As a reminder, each registered investment adviser must file an annual updating amendment to its Form ADV within 90 days of its fiscal year end. This means an adviser with a December 31 fiscal year end will be required to file an annual updating amendment to its Form ADV by March 30, 2024. Because March 30th falls on a Saturday and IARD will have limited hours that day, we strongly encourage filers to file by March 29, 2024. We are here to help with the legal needs affecting your advisory business, including:

- Preparing and filing the annual updating amendment

- Navigating recent and upcoming regulatory changes

- Assisting with ongoing compliance requirements throughout the year

Preparing for the annual updating amendment

In the annual updating amendment, advisers must update their responses to all items in Part 1A, 1B, 2A and 2B (as applicable), including the corresponding sections of all schedules. Advisers may, but are not required to, submit amended versions of the relationship summary required by Part 3, as part of the annual updating amendment.

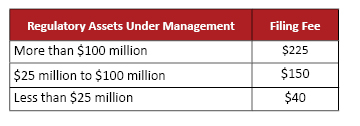

SEC-registered investment advisers must pay the fee reflected in the table below based on the amount of their regulatory assets under management. Filing fees are waived for state-registered firms.

Fees must be deposited to the firm's IARD Flex-Funding Account before the annual updating amendments may be submitted. Each firm should review their Flex-Funding Account now to determine whether it must make any deposits to their accounts—this is not something to save for the last minute as account transfers can take days. Firms may submit payments by check, wire transfer, or electronic payment/transfer. Instructions and relevant addresses are available at the following links:

Within 120 days of its fiscal year end, an adviser must deliver to each client (1) a free updated brochure that either includes a summary of material changes or is accompanied by a summary of material changes, or (ii) a summary of material changes that includes an offer to provide a copy of the updated brochure and information on how a client may obtain the brochure. This means an adviser with a December 31 fiscal year end will be required to deliver its brochure to clients by April 29, 2024.

Navigating recent and upcoming regulatory changes

Numerous regulatory changes have recently, or may soon, affect investment advisory businesses.

Effective January 1, 2024, the Corporate Transparency Act requires many entities formed or registered to do business in the United States, including certain non-SEC registered investment advisers and other entities that are not federally registered investment advisers, to submit beneficial ownership information to the U.S. Treasury’s Financial Crimes and Enforcement Network (FinCEN). State-registered investment advisers should take special note of the new requirements.

SEC Final Rules

- Private Fund Advisers; Documentation of Registered Investment Adviser Compliance Reviews, imposing new regulations on private fund advisers and requiring ALL registered advisers to document their annual review in writing.

- Amendments to Form PF, updating certain reporting requirements for private fund advisers.

- Form N-PX and Say-on-Pay Vote Disclosure, imposing changes to the information registered funds report about their proxy votes and requiring institutional investment managers to report how they voted proxies relating to certain executive compensation matters (first filings subject to the amendments due in 2024).

SEC Proposals

- Outsourcing by Investment Advisers, proposing new due diligence and monitoring requirements for advisers that outsource certain services or functions.

- Enhanced Disclosures about ESG Practices, proposing that advisers provide additional information about their environmental, social, and governance (ESG) practices.

- Cybersecurity Risk Management for Investment Advisers, proposing new policies and procedures regarding cybersecurity risks and reporting requirements on significant cybersecurity issues.

- Safeguarding Client Assets, proposing to expand the scope of the custody rule and updating related recordkeeping and reporting requirements.

- Conflicts of Interest Associated with the Use of Predictive Data Analytics, proposing to require firms to eliminate or neutralize the effect of conflicts of interest associated with the use of certain technologies.

- Privacy of Consumer Financial Information and Safeguarding Customer Information, proposing new requirements regarding policies and procedures, notifications to clients, and the scope of information covered by Regulation S-P protecting privacy of customer financial information.

SEC examination priorities include ongoing initiatives for compliance with the Investment Adviser Marketing Rule, a likely continued focus on off-channel communications and additional upcoming priorities for 2024 as published by the SEC’s Division of Examinations.

In addition, the Department of Labor (DOL) recently proposed the Retirement Security Rule redefining who is an investment advice fiduciary under the Employee Retirement Income Security Act (ERISA). DOL also proposed amendments to several existing prohibited transaction exemptions that currently provide prohibited transaction relief to investment advice fiduciaries, including the exemption financial institutions commonly rely upon in connection with rollovers.

Assisting with ongoing compliance requirements throughout the year

The number of enforcement actions brought by the SEC continues to rise, with the Division of Enforcement reporting 501 standalone actions during its 2023 fiscal year. The SEC also reported the second highest amount of monetary recoveries in SEC history for the 2023 fiscal year, totaling nearly $5 billion in civil penalties, disgorgement, and prejudgment interest. While some of these actions involve willful fraud, others are for compliance oversights as simple as failing to update the Form ADV. Taking a proactive approach to compliance can help firms avoid becoming another enforcement statistic.