On March 6, 2024, the U.S. Securities and Exchange Commission (SEC) adopted final rules requiring companies to provide certain climate-related information in their annual reports and registration statements. The SEC Fact Sheet is available here. Set forth below are some initial observations, with a more detailed client alert and webinar to follow.

- Scope 3 Greenhouse Gas (GHG) Emissions Disclosure Not Required. The final rules eliminate the proposed requirement to disclose Scope 3 GHG emissions.

- Scope 1 and 2 GHG Emissions Disclosure Required for Certain Filers, if Material. The final rules require disclosure of Scope 1 and/or Scope 2 GHG emissions by large accelerated filers and accelerated filers (other than smaller reporting companies (SRCs) and emerging growth companies (EGCs), which are exempt from this disclosure requirement), only if such emissions are material. The final rules include a phase-in compliance date for this requirement.

- Attestation Required, with Phase-In Compliance Dates. Companies required to disclose Scope 1 and/or Scope 2 GHG emissions must include an attestation report covering this disclosure in the relevant filing, subject to extended phase-in compliance dates. Under the final rules:

- accelerated filers need only obtain limited assurance over their Scope 1 and/or Scope 2 GHG emissions disclosure (the proposed rules would have required a reasonable assurance level after a phase-in period), and

- large accelerated filers are required initially to obtain limited assurance over their Scope 1 and/or Scope 2 GHG emissions disclosure and, after an additional phase-in period, reasonable assurance over these disclosures.

- Narrowed Financial Statement Disclosure Required. The SEC eliminated the proposed financial impact metrics disclosure requirement, which would have required companies to disclose the financial impacts of climate-related risks on financial statement line items unless the aggregated impact of such risks was less than one percent of the total line item for the relevant fiscal year. Instead, the final rules are narrower, focused on severe weather events and other natural conditions.

- Board Expertise Disclosure Not Required. The final rules require certain disclosures relating to board oversight of climate risks but eliminate the proposed requirements to describe board members’ climate-related expertise and to identify specific board members responsible for climate-risk oversight.

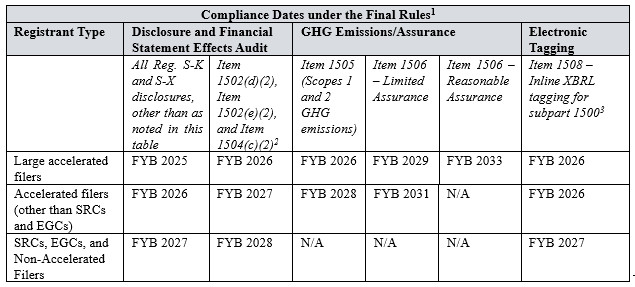

The final rules are effective 60 days following publication in the Federal Register. Companies are required to comply with the final rules on a phase-in basis, depending on filer status and the content of the required disclosure. The following chart, derived from the SEC Fact Sheet, provides a summary of the phase-in periods for compliance with the final rules.

[1] As used in this chart, “FYB” refers to any fiscal year beginning in the calendar year listed.

[2] These provisions refer to quantitative and qualitative disclosure related to material actions taken (1) to mitigate or adapt to climate-related risks, (2) under a climate-related transition plan, and (3) to achieve a disclosed climate-related target or goal, respectively.

[3] Financial statement disclosures under Article 14 will be required to be tagged in accordance with existing rules pertaining to the tagging of financial statements. See Rule 405(b)(1)(i) of Regulation S-T.