On June 21, 2018, the Department of Labor (DOL) issued final regulations establishing alternative criteria under section 3(5) of the Employee Retirement Income Security Act of 1974 (ERISA) for forming single-employer association health plans (AHPs) (the Final Rule). The Final Rule makes it easier for association-sponsored Multiple Employer Welfare Arrangements (MEWAs) that offer group health coverage to be treated as a single “employer” for purposes of ERISA and treated as a single health plan. The Final Rule also establishes criteria for allowing sole proprietors and other business owners who do not have employees to qualify as employers for purposes of participating in an AHP.

This Legal Alert provides brief background on the Final Rule’s single-employer AHP criteria, and includes a chart that outlines some of the key differences between the requirements for MEWAs, single-employer AHPs established pursuant to existing guidance, and single-employer AHPs according to the alternative criteria established under the Final Rule. Future Legal Alerts on the Final Rule will provide in-depth analyses of the new AHP criteria and the key issues for employers and associations considering AHPs.

Background

The term “association health plan” is used to describe a broad range of health insurance coverage arrangements offered to individuals and/or employers through an association or a similar group or alliance. For most AHPs, the group health plan exists at the individual employer level for ERISA purposes, and the number of employees covered by each employer member determines whether an employer’s heath plan is covered under the individual and small group market reform rules under the Affordable Care Act (ACA) (such as essential health benefit requirements) or the large group market reform rules.

In order for a group of employers to come together to establish a single-employer AHP, the employers must be members of a “bona fide group or association” in which they share a “commonality of interest” beyond the provision of benefits, and they must exercise control over the administration and management of the AHP. To date, DOL advisory opinions and court decisions have applied a facts and circumstances approach to determining whether a bona fide group or association exists, but the historical conditions for establishing commonality of interest under sub-regulatory guidance have been too narrow for most associations.

The Final Rule

The Final Rule redefines the criteria for a bona fide group or association of employers capable of establishing an AHP that is a single-employer employee welfare benefit plan and a group health plan as those terms are defined in ERISA. If a group or association of employers meets the Final Rule’s new, alternative commonality of interest test, the number of employees employed by all of the employers participating in the association will determine whether coverage is subject to the small group market or the large group market rules. This approach will offer small employers and business owners the opportunity to come together and use economies of scale to offer large group market health insurance coverage to their employees.

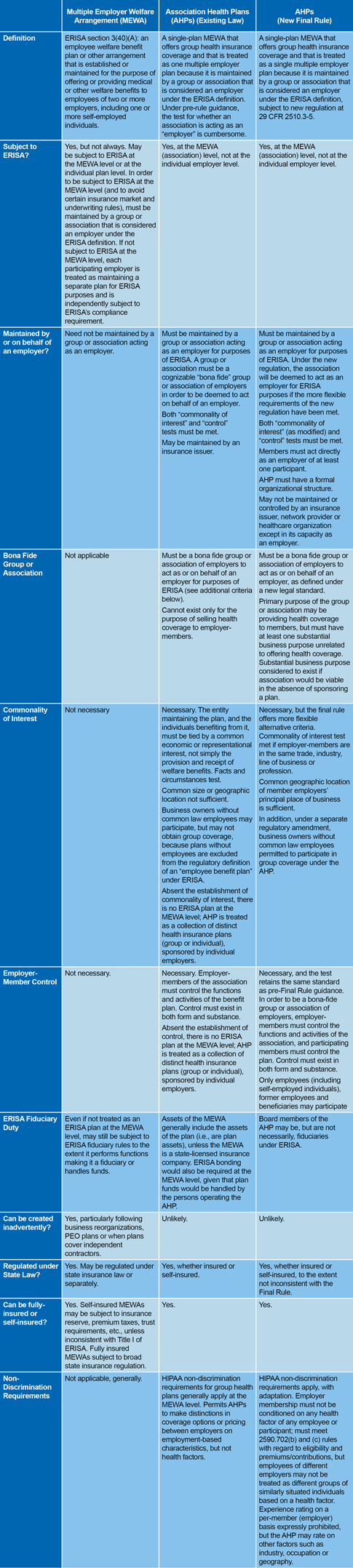

The chart below provides a high-level comparison of the characteristics of a MEWA and the criteria for a single-employer AHP under existing law and guidance, and the new, alternative criteria for establishing a single-employer AHP under the Final Rule.

Applicability Dates

For fully insured AHPs: September 1, 2018. Associations may form a fully insured single-employer AHP effective as of this date.

Existing self-insured AHPs: January 1, 2019. Associations that already maintain self-insured AHPs that comply with existing guidance, but want to expand within a geographic area or cover a particular industry, may do so as of this date. Note that existing AHPs may opt to continue to comply with the DOL’s pre-rule guidance.

For new self-insured AHPs: April 1, 2019. Associations that want to form new self-insured AHPs may do so effective as of this date.

[View source.]