in the Performance Graph. If the peer group is not a published industry or line-of-business index, the identity of the issuers composing the group must be disclosed in a footnote. The returns of each component issuer of the group must be weighted according to the respective issuer’s stock market capitalization at the beginning of each period for which a return is indicated. If the company selects or otherwise uses a different peer group from the peer group it used for the immediately preceding fiscal year, it must explain, in a footnote, the reason(s) for this change, such as “we removed company X from our peer group because [it is no longer public, went bankrupt, its market cap is no longer representative, etc.] and we added company Y.” The company must also compare the company’s TSR with that of both: (a) the newly selected peer group; and (b) the peer group used in the immediately preceding fiscal year.

(6) Column (h): Net Income. In this column, provide the company’s net income for each year in the PVP table.

(7) Column (i): Company Selected Measure. In this column, which is not required for SRCs, the company must designate a financial measure (the “Company-Selected Measure”) from the Tabular List (see “Pay Versus Performance – Tabular List of Most Important Financial Performance Measures” below), which in the company’s assessment represents the most important financial performance measure (that is not otherwise required to be disclosed in the table – e.g., TSR) used by the company to link compensation actually paid to the company’s NEOs for the most recently completed fiscal year to company performance. The company must then report for each year in this column the numerically quantifiable performance of the company under the Company-Selected Measure.

Companies that do not use any financial performance measures to link executive compensation actually paid to company performance, or that only use measures already required to be disclosed in the table, would not be required to disclose a Company-Selected Measure or its relationship to executive compensation actually paid. For purposes of this disclosure, “financial performance measures” means measures that are determined and presented in accordance with the accounting principles used in preparing the issuer’s financial statements, any measures that are derived wholly or in part from such measures, and stock price and TSR. A financial performance measure need not be presented within the company’s financial statements or otherwise included in a filing with the SEC to be a Company-Selected Measure. Disclosure of any Company-Selected Measure, or any additional measure that the company elects to provide, that is a non-GAAP financial measure will not be subject to Regulation G or to Item 10(e) of Regulation S-K. Nevertheless, the company must provide disclosure as to how it calculated such a measure from the company’s audited financial statements. That disclosure may resemble a reconciliation table that the company might otherwise have used to comply with Regulation G or S-K Item 10(e)).

Pay Versus Performance Relationship Disclosures

Companies must use the information in the PVP Table to provide a “clear description” (graphically, narratively or a combination of the two) of the relationship over each of the years in the PVP Table between the compensation “actually paid” to the PEO and the average compensation “actually paid” to the non-PEO NEOs (columns (c) and (e) of the PVP Table) to each of the following metrics:

- The company’s cumulative TSR (column (f) of the PVP Table);

- The peer group cumulative TSR (column (g) of the PVP Table, which is not required for SRCs);

- The company’s net income (column (h) of the PVP Table)); and

- The “Company-Selected Measure” (column (i) of the PVP Table) and any additional measure that the company elects to provide in the PVP Table (not required for SRCs).

The descriptions described above must also include a comparison of the company’s cumulative TSR (column (f) of the PVP Table) and peer group cumulative TSR (column (g) of the PVP Table) over the same period.

Pay Versus Performance – Tabular List of Most Important Financial Performance Measures

Companies, other than SRCs, must provide a tabular list of at least three, and up to seven, financial performance measures (the “Tabular List”), which in the company’s assessment represent the most important financial performance measures the company used to link compensation that it actually paid to the company’s NEOs, for the most recently completed fiscal year, to company performance. The company may provide the Tabular List disclosure either as one list, as two separate lists (one for the PEO, and one for all NEOs other than the PEO), or as separate lists for the PEO and each NEO other than the PEO. If the company elects to provide multiple lists in accordance with the immediately preceding sentence, each list must include at least three, and up to seven, financial performance measures, which in the company’s assessment represent the most important financial performance measures the company used to link compensation that it actually paid to that particular NEO, or those NEOs, as applicable, for the most recently completed fiscal year, to company performance.

If a company, for the most recently completed fiscal year, used fewer than three financial performance measures to link compensation actually paid to the company’s NEOs to company performance, the Tabular List must include all such measures that the company used, if any. A company may include in the Tabular List non-financial performance measures (i.e., performance measures other than those that fall within the definition of financial performance measures) that it company used, during the most recently completed fiscal year, to link compensation actually paid to the company’s NEOs to company performance, if it determines that such measures are among its three to seven most important performance measures, and it has disclosed its most important three (or fewer, if the company only uses fewer) financial performance measures, as described above.

The financial performance measure that the company deems to be the most important is the one that must be added to the PVP Table as the Company Selected Measure (column (i) to the SVP), together with the values (e.g., dollars or if a ratio, perhaps a percentage) indicating achievement of that measure reported for each year. Other than identifying the most important measure as the Company-Selected Measure in the PVP Table, the measures in the Tabular List are not required to be ranked.

Pay Versus Performance – Format and XBRL

The PVP disclosures disclosure must appear with, and in the same format as, the rest of the disclosure required to be provided pursuant to Item 402 of Regulation S-K (i.e., executive compensation disclosure) and, in addition, must be provided in an Interactive Data File in accordance with Rule 405 of Regulation S-T and the EDGAR Filer Manual.

Pay Versus Performance – Smaller Reporting Companies

An SRC may provide the PVP information for three (two in the first year of disclosure) years, instead of five years. An SRC is not required to provide the peer group TSR disclosures, the Company-Selected Measure disclosure, or the Tabular List. For purposes of calculating compensation “actually paid” in columns (c) and (e) of the SVP Table, SRCs are not required to disclose amounts relating to pension benefits. An SRC is not required to comply with the XBRL requirements described above until the third filing in which it provides PVP disclosure.

Pay Versus Performance – Filed Status

Although the PVP disclosures are “filed” (and therefore subject to liability under Section 18 of the Exchange Act) rather than “furnished,” they will not be deemed to be incorporated by reference into any filing under the Securities Act or the Exchange Act, except to the extent that the company specifically incorporates them by reference. Accordingly, unless incorporated by reference into a Securities Act registration statement, the PVP disclosures will not be subject to liability under Section 11 of the Securities Act. The Commission noted that while subjecting these disclosures to Exchange Act Section 18 “may create an incremental risk of litigation, . . . Section 18 does not provide for strict liability with respect to ‘filed’ information.”

What You Need to Do Now

Most importantly, START PREPARING — NOW! The PVP disclosures will be required in proxy statements that include executive compensation disclosures for fiscal years ending on or after Dec. 16, 2022 — i.e., for most companies, during the 2023 proxy season.

As soon as practicable, engage with the right constituencies to make some basic determinations – the composition of the “Tabular List,” the selection of the “Company-Selected Measure” and the selection of the company peer group.

- Compensation committees, compensation consultants, actuaries, valuation and legal advisors and other internal constituencies (HR, accounting and finance) all should be aligned on steps necessary to create the PVP disclosures.

- The new disclosures require companies to make subjective assessments of the “most important” performance measures to include in the “Tabular List” and, from this list, to identify the “Company-Selected Measure” to be included in the new PVP Table. These may be new decisions for many boards and committees, adding an additional layer to the already-complex process of setting and determining executive compensation. These decisions may require significant consideration by the company’s senior management, as well as the compensation committee and the board of directors.

- Review past disclosures (e.g., CD&A) to determine the company’s past statements regarding its important performance measures. Similarly, review historical compensation committee minutes and other materials to determine whether the compensation committee has weighted these measures– either formally or informally.

- The performance metrics included in the Tabular List and the metric selected as the Company-Selected Measure are required to be financial measures. Determine whether additional non-financial metrics have been considered when determining executive pay levels. Listing non-financial metrics indicates that pay and financial performance are not always directly correlated and that qualitative performance metrics also are important in making compensation decisions.

- Identify the peer group to be used in the PVP Table. Compensation committees should carefully consider each year whether to change the companies in the compensation peer group if that peer group is used for the PVP Table, because the company will still be required to disclose the TSR of the prior peer group.

- Companies should consider whether the disclosure in its CD&A is consistent with the Company-Selected Measure set forth in the PVP Table. Presumably, that measure is the metric that the company has determined is the most important to link pay and performance and, therefore, should be the metric that most closely correlates to compensation paid to the executives.

Prepare for new or different calculations in arriving at compensation “actually paid” and in determining TSR and Peer Group TSR. The adjustments to total compensation that the company uses in determining compensation “actually paid” will require additional calculations and evaluations to complete the disclosure.

- While the fair value computations required with respect to share-based payments will use the same methodology that is used in the tables already included in the proxy statement, the compensation “actually paid” table that requires determining the values based on vesting dates and year-end dates (as opposed to grant dates) is new, and so is accounting for fluctuations in the value of grants made in prior years. Companies will need to allow additional time for their internal finance and accounting teams to understand and prepare these new valuations. This preparation may result in a complex and time-consuming process, particularly for companies that make frequent equity grants, because it will require an analysis of each grant’s initial value, vesting schedule, subsequent year-end value, any forfeitures and any dividends.

- Another challenge will be determining changes in fair value for performance awards based on the “probable outcome of such conditions as of the last date of the fiscal year.” While required on a periodic basis for financial statement reporting, projecting outcomes in compensation disclosure is uncharted territory. Companies will have to evaluate how much detail to include in their disclosures of the fair value assumptions used to derive these values versus confidentiality concerns regarding such information. For example, confidential non-public information regarding the company may have a material impact on the probable outcome of a vesting condition, and companies will have to determine whether and to what extent to disclose that information.

- Similar to the adjustments to reflect changes in equity value above, the underlying data for computing the value of pension benefits (“service cost” and “prior service cost”) likely is readily assessable; however, the calculations are new as they will apply to a subset of employees – plus, an individual’s service cost is not an item that a company would normally calculate annually. Because these calculations are new, the company’s finance team should work with actuaries to determine these amounts.

- Many companies might not have tracked historically their TSR or the TSR of their compensation peer group. Even those that have done so might not have performed the TSR calculations as required by the PVP disclosure rules. Accordingly, companies will need to perform these relatively complex calculations with respect to several prior fiscal years to satisfy their disclosure obligations.

Determine how to “clearly” disclose the relationships between pay and performance. Companies must assess the data presented in the PVP Table and decide on an approach to discuss the relationship between compensation “actually paid” and company performance (e.g., TSR, net income, and Company-Selected Measure) as reflected in the table. The new PVP rules do not mandate a particular format for this disclosure. Formats suggested in the SEC’s release include: (a) a graph providing executive compensation actually paid and change in the financial performance measure (TSR, net income, or Company-Selected Measure) on parallel axes and plotting compensation and such measure(s) over the required time period, and (b) disclosing the percentage change over each year of the required time period in both executive compensation actually paid and the financial performance measure, together with a brief discussion of that relationship. In either event, companies should be prepared to include additional narrative explanation when there is an apparent disconnect between the particular performance metric and the compensation paid to executives.

Consider preparing a mock-up of the disclosures now. Data for 2020 and 2021 that are necessary to calculate the disclosures should already be available; therefore, companies should consider creating a general mock-up of the PVP Table and related disclosures (e.g., adjustments to arrive at compensation “actually paid”). This process will help identify the persons/groups necessary to the process and will assist in determining whether relationship disclosure should be graphic, narrative, or a combination of the two. Perhaps most importantly, in this first year of compliance, it will provide an opportunity for a more focused review of these disclosures outside the ordinary (and often hurried) 10-K/proxy process.

[1] See Exchange Act Release No. 95607 (Aug. 25, 2022)