On March 6, 2024, two years after the issuance of a proposing release and following more than 24,000 comment letters and 4,500 unique letters submitted in response, by a vote of 3-2, the U.S. Securities and Exchange Commission (“SEC”) adopted new rules with respect to climate change disclosures for publicly traded companies.[1] The rules require comprehensive discussion of material climate-related risks, identification of any climate-related goals or targets, and, for large accelerated filers (“LAFs”) and accelerated filers (“AFs”), information about Scope 1 emissions and/or Scope 2 greenhouse gas emissions (“GHG”), if material, coupled with a third-party assurance report for LAFs. The new rules also require financial statement disclosures with respect to the impact of severe weather events on a registrant’s financial results, as well, in certain cases, as disclosures related to carbon offsets and renewable energy credits or certificates (“RECs”).

The merits – and legality – of the new rules will be the subject of much debate and litigation. In fact, 10 states have already filed a petition in the Eleventh Circuit challenging the rule under the Administrative Procedures Act.[2] Undeniably, however, the rules mark an important step by the SEC toward a disclosure regime closer in line with those being implemented in Europe and elsewhere.

Rules Summary

Under the rule and form amendments adopted by the SEC, U.S.-listed public companies will be required to make annual disclosures in a new section titled “Climate-Related Disclosure” (or by cross‑reference to other sections of the issuer’s Annual Report on Form 10-K, such as the Risk Factors, Business, or MD&A), and in separate notes to the financial statements, as applicable, regarding:

- Climate-related risks, including descriptions of:

- The board’s and management’s oversight and governance of climate-related risks;

- The real or likely material impacts of climate-related risks on the registrant’s business, strategy, outlook, and financial statements;

- The registrant’s climate-related risk management process; and

- Climate-related risk mitigation, including the registrant’s transition plans and targets and goals.

- For certain large companies, if material, Scope 1 and Scope 2 GHG emissions and an attestation report for the GHG emissions.

- Additional notes to the financial statements related to:

- Specified climate-related financial statement metrics and the effect of certain weather‑related events and other natural conditions that result from or are exacerbated by climate change on the financial statements; and

- If applicable, disclosure regarding the registrant’s use of carbon offsets or RECs.

LAFs and AFs are also required to provide disclosure on Scope 1 and Scope 2 GHG emissions, if material, and to include an attestation report providing assurance on any Scope 1 and, in the case of LAFs, Scope 2 GHG emissions so disclosed from a “GHG emissions attestation provider,” which must be independent and meet certain other specified requirements but is not required to be an independent accounting firm.

The disclosure rules will also apply to companies initially conducting a public offering, and the SEC adopted similar disclosure requirements that will apply to foreign private issuers.

In response to comments, the SEC’s final rules reflect various efforts to streamline, reduce redundancy, and add materiality qualifiers in an effort to ease the reporting burdens on issuers, in addition to the following significant changes as compared to draft rules outlined in the SEC’s proposing release (the “Proposing Release”):

- No requirements to disclose the climate-related expertise of each member of the board of directors.

- No requirement to disclose and discuss climate-related opportunities.

- Climate-related risks disclosure has been pared back and simplified.

- Significant reduction of the reporting burden for GHG emissions:

- Complete removal of disclosure on Scope 3 emissions, which come from indirect sources such as supply chains or consumers.

- Limiting Scope 1 and 2 disclosure and attestation requirements to LAFs and AFs.

- Addition of materiality qualifier to Scope 1 and 2 disclosure and attestation requirements.

- No requirement to quarterly report on changes in disclosures made regarding the registrant’s climate-related risks and the impact on strategy of those risks, governance and risk management of climate-related risks, climate-related targets and goals, and GHG emissions disclosures and attestation.

- Addition of minimum thresholds for required climate-related financial disclosures.

- Expanded safe harbor provisions for certain climate-related forward-looking statements.

- Extending deadline for GHG emissions disclosures and provision of any related attestation reports until the due date for the second quarter Form 10-Q.

The SEC’s final rules do, however, reflect a few other changes that may heighten the burden on registrants as compared to the Proposing Release:

- Added a requirement to disclose any disagreements with a prior GHG emissions attestation provider.

- Added requirement to include disclosure as a note to the financial statements regarding use of carbon offsets and RECs in certain cases.

In drafting the rules, the SEC borrowed concepts from the Task Force on Climate-related Financial Disclosure (“TCFD”) framework[3] and GHG Protocol because many investors and issuers were already familiar with the concepts or using them for voluntary reporting or mandatory international reporting, and building off those reporting frameworks would thus mitigate compliance costs for those issuers and allow investors to more easily make comparisons between U.S.-listed public companies and foreign companies not subject to SEC oversight. Indeed, in finalizing the rules, certain of the SEC’s changes included revising definitions to better align them with the definitions used in the TCFD framework. However, Chair Gensler noted that the SEC’s goal was to create a framework that was tailored to U.S.-listed public companies, and in the Adopting Release, the SEC noted that “while the final rules use concepts from both TCFD and the GHG Protocol where appropriate, the rules diverge from both of those frameworks in certain respects where necessary for [U.S.] markets and registrants and to achieve our specific investor protection and capital formation goals.”

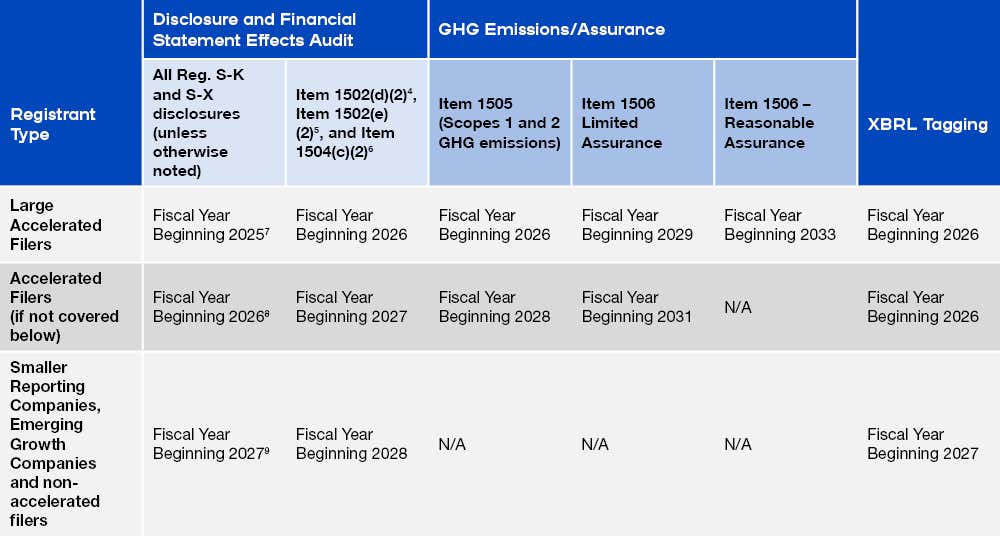

The final rules will be effective 60 days following publication of the Adopting Release in the Federal Register. The key compliance timeframe is as follows:

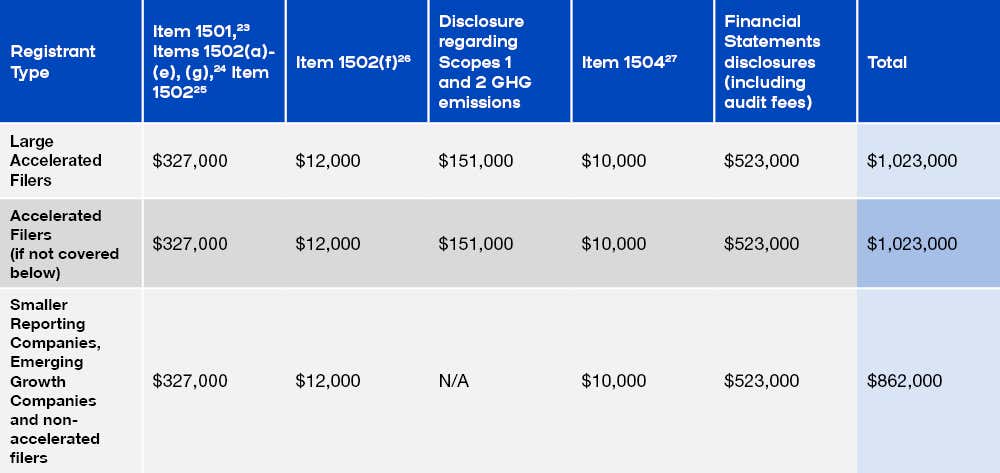

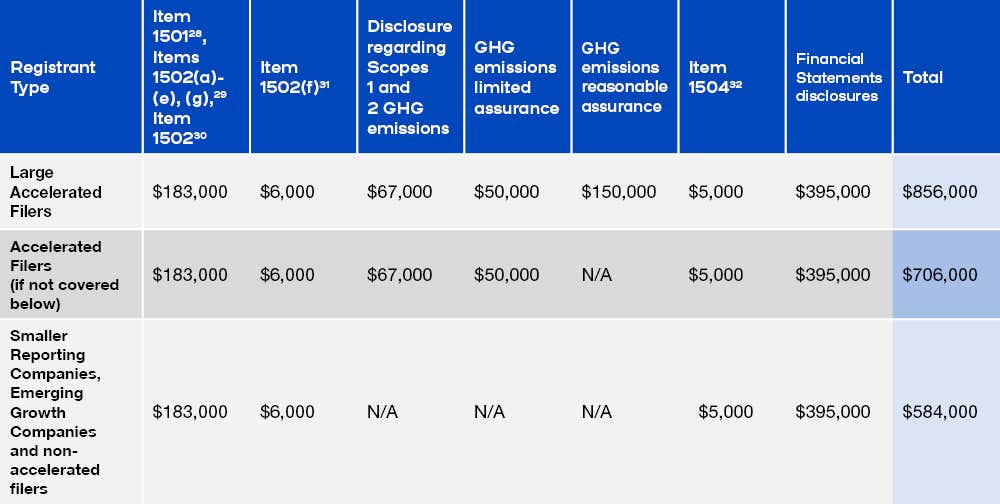

The SEC has acknowledged that there could be a considerable range in compliance costs for issuers. Depending on the registrant and disclosures they’re required to make, annual compliance costs, averaged over the first 10 years of compliance, were estimated by the SEC to range from less than $197,000 to over $739,000, with costs for the first year in particular estimated at just over $1.0 million for LAFs and AFs and $862,000 for all other filers, as summarized further below.

Key Takeaways for Public Companies

The final rules are consistent with the general SEC practice of focusing on disclosure requirements around operations and results, rather than mandating that companies adopt specific business practices. Indeed, in the Adopting Release, the SEC explicitly states that the final rules are not intended to incentivize or disincentivize, for example, the use of a transition plan or any other climate risk management tool. However, it’s a near certainty that many issuers will adopt changes to their business practices in response to the final rules, in some cases to minimize disclosure obligations and, in some cases, to avoid what could be embarrassing disclosures regarding failure to have implemented certain practices.

The SEC’s final rules requiring disclosures regarding climate-related risks, the registrant’s oversight and management of climate-related risks, and, with respect to larger registrants, GHG emissions, should prompt public companies, if they haven’t already, to:

- Review current climate-related strategies, processes, and disclosures, including any climate-related reporting that the registrant already conducts, and climate-related statements previously made by the registrant;

- Review what climate-related information is currently tracked, measured, and monitored;

- Determine who has oversight and responsibility for climate-related risks and opportunities and evaluate board oversight and responsibility for such risks and opportunities;

- Identify climate-related risks material to the registrant’s operations and financial results; and if an LAF or AF, begin determining whether GHG emissions are material to their operations and, if so, begin tracking such emissions (if not already doing so) and research, identify, and engage an attestation provider.

The final rules also reinforce the prospect of SEC enforcement risk for public companies with respect to their climate disclosures. Although the rule does not alter the long-standing materiality standard, its climate risk disclosures requirements bolster the SEC’s Division of Enforcement’s ability to scrutinize environmental risk factors to determine whether companies are disclosing ESG-related material risks, even in the absence of any ESG-related material event. As with all risk disclosures, issuers need to take care to avoid hypothetical and generic ESG-related risk disclosures if those risks have actually occurred.

Finally, issuers should be mindful that the SEC’s rules are not the only rules that may apply to them when it comes to climate-related disclosures. For example, if an issuer does business in California or the EU, it should confirm whether any of California’s climate disclosure rules[10] or the EU’s Corporate Sustainability Reporting Directive (“CSRD”)[11] apply. For companies that do, even absent the SEC’s reporting requirements, they may be required to make certain climate-related disclosures, including potentially on their Scope 3 GHG emissions, with respect to which it will be critical to ensure that they have verified data on emissions for those in their value chain.

Background

Since 2010, the SEC and its staff have been focused on disclosures that public companies make about climate change risks. In 2010, the SEC provided guidance on climate change disclosure (the “2010 Guidance”),[12] assessing compliance with disclosure obligations under the federal securities laws, engaging with public companies on these issues, and learning how the market is currently managing climate-related risks.

In February 2021, the SEC’s then-Acting Chair Allison Herren Lee directed the Division of Corporation Finance to enhance its focus on climate-related disclosure in public company filings.[13] As part of its enhanced focus in this area, the staff of the Division of Corporation Finance (the “Staff”) has reviewed the extent to which public companies address the topics identified in the SEC’s 2010 Guidance. In September 2021, the SEC published a sample letter to companies providing illustrative comments that the Division of Corporation Finance may issue to companies regarding their climate-related disclosure, or the absence of climate-related disclosure[14] (the “Sample Letter”).

In March 2021, the SEC announced the creation of a Climate and ESG Task Force (the “Task Force”) in the Division of Enforcement[15] and then-Acting SEC Chair Lee asked the Staff to evaluate the SEC’s disclosure rules “with an eye toward facilitating the disclosure of consistent, comparable, and reliable information on climate change.”[16] To facilitate the Staff’s assessment, Lee requested public comment on questions that would be useful to consider as part of the evaluation. Lee also solicited comments generally as to how the SEC can best regulate climate change disclosures. The SEC received over 400 comment letters in response to this request. In June 2021, SEC Chair Gary Gensler indicated that he had asked the Staff to put together recommendations for mandatory company disclosures on climate risk.[17]

On March 22, 2022, the SEC proposed significant new disclosure requirements modeled in part on the TCFD disclosure framework[18] to enhance and standardize climate-related disclosure requirements. The proposed amendments contemplated wide-ranging periodic disclosure requirements regarding the registrant’s identification and management of climate-related risks, climate-related risks that are reasonably likely to have material impacts on the registrant’s business, consolidated financial statements, and GHG emission metrics, climate-related financial metrics, and Scope 1, 2, and 3 GHG emissions and, following a phase-in period, companies would be required to provide an attestation report for its Scope 1 and Scope 2 emissions disclosures from an independent expert qualified in GHG emissions.

The SEC received over 24,000 comment letters in response to the Proposing Release. The SEC noted in its adopting press release that the final rules reflected the SEC’s “efforts to respond to investors’ demand for more consistent, comparable, and reliable information about the financial effects of climate-related risks on a registrant’s operations and how it manages those risks while balancing concerns about mitigating the associated costs of the rules.”[19] Demonstrating both the reaction from issuers to demand from investors on climate-related disclosures, as well as potential risk for lack of consistency among issuers, the SEC noted in the Adopting Release that even in the absence of these rules, many U.S. publicly listed companies, and nearly all companies in the Russell 1000 Index, were providing some disclosures regarding climate-related risks, with 36% of all annual reports overall, and 68% of reports by LAFs, containing climate-related key words in 2022.

Form 10-K Climate Related Disclosures (New Item 6)

Below is a summary of the new disclosure items for U.S. issuers’ Annual Reports on Form 10-K. LAFs and Afs will also be required to report on the registrant’s Scope 1 and Scope 2 GHG Emissions in the Quarterly Report on Form 10-Q for the second quarter, or as an amendment to the Form 10-K due at approximately the same time as the second quarter Form 10-Q.

Governance and Risk Management (Items 1501 and 1503)

Under new Items 1501 and 1503, disclosure is required regarding a registrant’s board and management oversight over climate-related risks, as well as the registrant’s material climate-risk identification and management strategies.

Board Oversight

Companies must describe the board of directors’ oversight of the climate-related risks, and identify and describe, if applicable:

- Any board committee or sub-committee responsible for oversight of climate-related risks;

- The process by which the board of directors or sub-committee is informed about climate‑related risks;

- Whether and how the board of directors oversees progress against any identified target or goal or transition plan.

Management Oversight

Companies must describe management’s role in assessing and managing the registrant’s material climate-related risks. The disclosure should address, as applicable, items including:

- Whether and which management positions or committees are responsible for assessing and managing climate-related risk;

- The expertise of members of management responsible for assessing and managing climate‑related risks (including prior work experience in climate-related matters, any relevant degrees or certifications, and knowledge, skills, or other background in climate‑related matters);

- Management’s process for assessing and managing climate-related risks; and

- Whether management reports information about the identified risks to the registrant’s board of directors.

Risk Management

Companies must describe any process they have for identifying, assessing, and managing material climate-related risks, including the process for:

- identifying whether a material physical or transition risk has been or is reasonably likely to be incurred;

- determining whether to mitigate, accept, or adapt to any identified risk, and

- the prioritization of risks.

In terms of climate-related risk management, companies must disclose whether and how any identified process has been integrated into the registrant’s overall risk management system or process.

Risks and Impact on Strategy (Item 1502)

Under new Item 1502, companies are required to disclose climate-related risks that have materially impacted or are reasonably likely to have a material impact on the registrant, including on its strategy, results of operations, or financial condition in both the short term as well as in the long term. The disclosure must include:

- Information on the nature of the impact or risk presented and the extent of the registrant’s exposure to the risk;

- Whether and how each impact is integrated into the registrant’s strategic, financial planning, and capital allocation considerations as well as business model and strategy, including the role of any carbon offsets or RECs utilized; and

- Information on the financial statement impact, including whether and how the identified risks have or are reasonably likely to materially affect the financial statements.

For companies that have set an internal price on carbon and if the use of the internal carbon price is material to how the registrant evaluates and manages an identified climate-related risk, disclosure must be provided regarding the total price per metric ton of CO2e including how the total price is estimated to change over the time periods referenced.

In the Adopting Release, the SEC adopted the short-term (i.e., the next 12 months) and long-term (i.e., beyond the next 12 months) temporal standard (rather than short, medium, and long), which they noted was generally consistent with the existing standard in the MD&A and would help address concerns from commenters that the imposition of a different temporal standard (such as the proposed medium-term period) would potentially conflict with the assessment of other risks and events that are reasonably likely to have a material impact on future operations.

The SEC also reaffirmed that in evaluating whether climate-related risks have materially impacted or are reasonably likely to have a material impact on the registrant, including on its business strategy, results of operations, or financial condition, companies should rely on the materiality standard set forth in the numerous cases addressing materiality in the securities laws, as well as Rule 405 under the Securities Act of 1933, as amended and Exchange Act Rule 12b-2.[20] The SEC also confirmed that the reasonably likely component is the same standard as that used in the MD&A regarding known trends, events, and uncertainties.

Targets and Goals (Item 1504)

Under new Item 1504, a registrant must disclose any climate-related target or goal that has materially affected or is reasonably likely to materially affect the registrant’s business, results of operations, or financial condition. The disclosure must provide “any additional information or explanation necessary to an understanding of the material impact or reasonably likely material impact of the target or goal, including…but not limited to, a description of:”

- The scope of activities included in the target;

- The unit of measurement;

- The timeframe during which the goal is intended to be achieved and whether this timeframe is consistent with other goals established by applicable rules, regulations, or guidance;

- If established, the defined baseline time period by which progress will be tracked; and

- How the registrant intends to meet the climate-related targets or goals.

Annually, a registrant must update the disclosure by describing the actions taken during the year to achieve the targets or goals and include a discussion of any material impacts to its business, results of operations or financial condition as a direct result of the target or goal, or the actions taken to make progress toward meeting the target or goal. Disclosure also needs to be made of any material expenditures and material impacts on financial estimates and assumptions as a direct result of the target or goal or the actions taken to make progress towards meeting it.

- If carbon offsets or RECs were used as a material component of the plan to achieve climate-related The amount of carbon avoidance, reduction, or removal represented by the offsets, or the amount of generated renewable energy represented by the RECs,

- The nature and source of the offsets or RECs,

- A description and location of the underlying projects,

- Any registries or other authentication of the offsets or RECs, and

- The cost of the offsets or RECs.

Note that the carbon offsets or RECs disclosure requirements are similar to those required in California for companies making net-zero, carbon-neutral, or significant emissions reductions claims; indeed, the SEC’s Adopting Release explicitly references the California rules.[21] A registrant that does business in California and makes a significant emissions reductions target claim in their SEC filings will likely also need to comply with California’s Voluntary Carbon Market Disclosures Business Regulations Act and, in addition to the required SEC disclosure, provide information on the name of the offset seller and registry, the project name, and the specific protocol used to estimate emissions reductions or removal benefits.

Reporting and Attestation of GHG Emissions (Items 1505 and 1506)

LAFs and AFs starting in 2026 and 2028, respectively, will be required to provide disclosures regarding their Scope 1 and Scope 2 GHG emissions if such emissions are material (for the most recent fiscal year) or previously disclosed in an SEC filing (for historical fiscal years) and beginning in 2029 and 2031, respectively, will be required to provide an attestation report with a limited assurance of the GHG emissions disclosed. With the addition of the materiality qualifier for Scope 1 and Scope 2 GHG emissions reporting, many companies may argue that their Scope 1 and Scope 2 GHG emissions are not simply material to an investment decision because they will not materially impact the registrant’s financial results, particularly in the case of issuers in industries that already have the relatively low rates of climate-related disclosures, such as with consumer retail, technology, and banking companies.

This disclosure may be incorporated in the Annual Report on Form 10-K by reference from the Quarterly Report on Form 10-Q for the second quarter of the following fiscal year, or may be addressed in an amendment to the Form 10-K filed by the due date for disclosure in the applicable Form 10-Q.[22] Foreign private issuers are permitted to make this disclosure in an amendment to the Form 20-F within 225 days after the end of the fiscal year.

Reporting

For Scope 1 and Scope 2 emissions that are required to be disclosed under the rules, companies must provide:

- Disclosure of the Scope 1 and Scope 2 emissions separately, expressed in terms of CO2e, together with disclosure of any individually material constituent gas on a disaggregated basis; and

- Scope 1 and/or Scope 2 emissions in gross terms, excluding the impact of any purchased or generated offsets.

Disclosure regarding GHG emissions from a manure management system is permitted to be omitted from the Scopes 1 and 2 emissions disclosures so long as implementation of the provision is subject to restrictions on appropriated funds or otherwise prohibited under federal law.

Companies providing disclosure regarding Scopes 1 and 2 emissions are required to provide disclosure regarding the methodology, significant inputs, and significant assumptions used to calculate their GHG emissions. The description must include:

- Organizational boundaries used when calculating the disclosed GHG emissions, including:

- the method used to determine the boundaries;

- A brief discussion of the operational boundaries used, including the approach to the categorization of emissions and emissions sources; and

- and a succinct explanation of any material differences between these boundaries and the scope of entities and operations included in the consolidated financial statements; and

- A brief description of the protocol or standard used to report the GHG emissions, including the calculation approach, the type and source of any emission factors used, and any calculation tools used to calculate the emissions.

A registrant is allowed to use reasonable estimates when disclosing its GHG emissions, as long as it also describes the underlying assumptions and reasons for using the estimates.

Attestation

Subject to the compliance phase in periods specified above, a registrant required to provide disclosure regarding Scope 1 and/or Scope 2 emissions must also include an attestation report covering the disclosure in the filing. For filings made by LAFs beginning Fiscal Year 2029 and AFs beginning Fiscal Year 2031, the report must be provided at a limited assurance level and cover the Scope 1 and/or Scope 2 emissions disclosure. The level of assurance increases to a reasonable level of assurance for Scope 1 emissions disclosures by LAFs beginning in Fiscal Year 2033.

The attestation report must be provided under standards that are (A) (i) publicly available at no cost or (ii) that are widely used for GHG emissions assurance and (B) established by a body or group that has followed due process procedures, including the board distribution of the framework for public comment. The attestation report must follow the standards set forth by the standard (or standards) used by the GHG emissions attestation provider. Any voluntary assurance reports obtained after the first required fiscal year assurances must follow the same requirements as those for required assurances.

The attestation report must be prepared and signed by a GHG emissions attestation provider, which is defined by Rule 1506 as a person or firm that has the following characteristics:

- GHG Emissions Expert: Is an expert in GHG emissions and has significant experience in measuring, analyzing, reporting or attesting to GHG emissions that enables them to: (i) perform engagements in accordance with attestation standards and applicable legal and regulatory requirements and (ii) issue reports that are appropriate.

- Independent: The GHG emissions attestation provider must be independent from the registrant, and any of its affiliates, during the attestation and professional engagement period. Independence hinges on the attestation provider’s capability to exercise objective and impartial judgment on all issues within their engagement. In determining independence, the SEC will consider all relevant circumstances (including all financial or other relationships between the attestation provider and the registrant (or any of its affiliates) and whether the relationship or provision of services:

- creates a mutual or conflicting interest between the attestation provider and the registrant (or any of its affiliates);

- places the attestation provider in the position of attesting to their own work;

- results in the attestation provider acting as management or an employee of the registrant (or any of its affiliates); or

- places the attestation provider in a position of being an advocate for the registrant (or any of its affiliates).

In addition to including the attestation report, companies must disclose:

- whether the GHG emissions attestation provider is subject to any oversight inspection program and, if so, must disclose the program(s) and whether the GHG emissions attestation engagement is included within the scope of authority of the oversight inspection program; and

- whether any GHG emissions attestation provider that was previously engaged to provide attestation over the registrant’s GHG emissions disclosure was dismissed or declined to stand for reappointment.

Similar to the requirements to disclose disagreements between the registrant and its independent auditors, if a previously engaged GHG emissions attestation provider was dismissed or refused to stand for reappointment, disclosure must be provided regarding this and whether there were any disagreements with the former GHG emissions attestation provider on any matter of measurement or disclosure of GHG emissions or attestation scope of procedures and, if applicable, describe each disagreement and whether the registrant has authorized the former provider to respond fully to the inquiries of successor GHG emissions attestation providers concerning the subject matter of each disagreement. Item 1506(d)(2)(ii) provides that the term “disagreements” is to be interpreted broadly and include any difference of opinion concerning any matter of measurement or disclosure of GHG emissions or attestation scope or procedures that (if not resolved to the satisfaction of the former GHG emissions attestation provider) would have caused it to make reference to the subject matter of the disagreement in connection with the report.

Companies that are not required to include a GHG emissions attestation but make GHG emissions disclosures in the filing that are subject to third-party assurance must still identify and discuss the service provider, assurance standard used, level and scope of services provided, brief description of the results, whether the service provider has any other material business relationships with or has provided any material professional services to the registrant, and whether the service provider is subject to any oversight inspection programs and, if so, which programs and whether assurance services are included within the scope of authority of such oversight inspection program.

Financial Disclosures

New Article 14 of Regulation S-X requires public companies to include in their consolidated financial statements and discuss in separate notes to the financial statements disclosure regarding capitalized costs, expenditures expensed, charges, losses, or recovery results when a severe weather event or other natural condition is a significant contributing factor in incurring the capitalized cost, expenditure expensed, charge, loss, or recovery. Specifically, public companies are required to provide information regarding:

- The aggregate amount of expenditures expensed as incurred and losses from severe financial events and other natural conditions (i.e., hurricanes, tornadoes, floods, droughts, etc.).

- Disclosure is not required if the aggregate amount of expenditures expensed as incurred and losses is greater than $100,000 and greater or equal to 1% of the absolute value of income or loss before income tax expense or benefit.

- The disclosure must separately identify where they are presented in the income statement.

- The aggregate amount of capitalized costs and charges incurred as a result of severe weather events and other natural conditions.

- Disclosure is not required if the aggregate amount of the absolute value of capitalized costs and charges is greater than $500,000 and equals or exceeds 1% of the absolute value of stockholders’ equity or deficit.

- The disclosure must separately identify where they are present in the balance sheet.

- The aggregate amount of any recoveries recognized as a result of severe weather events and other natural conditions for which disclosures are made.

- If carbon offsets or RECs are used as a material component of the registrant’s plans to achieve disclosed climate-related targets or goals, the aggregate amount of carbon offsets and RECs expensed, the aggregate amount of capitalized carbon offsets and RECs recognized, and the aggregate amount of losses incurred on the capitalized carbon offsets and RECs.

- The disclosure must separately identify where they are present in the income statement and balance sheet.

- If disclosure is required, the accounting policy for carbon offsets and RECs must also be described.

New Article 14 also requires disclosure of whether and how estimates and assumptions used to produce the financial statements were materially impacted by exposures to risks and uncertainties associated with, or known impacts from, severe weather events and other natural conditions, or any climate-related targets or transition plans disclosed by the registrant.

The metrics must be calculated using financial information consistent with the consolidated financials (i.e., information from consolidated subsidiaries must be included) and the metrics must be provided for the most recently completed fiscal year and, to the extent previously disclosed or required to be disclosed, for the historical fiscal years included in the filing.

Safe Harbor Protection for Certain Climate-Related Disclosures (Item 1507)

In the Proposing Release, the SEC proposed a safe harbor only for statements regarding Scope 3 emissions disclosed pursuant to Items 1500 through 1506. However, in the Adopting Release, the SEC noted that due to feedback from commenters and because the final rules will not require disclosure regarding Scope 3 emissions, the final rules provide safe harbor protection for disclosures (other than historic facts) provided pursuant to Item 1502(e) (transition plans), 1502(f) (scenario analysis), 1502(g) (internal carbon pricing), and 1504 (targets and goals). Additionally, certain other disclosures and statements may fall within the definition of “forward-looking statement” and thus receive safe harbor protection.

Definitions

Although the SEC sought to adopt definitions that are similar to those used in the climate-related disclosure framework of the TCFD and the GHG Protocol, with which many registrants and investors would be familiar with, in response to comments expressing significant concerns about the scope of the proposed rules, the SEC modified the definitions of the rules to more closely conform them with other SEC rules relevant to risk assessment and to limit the scope of the disclosure (including by limiting the time periods for which disclosure is to be made).

Disclosure by Foreign Private Issuers

The SEC amended Form 20-F to add Item 3.E, which requires a foreign private issuer to include in its Annual Report on Form 20-F the same type of disclosure that the SEC requires pursuant to Item 1500 through 1507 of Regulation S-K. The SEC also amended Form 6-K to require climate‑related disclosure in Item B, information and documentation required to be furnished.

Structured Data

The SEC requires that companies tag the information specified in subpart 1500 of Regulation S-K in Inline XBRL in accordance with Rule 405 of Regulation S-T and the EDGAR Filer Manual. These tagging requirements include block text tagging of narrative disclosures, as well as detail tagging of quantitative amounts disclosed within the narrative disclosures.

Costs

The SEC’s cost estimates with respect to the new rules are summarized in the following tables.

First Year:

Ongoing costs:

In Summary

The final amendments adopted by the SEC represent a significant step in the SEC’s efforts to promote greater transparency regarding and standardization of climate-related disclosures. With these final rules, the SEC now moves past its reliance on more general disclosure requirements and interpretive guidance by creating an entirely new disclosure regime that will apply to periodic disclosures regarding climate-related risks, the registrant’s oversight of the climate-related risks, and the registrant’s impact on the environment. These new rules also move the SEC, and U.S.‑listed public companies, closer in-line with the disclosure requirements in the EU (with the CSRD) and other jurisdictions, such as China, which are generally following S2 of ISSB for required climate disclosures. To the extent that U.S. public companies have not already done so in response to CSRD or the California required disclosures, these new disclosure requirements will require U.S. public companies to evaluate and adapt their disclosure controls and procedures, management processes, and governance structures around climate-related risks and the registrant’s own GHG emissions – if not also their data collection and verification processes for GHG emissions of those in their value chain – to prepare for the new environment of transparency in this important area.

Appendix A

Definitions from Item 1500 (§ 229.1500) of the SEC Rule

Carbon offsets represents an emissions reduction, removal, or avoidance of greenhouse gases (“GHG”) in a manner calculated and traced for the purpose of offsetting an entity’s GHG emissions.

Climate-related risks means the actual or potential negative impacts of climate-related conditions and events on a registrant’s business, results of operations, or financial condition. Climate-related risks include the following:

(1) Physical risks include both acute risks and chronic risks to the registrant’s business operations.

(2) Acute risks are event-driven and may relate to shorter term severe weather events, such as hurricanes, floods, tornadoes, and wildfires, among other events.

(3) Chronic risks relate to longer term weather patterns, such as sustained higher temperatures, sea level rise, and drought, as well as related effects such as decreased arability of farmland, decreased habitability of land, and decreased availability of fresh water.

(4) Transition risks are the actual or potential negative impacts on a registrant’s business, results of operations, or financial condition attributable to regulatory, technological, and market changes to address the mitigation of, or adaptation to, climate-related risks, including such non-exclusive examples as increased costs attributable to changes in law or policy, reduced market demand for carbon-intensive products leading to decreased prices or profits for such products, the devaluation or abandonment of assets, risk of legal liability and litigation defense costs, competitive pressures associated with the adoption of new technologies, and reputational impacts (including those stemming from a registrant’s customers or business counterparties) that might trigger changes to market behavior, consumer preferences or behavior, and registrant behavior.

Carbon dioxide equivalent or CO2e means the common unit of measurement to indicate the global warming potential (“GWP”) of each greenhouse gas, expressed in terms of the GWP of one unit of carbon dioxide.

Emission factor means a multiplication factor allowing actual GHG emissions to be calculated from available activity data or, if no activity data are available, economic data, to derive absolute GHG emissions. Examples of activity data include kilowatt-hours of electricity used, quantity of fuel used, output of a process, hours of operation of equipment, distance travelled, and floor area of a building.

GHG or Greenhouse gases means carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), nitrogen trifluoride (NF3), hydrofluorocarbons (HFCs), perfluorocarbons (PFCs), and sulfur hexafluoride (SF6).

GHG emissions means direct and indirect emissions of greenhouse gases expressed in metric tons of carbon dioxide equivalent (CO2e), of which:

(1) Direct emissions are GHG emissions from sources that are owned or controlled by a registrant.

(2) Indirect emissions are GHG emissions that result from the activities of the registrant but occur at sources not owned or controlled by the registrant.

Internal carbon price means an estimated cost of carbon emissions used internally within an organization.

Operational boundaries means the boundaries that determine the direct and indirect emissions associated with the business operations owned or controlled by a registrant.

Organizational boundaries means the boundaries that determine the operations owned or controlled by a registrant for the purpose of calculating its GHG emissions.

Renewable energy credit or certificate or REC means a credit or certificate representing each megawatt-hour (1 MWh or 1,000 kilowatt-hours) of renewable electricity generated and delivered to a power grid.

Scenario analysis means a process for identifying and assessing a potential range of outcomes of various possible future climate scenarios, and how climate-related risks may impact a registrant’s business strategy, results of operations, or financial condition over time.

Scope 1 emissions are direct GHG emissions from operations that are owned or controlled by a registrant.

Scope 2 emissions are indirect GHG emissions from the generation of purchased or acquired electricity, steam, heat, or cooling that is consumed by operations owned or controlled by a registrant.

Transition plan means a registrant’s strategy and implementation plan to reduce climate-related risks, which may include a plan to reduce its GHG emissions in line with its own commitments or commitments of jurisdictions within which it has significant operations.

[1] SEC Adopts Rules to Enhance and Standardize Climate-Related Disclosures for Investors and Release No. 33-11275, The Enhancement and Standardization of Climate-Related Disclosures for Investors (March 6, 2024), (the “Adopting Release”).

[2] The petition argues that “the final rule exceeds the [SEC’s] statutory authority and otherwise is arbitrary, capricious, an abuse of discretion, and not in accordance with law.”

[3] The TCFD is an industry-led task force that intends to promote better-informed investment, credit, and insurance underwriting decisions. It was designed to elicit information to help investors better understand a company’s climate-related risks to enable them to make more informed investment decisions.

[4] Quantitative and qualitative disclosure of material expenditures incurred and material impacts on financial estimates and assumptions that directly result from activities to mitigate or adapt to disclosed climate-related risks.

[5] Quantitative and qualitative disclosure of material expenditures incurred and material impacts on financial estimates and assumptions as a direct result of the disclosed transition plan.

[6] Quantitative and qualitative disclosure of material expenditures and material impacts on financial estimates and assumptions as a direct result of a company’s disclosed climate-related target or goal or the actions take to make progress thereto.

[7] For companies with a fiscal year ending December 31, the 10-K for Fiscal Year 2025, filed in the first quarter of 2026.

[8] For companies with a fiscal year ending December 31, the 10-K for Fiscal Year 2026, filed in the first quarter of 2027.

[9] For companies with a fiscal year ending December 31, the 10-K for Fiscal Year 2027, filed in the first quarter of 2028.

[10] California Climate Laws Require Public Disclosure of Greenhouse Gas Emissions and Climate-Related Financial Risks; California Enacts AB 1305 to Strengthen the Voluntary Carbon Market and Continues to Lead on Climate Regulation.

[11] Corporate Sustainability: EU to Expand ESG-Related Reporting Obligations.

[12] Commission Guidance Regarding Disclosure Related to Climate Change, Release No. 33-9106 (Feb. 2, 2010).

[13] Statement on the Review of Climate-Related Disclosure (Feb. 24, 2021).

[14] Commission Guidance Regarding Disclosure Related to Climate Change, Release No. 33-9106 (Feb. 2, 2010).

[15] SEC Announces Enforcement Task Force Focused on Climate and ESG Issues (Mar. 4, 2021).

[16] Public Input Welcomed on Climate Change Disclosures (Mar. 15, 2021).

[17] Chair Gary Gensler, Prepared remarks at London City Week (June 24, 2021).

[18] Release No. 33-11042, The Enhancement and Standardization of Climate-Related Disclosures for Investors (March 22, 2022), (the “Proposing Release”).

[19] SEC Adopts Rules to Enhance and Standardize Climate-Related Disclosures for Investors.

[20] See, e.g., TSC Industries, Inc. v. Northway, Inc., 426 U.S. 438, 449 (1976); Basic, Inc. v. Levinson, 485 U.S. 224, 232 (1988); and Matrixx Initiatives, Inc. v. Siracusano, 563 U.S. 27 (2011).

[21] California Enacts AB 1305 to Strengthen the Voluntary Carbon Market and Continues to Lead on Climate Regulation.

[22] Similar to incorporation of Part III of the Form 10-K by reference to a registrant’s proxy statement, in order to incorporate the GHG emissions disclosures by reference to the future filing, the Form 10-K will need to include language indicating the intent to incorporate such disclosure.

[23] Disclosure related to governance of climate-risks.

[24] Disclosure regarding impacts of climate-related risks on strategy, business model, and outlook.

[25] Disclosure regarding climate-related risk management.

[26] If applicable, disclosure regarding scenario analysis.

[27] If applicable, disclosure regrading climate related targets or goals.

[28] Disclosure related to governance of climate-risks.

[29] Disclosure regarding impacts of climate-related risks on strategy, business model, and outlook.

[30] Disclosure regarding climate-related risk management.

[31] If applicable, disclosure regarding scenario analysis.

[32] If applicable, disclosure regrading climate related targets or goals.

[View source.]