On August 23, 2023, in a 3-2 vote, the SEC adopted a rule package (the “Adopted Rules”) that establishes significant new obligations for private fund advisers under the Investment Advisers Act of 1940. While the Adopted Rules pare back some of the proposed rules’ flat prohibitions and institute important (but limited) exceptions from certain rule obligations for existing funds, the rule package remains in many respects a marked departure from the disclosure-based approach that has generally prevailed under the Advisers Act, particularly in the institutional context.

The Adopted Rules include the following, among other provisions/rule amendments:

- Restricted Activities Rule: Prohibits certain adviser charges to and relationships with a private fund unless the adviser meets certain investor disclosure or consent requirements.

- Preferential Treatment Rule: Prohibits granting redemption rights or providing information to an investor if the adviser reasonably expects either to have a material, negative effect on other investors (subject to exceptions), and requires disclosure with respect to other preferential terms.

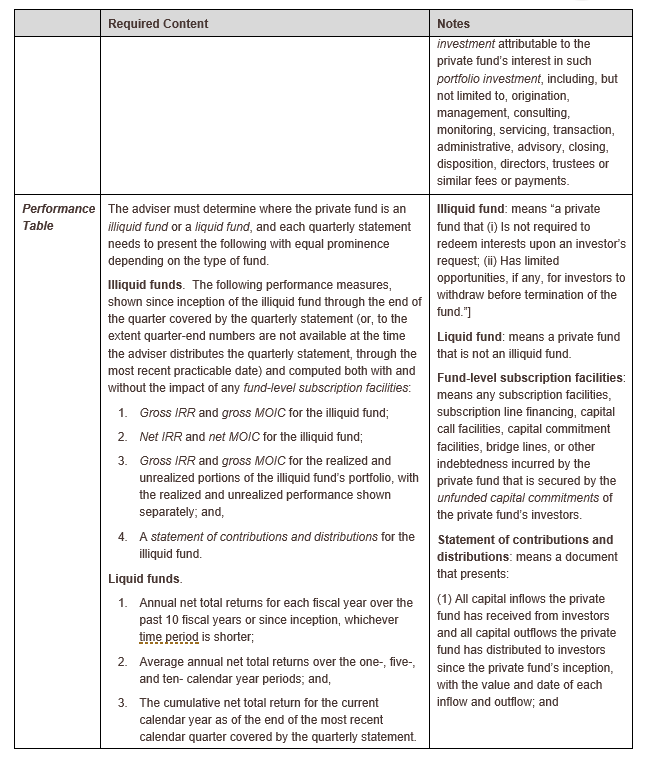

- Quarterly Statement Rule: Requires quarterly statements that include three mandatory tables -- a “Fund Table” (regarding certain fees and expenses), a “Portfolio Investment Table” (regarding compensation the adviser or related persons receives from a portfolio investment), and a “Performance Table.”

- Private Fund Audit Rule: Requires audits for private funds (i.e., the investment adviser cannot rely on surprise examination under the Custody Rule with respect to vehicles that are within the definition of private fund).

- Adviser-Led Secondaries Rule: Requires a fairness or valuation opinion for adviser-led secondaries.

We note:

- Existing funds are provided a limited exclusion from certain provisions of the Restricted Activities Rule and the Preferential Treatment Rule.

- The scope of the Adopted Rules is, generally, limited to advisers to a “private fund”1, defined as an issuer that would be an investment company but for Investment Company Act Section 3(c)(1) or a 3(c)(7).

- Certain of the Adopted Rules apply only to SEC-Registered Investment Advisers, while others apply to all investment advisers to private funds (i.e., including Exempt Reporting Advisers, state-registered advisers, and Foreign Private Advisers).

- Compliance dates:

- Adviser-Led Secondaries Rule, Preferential Treatment Rule, and Restricted Activities Rule:

- For advisers with $1.5 billion or more in private funds assets under management, the compliance date is 12 months after the date of publication in the Federal Register.

- For advisers with less than $1.5 billion in private funds assets under management, the compliance date is 18 months after the date of publication in the Federal Register.

- Private Fund Audit Rule and Quarterly Statement Rule: the compliance date is 18 months after the date of publication in the Federal Register.

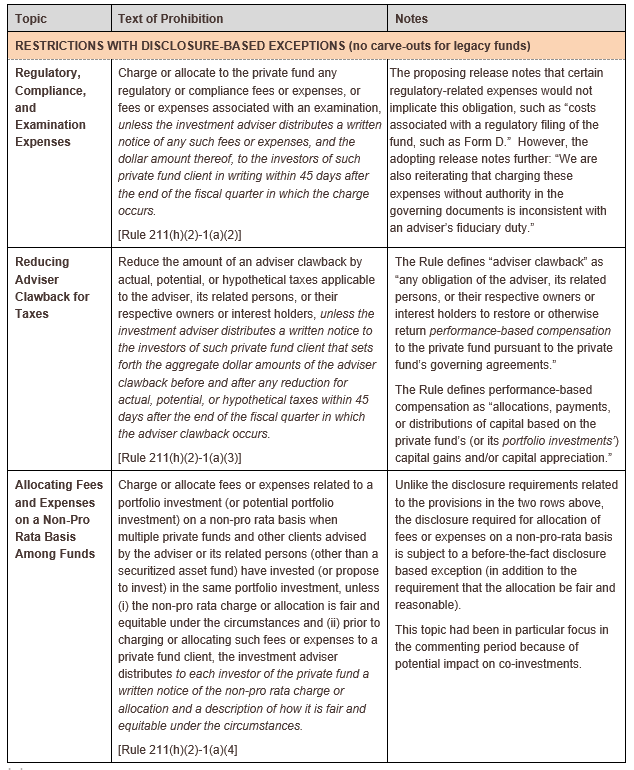

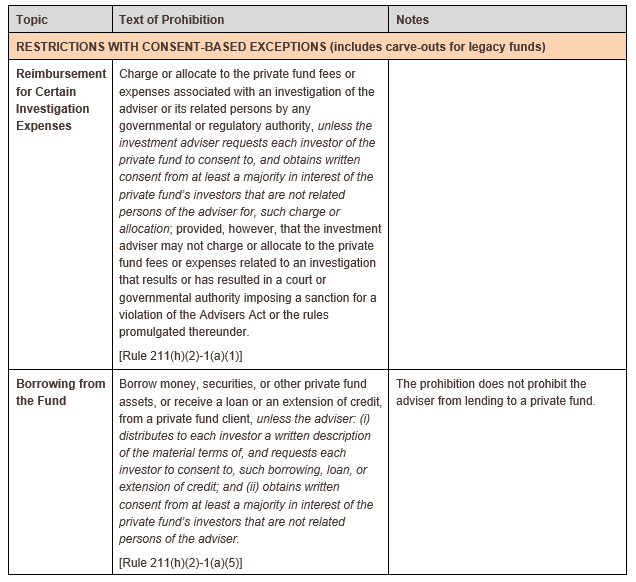

RESTRICTED ACTIVITIES RULE

The Restricted Activities Rule establishes five categories of activities (generally, charges to and arrangements and relationships with a private fund) that are, directly or indirectly, prohibited unless disclosure is made or investor consents are obtained as described in the following chart.

As noted in the chart, three types of prohibitions are subject to disclosure-based exceptions, and two types of prohibitions are subject to consent-based exceptions. The disclosure-based exceptions require specific reporting either after the charge or allocation occurs or, in the case of non-pro rata allocation of expenses to a fund, prior to the charge or allocation.

The restrictions that are subject to consent-based exceptions will not apply to the contractual agreements governing legacy funds (i.e., a fund that has commenced operations as of the Restricted Activities Rule compliance date) to the extent that compliance with such provision would require the parties to amend such governing agreements.

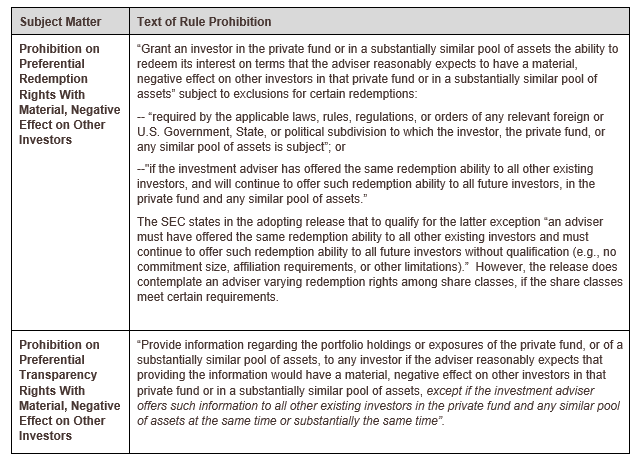

PREFERENTIAL TREATMENT RULE

The Preferential Treatment Rule, as described in the below chart:

- Prohibits advisers from granting certain types of preferential redemption or transparency rights to an investor that the adviser reasonably expects to have a material, negative effect on other investors, subject to exceptions; and,

- Requires advisers to provide written disclosures to prospective and current investors in a private fund regarding all preferential treatment the adviser or its related persons provide to other investors in the same fund.

Prohibited Preferential Treatment (subject to limited exceptions for legacy funds)

Other Preferential Treatment

In addition to the categories of preferential treatment discussed in the chart above, the Preferential Treatment Rule also requires disclosure (on various timelines) of other types of preferential terms, as described below.

Pre-investment notice for preferential treatment regarding any material economic terms. Under the Rule, an adviser must provide to each prospective investor in the private fund, prior to the investor’s investment in the private fund, a written notice that provides specific information regarding any preferential treatment related to any material economic terms that the adviser or its related persons provide to other investors in the same private fund [Rule 211(h)(2)-3(b)(2)].

In discussing the Rule’s provisions requiring pre-investment disclosure of “material economic terms”, the adopting release refers to “those terms that a prospective investor would find most important and that would significantly impact its bargaining position”, citing, by way of non-exhaustive example, “the cost of investing, liquidity rights, fee breaks, and co-investment rights”.

Post-investment notice for other preferential terms (terms other than material economic terms): Under the Rule, an adviser must distribute to current investors:

- For an illiquid fund, as soon as reasonably practicable following the end of the private fund’s fundraising period, written disclosure of all preferential treatment the adviser or its related persons has provided to other investors in the same private fund;

- For a liquid fund, as soon as reasonably practicable following the investor’s investment in the private fund, written disclosure of all preferential treatment the adviser or its related persons has provided to other investors in the same private fund; and

- On at least an annual basis, a written notice that provides specific information regarding any preferential treatment provided by the adviser or its related persons to other investors in the same private fund since the last written notice provided in accordance with this requirement, if any. [Rule 211(h)(2)-3(b)(2)]

The definitions of illiquid and liquid fund are discussed below in the section Quarterly Statements Rule.

The SEC’s stated purpose in not requiring pre-investment notice of terms other than material economic terms was to allow advisers to wait until after an investor has invested in the fund to disclose the remaining preferential terms (i.e., all preferential terms that are not material economic terms) so as not to impede the closing process.

With respect to the disclosure that is required of preferential terms, the adopting release states: “the final rule will require an adviser to describe specifically the preferential treatment to convey its relevance… For example, if an adviser provides an investor with lower fee terms in exchange for a significantly higher capital contribution than paid by others, we do not believe that mere disclosure that some investors pay a lower fee is specific enough..[A]n adviser must describe the lower fee terms, including the applicable rate (or range of rates if multiple investors pay such lower fees), in order to provide specific information as required by the rule.…”

EXCEPTIONS FOR EXISTING FUNDS

Neither (i) the “preferential treatment” that is prohibited under the Preferential Treatment Rule, nor (ii) the portion of the Restricted Activities Rule with consent-based exceptions will apply with respect to contractual agreements governing a private fund that has commenced operations as of the relevant compliance date and that were entered into in writing prior to the compliance date if the provision would require the parties to amend such governing agreements.

The Adopting Release sets forth certain, non-exclusive scenarios that could indicate a fund had “commenced operations”. In particular: “[t]he commencement of operations includes any bona fide activity directed towards operating a private fund, including investment, fundraising, or operational activity. Examples of activity that could indicate a private fund has commenced operations include issuing capital calls, setting up a subscription facility for the fund, holding an initial fund closing and conducting due diligence on potential fund investments, or making an investment on behalf of the fund.”

We highlight that the exceptions provided for legacy funds:

- Are only exceptions from certain provisions of the Adopted Rules, and as such the fund will still need to comply with significant portions of the Adopted Rules; and

- Even with respect to the specific provisions from which legacy funds are excepted, close attention must be paid to the language of the exception, which carve-out is only with respect to the extent that compliance with such prohibition or restriction would require the parties to amend governing agreements.

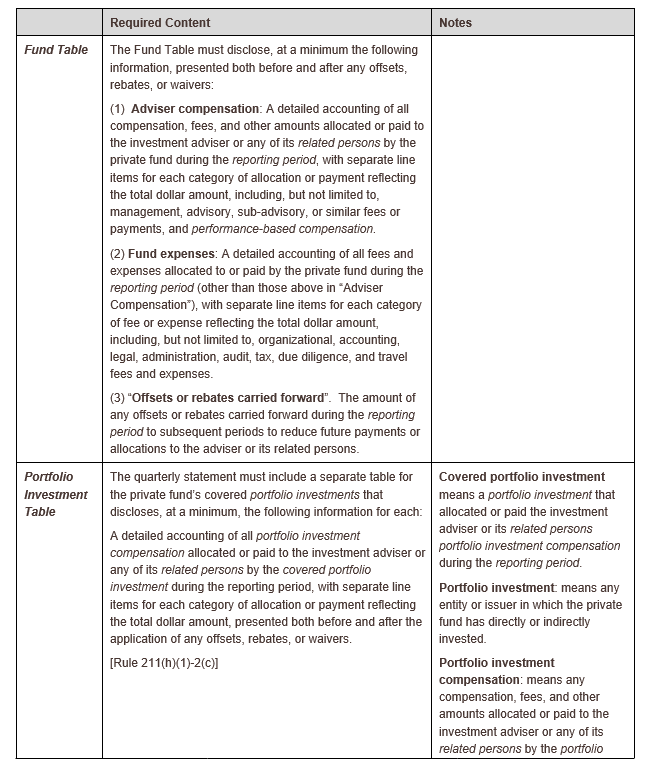

QUARTERLY STATEMENT RULE

The Quarterly Statement Rule will require an RIA that advises a private fund to prepare and distribute quarterly statements that include three tables, as further described in the below chart:

- A “Fund Table” setting forth certain information regarding fees, expenses, and offsets or rebates paid to the adviser and its related persons, and fees and expenses paid to other persons;

- A “Portfolio Investment Table” identifying each “portfolio investment” that has paid compensation to the adviser or a related person in the reporting period; and,

- A “Performance Table” setting forth certain performance-related information that varies depending on whether the fund is a “liquid fund” or “illiquid fund” under the Rule, including, in the case of an illiquid fund, Gross IRR and Gross MOIC for the realized and unrealized portions of the illiquid fund’s portfolio, with the realized and unrealized performance shown separately. Performance must be shown both including and excluding the impact of any fund-level subscription facilities.

While the information required for those tables is generally tracked by advisers, additional processes will likely be needed to bring the same into the quarterly report process, to capture/calculate certain information under the Rule’s requirements, or to include the required cross-references to governing documents, among other considerations.

Other considerations:

- Commencement of the requirement for new funds: For a newly formed private fund, the Rule requires a quarterly statement to be prepared and distributed beginning after the fund has at least two full fiscal quarters of generating operating results.

- Timing requirements for distribution of quarterly statements:

- Except for funds of funds, the adviser or another person must distribute the quarterly statement within 45 days after the end of each of the first three fiscal quarters of each fiscal year of the private fund and 90 days after the end of each fiscal year of the private fund.

- For funds of funds, the adviser or another person must distribute the quarterly statement within 75 days after the end of the first three fiscal quarters of each fiscal year and 120 days after the end of each fiscal year.

- Cross references: The quarterly statement must include prominent disclosure regarding the manner in which all expenses, payments, allocations, rebates, waivers, and offsets are calculated and include cross references to the sections of the private fund’s organizational and offering documents that set forth the applicable calculation methodology.

PRIVATE FUND AUDIT RULE

Rule 206(4)-10 will require RIAs to private funds to cause each private fund that it advises to undergo a financial statement audit that meets the requirements of the pooled investment vehicle audit exemption under the Advisers Act Custody Rule. As such, private funds would not be able to rely on the surprise examination provisions of the Custody Rule.

Timing requirements and other requirements for such audit will be as set forth in the Custody Rule and associated guidance. As such, audited financial statements must be distributed within 120 days of the end of the fund’s fiscal year.

ADVISER-LED SECONDARIES RULE

The Rule prohibits an SEC-Registered Investment Adviser that advises private funds from “complet[ing] an adviser-led secondary transaction with respect to any private fund” unless the adviser:

- obtains, and distributes to investors in the private fund, a “fairness opinion” or “valuation opinion” from an independent opinion provider; and

- prepares, and distributes to investors in the private fund, a written summary of any material business relationships the adviser or any of its related persons has, or has had within the past two years, with the independent opinion provider prior to the closing of the adviser-led secondary transaction.

“Adviser-led secondary transactions” is defined as: “transactions initiated by the investment adviser or any of its related persons that offer the private fund’s investors the choice between: (i) selling all or a portion of their interests in the private fund; or (ii) converting or exchanging all or a portion of their interests in the private fund for interests in another vehicle advised by the adviser or any of its related persons.”

WRITTEN DOCUMENTATION OF ANNUAL REVIEW OF COMPLIANCE PROGRAMS

Advisers Act Rule 206(4)-7 requires RIAs to annually review the adequacy of their policies and procedures established to comply with the Advisers Act’s provisions and the effectiveness of their implementation.

The amendments will revise Rule 206(4)-7 to expressly require written documentation of that annual review. The proposing release states that “the proposed required written documentation of the annual review under the compliance rule is meant to be made available to the Commission and the Commission staff and, therefore, should promptly be produced upon request”.

NEXT STEPS

The Adopted Rules’ compliance dates are between 12 and 18 months after publication of the Adopted Rules in the Federal Register, depending on the rule provision and adviser private fund AuM. While the Adopted Rules generally pared back the proposed rules’ more controversial elements, including certain per se prohibitions, and contained important exceptions for funds that have commenced operations as of the compliance date, private fund advisers will still find themselves with much to consider operationally, in terms of legal and compliance considerations, and in terms of investor relations. Advisers to private funds should consider the internal and external impacts of the Adopted Rules on their business and their next steps, which will vary based on the contours of the business.

While this alert focused primarily on summarizing the Adopted Rules, our team will be continuing to analyze the Adopted Rules and associated guidance with respect to specific impacts on private fund legal and business structures and next steps, and will continue to communicate updates.