Heard Around the Industry

Status of New Loan Activity: Lender activity during the pandemic appears mixed, with approximately one-third of lenders not lending at all at the moment and the others either being cautious and conservative or pursuing higher profile deals. Lenders are adjusting and those that are still active are re-trading deals as they struggle to price their deals in the current lending climate. Lenders that are still lending are seeking deals with less “hair” that are easier to underwrite. Closing loans in the short term, however, presents its own set of challenges with the inability of lenders to conduct site inspections or for third-party due diligence to be conducted (e.g., structural inspections, environmental inspections, etc.).

Borrower Relief: Lenders are receiving temporary relief requests from borrowers impacted by COVID-19, which include: (1) requests for IO periods for loans requiring monthly P&I payments, (2) deferment of interest payments, (3) waivers of prepayment penalties, default interest and/or late fees, (4) with certain conditions, permitting subordinate debt related to government assistance programs, (5) allowing flexibility in addressing issues with tenants, (6) delaying project completion timelines, (7) providing flexibility to suspend or modify certain required reserve deposits, and (8) redirecting certain reserve funds for uses other than their designated purpose.

How to Request Relief from Lender/Servicer for COVID-19 Disruptions: If, as a result of COVID-19, you need short term relief from your lender, industry leaders have suggested certain guidelines to follow when making your request. Adhering to such guidelines will not guaranty that you will get the short term relief you are seeking (or any relief), but failure to abide by these guidelines may make your request less likely to be approved. If you are seeking assistance from your lender or servicer, please make sure to:

- If at all possible, to show good faith continue making some required loan payments (e.g., escrows, reserves, etc.) while negotiating for some relief.

- Make a reasonable request, based on the circumstances, and not merely a request to avoid payments altogether. Disclose the issues that warrant the relief requested and provide a full financial picture of the property that includes updated financial and property operating statements and projections that demonstrate the need for relief.

- Demonstrate to the lender/servicer that you are invested in the property. Provide the lender/servicer with a plan to maintain the property in the interim, as well as to deal with the economic and other issues (such as rent abatements or other incentives to retain tenants and minimize income losses at the property), as well as provide a plan for repayment of any forbearance.

Life Company Response to COVID-19: A life company servicer has advised that life companies are still evaluating the best protocol and response to the COVID-19 pandemic. Most life companies are currently handling issues on a case by case basis and responding based on the impact to a particular property. Based on this servicer’s experience and communications with some lenders, below is a list of items lenders will likely want to collect when making decisions. This servicer highly encourages borrowers to make their April mortgage payment(s) because loans that are current will likely be treated differently than loans in default.

- Year End 2017, 2018 and 2019 financials;

- YTD 2020 financials;

- Current rent roll;

- 2020 Pro-forma;

- Current balance sheet and income statement on the borrowing entity;

- YE 2019 and current balance sheet and income statement at the property level if different from above;

- Current financial statements on the primary principals of the sponsorship;

- Details of equity distributions to sponsors going forward

- Specific correspondence between the borrower and tenant(s) if applicable; and

- A write-up from the borrower, which must include (at a minimum):

- The expected impact to net operating income;

- Specific tenants that are impacted;

- When the economic impact from which the borrower is requesting relief started; and

- The specific relief requested.

Practical Solutions For Executing Documents - Electronic Signatures

Many of our clients have reached out over the last few weeks with questions about options for executing documents electronically and whether electronically executed documents (in particular promissory notes) are enforceable. Below is a summary of our findings and some practical solutions that we can offer in the new remote office environment:

Contracts and Other Documents: With the advent of secure, electronic signature platforms and mobile applications, many documents (other than recordable documents in certain jurisdictions) can be executed electronically on computers and mobile devices without the need of a printer. We can set up your documents for electronic signature and incorporate language into the document to confirm that electronic signatures are consented to and are valid and enforceable under the Electronic Signatures in Global and National Commerce Act (“E-SIGN”), and Uniform Electronic Transactions Act (“UETA”).

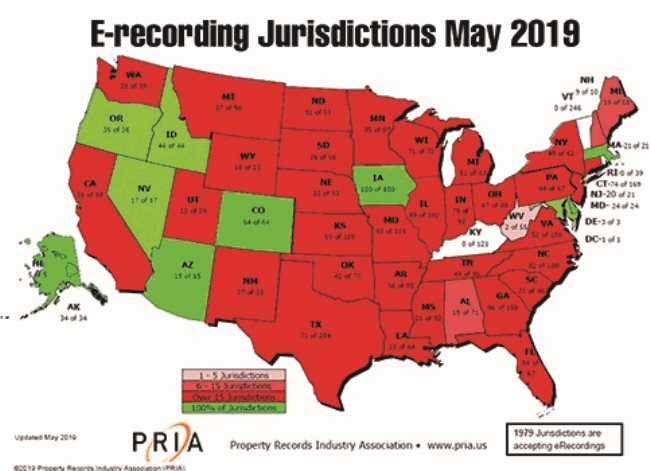

Electronic Notes and Mortgages: There is consensus within the mortgage industry that eNotes and eMortgages are enforceable nationwide (with a few exceptions for certain specific types of mortgages) under ESIGN and UETA as long as certain requirements are satisfied, and as long as (with respect to eMortgages), the recording jurisdiction permits electronic recording. For recordable documents that are acknowledged by means of a remote online notary, the state would need to accept notarizations that are not in-person. Most of the technical requirements for implementing an eMortgage are satisfied by proprietary systems referred to as eClosing and eVault systems that have been developed to execute, create, store, and deliver the eNotes. Many of these systems leverage blockchain or similar technology. We can help you coordinate the technical components and update their form loan documents to include eNote inserts and any consents required to comply with E-SIGN and UETA. Below is a map of the jurisdictions that permitted electronic recording as of last year. However, each individual jurisdiction in which documents are to be e-recorded would need to be searched to confirm the availability of, and requirements for, electronic recording.

More States Allow Mobile Notary and E-Recording

In the age of social distancing, questions arise as to how recordable documents can be acknowledged remotely without the in-person presence of a notary public. While nearly half of states allow some form of remote online notarization, the majority do not. In the wake of the pandemic multiple additional states are considering the use of mobile notarization.

Connecticut: In Connecticut, under Executive Order No. 7Q issued by Governor Ned Lamont on March 30, 2020, all relevant Connecticut state laws and regulations are modified to allow any notarial act that is required under Connecticut law to be performed using an electronic notarization process that allows a Connecticut notary public and the remotely situated signatory to communicate with each other simultaneously by sight and sound, provided certain conditions are met (see link below for a list of such conditions). Executive Order No. 7Q also eliminates all existing requirements under Connecticut law to have signatures on certain documents witnessed by a third party, except in the case of a last will and testament, which can now be witnessed remotely under the supervision of an attorney. Additional information, including the conditions that are required to be met for electronic notarizations under Executive Order No. 7Q may be found here.

DC: The District of Columbia allows notaries to apply for an endorsement to serve as an electronic notary, which allows for the electronic notarization of documents. Interested notary publics must apply to the Washington D.C. Office of the Secretary for permission to electronically notarize signatures, complete the required training course, take the required oath, identify a tamper-evident electronic device for notarizing documents, and provide copies of their electronic signature and official seal to the Office of the Secretary. Additional information can be found here.

Maryland: In Maryland, Governor Larry Hogan issued an executive order that temporarily waived the in-person requirement for notarizing documents in Maryland; provided that the notary notifies the Office of the Secretary of State of Maryland of his/her intent to use remote notarizations, identifies the communications technology vendor the notary intends to use and creates and retains an audio-visual recording of the performance of the notarial act among other requirements. Additional information can be found here.

New Jersey: In New Jersey, Measure A-3864, passed by the New Jersey State Senate and Assembly would allow remote notarization if the notary: (a) has personal knowledge of the person’s identity, (b) has evidence of the person’s identity by oath or affirmation from a credible witness, and (c) has two different types of identity. The notary would also be required to make a video of the notarial recording and retain it for 10 years. Additional information may be found here.

New York: In New York, Governor Andrew Cuomo issued an executive order permitting New York notaries to notarize via video. The video cannot be prerecorded, and the person must present valid photo identification during the video conference. Additional information may be found here.

Virginia: The ability to remotely and electronically notarize documents is permissible in Virginia. In fact, in 2011 Virginia became the first state to both recognize the legality of remote notarizations and to create the regulatory framework to enable them. Additional information can be found here and here.

U.S. Senate: Senators Mark Warner, D-V.A., and Kevin Cramer, R-N.D., introduced the “Securing and Enabling Commerce Using Remote and Electronic (SECURE) Notarization Act of 2020” into the U.S. Senate on March 18th. The legislation would make remote online notarizations legal around the country. Additional information may be found here.

No IRS Guidance for 1031 Exchanges

In light of current market volatility, real estate owners and developers are concerned about the impact COVID-19 will have on their ability to satisfy deadlines for “1031 like-kind exchanges.” The IRS has not yet provided specific guidance for 1031 transactions delated by the COVID 19 market disruption. Section 1031 of the Internal Revenue Code permits taxpayers to defer recognizing gain on certain real property by means of an “exchange” on “like-kind” investment property. There are certain requirements, such as a 45-day period from the initial sale to identify a “replacement” property, and a 180-day period from the initial sale to close on the purchase of the replacement property. With the market in flux, owners and developers have raised concerns about the ability to complete 1031 like-kind exchanges. The Internal Revenue Service in its Revenue Procedure 2018-58 (“Revenue Procedure”), permits in cases of federally declared disasters extensions of 1031 deadlines until the later of: (i) 120 days and (ii) the last day of the general disaster extension period as indicated by the IRS News Release or other guidance authorizing the Revenue Procedure to go into effect. We are monitoring developments with the Internal Revenue Service to see if similar relief is to be implemented in connection COVID 19. Additional information from the IRS, including updated to the foregoing may be found here.

Shutdown of Non-Essential New York Construction

Last week, New York Governor Andrew Cuomo reversed his decision to allow construction in New York to continue without restriction in response to the increasing number of COVID-19 cases. Under the new guidelines, only “essential” construction projects (such as roads, bridges, and health care facilities) are permitted to continue, while requiring all “non-essential” construction to cease unless cessation of work would jeopardize the health and safety of the occupants, or it would be unsafe to allow to remain undone until it is safe to shut the site. The guidelines are listed on the Empire State Development Site. Additional information may be found here.

Federal Reserve Supports the Flow of Credit to Consumers and Businesses

The Federal Reserve established the Term Asset-Backed Securities Loan Facility (TALF) to support the flow of credit to consumers and businesses by enabling the issuance of asset-backed securities (ABS) backed by student loans, auto loans, credit card loans, loans guaranteed by the Small Business Administration (SBA), and certain other assets. Under the program, the Federal Reserve will lend, on a non-recourse basis, to holders of certain AAA-rated asset based securities backed by newly and recently originated consumer and small business loans. Additional information may be found here.

CREFC and other industry groups have requested that the TALF be expanded to cover certain private label CMBS to assist with market liquidity. We will continue to monitor developments in this area.

New York to Provide Rent and Mortgage Abatement

The New York State Senate is entertaining a bill that would provide a 90-day rent abatement for any residential tenant or small business commercial tenant that has lost income or been forced to close their place of business as a result of government ordered restrictions in response to the outbreak of COVID-19. Landlords who face a financial hardship as a result of being deprived rent payments under the bill would receive forgiveness on any mortgage payments for the property for 90 days, with the amount forgiven to be determined based on the suspended rent as a percentage of the total rent. If passed, the bill would likely face constitutional challenges including a challenge as an impermissible taking under the Fifth Amendment to the U.S. Constitution. Additional information may be found here and here.

More on CARES Act

Paycheck Protection Program: The Paycheck Protection Program, which is available to small businesses with 500 or fewer employees, as well as sole proprietors, independent contractors, and others, allocates $350 billion in loans (possibly convertible to grants) to incentivize employers to retain their employees during the COVID-19 disruption, and to rehire those laid off due to COVID-19 once the situation stabilizes. Funds may be used for payroll, healthcare costs, rent, mortgage interest payments, utilities, and interest on any other pre-existing debt obligation. The maximum loan amount is the lesser of $10 million and 2.5 times the average monthly payroll during the year prior to the loan, and the maximum interest rate is 4%. These loans are available through June 30, 2020. Additional information may be found here.

Loan Forbearance for Multifamily Landlords: Owners of multifamily properties that are subject to a Freddie Mac or Fannie Mae loan may obtain up to 90-days of forbearance on their loans if their property operations were adversely affected by COVID-19. As a condition for loan forbearance, the owner must agree to not evict tenants who are adversely affected by COVID-19 (i.e., job loss, illness, reduced hours, family medical leave) during the 90 day period. Additional information may be found here.

120-Day Moratorium on Evictions: Owners of multifamily properties with federally-guaranteed loans or those participating in federal housing programs cannot seek to evict tenants, charge fees, penalties or other charges related to nonpayment of rent for 120 days from the passage of the CARES Act. Property owners must also issue a notice to tenants to vacate 30 days before an eviction and the notice to vacate cannot be issued during this 120-day period. Additional information may be found here.

[View source.]