The Provider Relief Fund (PRF) Reporting Portal opened for Reporting Period 2 on January 1, 2022. Recipients who received one or more General and/or Targeted PRF payments exceeding $10,000 in the aggregate from July 1, 2020 to December 31, 2020 must report on their use of funds in Reporting Period 2. The Reporting Portal for Reporting Period 2 will remain open through March 31, 2022 at 11:59 pm ET.

Period of Availability of Funds and Reporting Time Periods

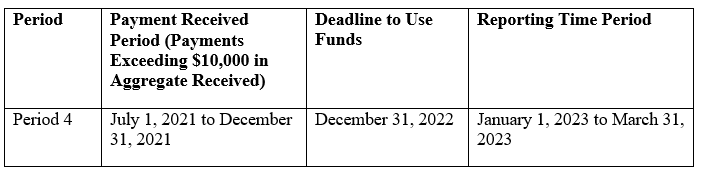

Providers are required to report on their use of funds in each Payment Received Period in which they received one or more payments exceeding, in the aggregate, $10,000, as indicated in the table below. Providers can only use payments for eligible expenses and lost revenues attributable to COVID-19 before the deadline corresponding to the relevant Payment Received Period. These deadlines are based on the date the payments are received (i.e., the deposit date for automated clearing house (ACH) payments or the check cashed date). Furthermore, reporting must be completed and submitted to HRSA by the last date of the relevant Reporting Time Period.

Reporting Period 2 Updates

If a recipient has previously reported, they may log into the Portal with their existing username, TIN, and password. (Note: New PRF Reporting Portal users must first register.) If applicable, the Reporting Portal will auto-populate previously entered data in certain fields, and recipients can edit and update any auto-populated fields. If changes are made to prepopulated data, once saved, the Portal cannot revert data back in case of error, and information must be manually re-entered.

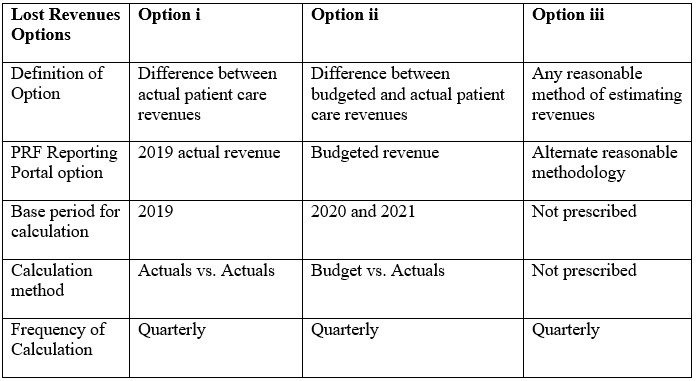

It is important to remember that the Period of Availability for Reporting Period 2 payments overlaps with payments received in Reporting Period 1. Therefore, providers will need to show how payments were applied to expenses and lost revenues from Q1 2020 through Q4 of 2021. The expenses and lost revenues for Q3 2021 and Q4 2021 must not be duplicative of those included in the Reporting Period 1 report for Q1 2020 through Q2 2021. Furthermore, returning reporting entities may change the methodology for calculating lost revenues but must then use the new methodology to calculate lost revenues for the entire Reporting Period 2 timeframe. As a reminder, there are three options to calculate lost revenues:

Updated HRSA guidance for Reporting Period 2 provides the information necessary for each option.

-

Option i: Difference between actual patient care revenues

-

Option ii: Difference between budgeted and actual patient care revenues

-

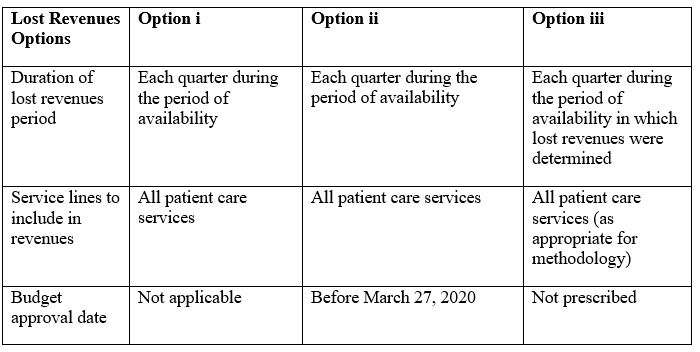

Actuals for each quarter during Period of Availability.

-

Budgets for each quarter during the Period of Availability.

-

Copy of the budget approved before March 27, 2020.

-

Executive-level attestation.

-

Option iii: Any reasonable method of estimating revenues

-

Calculated lost revenues for each quarter during the Period of Availability.

-

A narrative document describing the methodology, including an explanation of why the methodology is reasonable for the circumstances, and a description establishing how lost revenues were attributable to coronavirus (as opposed to a loss caused by any other source).

-

A calculation of lost revenues attributable to coronavirus using the methodology described in the narrative document.

Finally, returning recipients may change previously reported financial information as part of the lost revenues calculation if there was a change to their patient care revenue since the Reporting Period 1 report was filed. If changes are made to previously submitted data, providers must write a justification for the change. For providers who reported in Reporting Period 1, the Reporting Portal will calculate remaining unused lost revenues that can be reimbursed by PRF payments received during future payment periods.

More information on Reporting Period 2, including updated guidance from HRSA, is available here.