With fluctuating capital availability, broadly tightening terms, increasing sponsor demand and pressure on pricing in particular on capital call facilities, the market has been changing, if not challenging, for fund borrowers looking at their fund finance lines in 2024.

We have seen a significant rise in alternative financing structures, largely focused around net asset value (NAV) facilities offering potentially better tenure, pricing and bespoke financing solutions in a more difficult market environment, and a creeping interest in hybrid facilities as well. As has been observed in numerous recent NAV financing commentaries, there are specific current drivers elongating fundraising timeframes, whilst attractive secondaries fund investment opportunities abound, largely based on similar factors including sponsors’ ongoing search for liquidity. In these conditions, secondaries fund sponsors will have fund finance on the agenda practically by default, particularly where strategic enhancements to value creation are available via financing arrangements. We have observed that appetite for more expensive facilities can be maintained where they are supporting the promise of instant liquidity to snap up good deals in challenging market conditions and thereafter, long term value.

This article looks at secondaries fund financing, with a focus of one of the key legal aspects: security packages and consent issues, and how challenges around these features can be addressed.

Secondaries fund financing

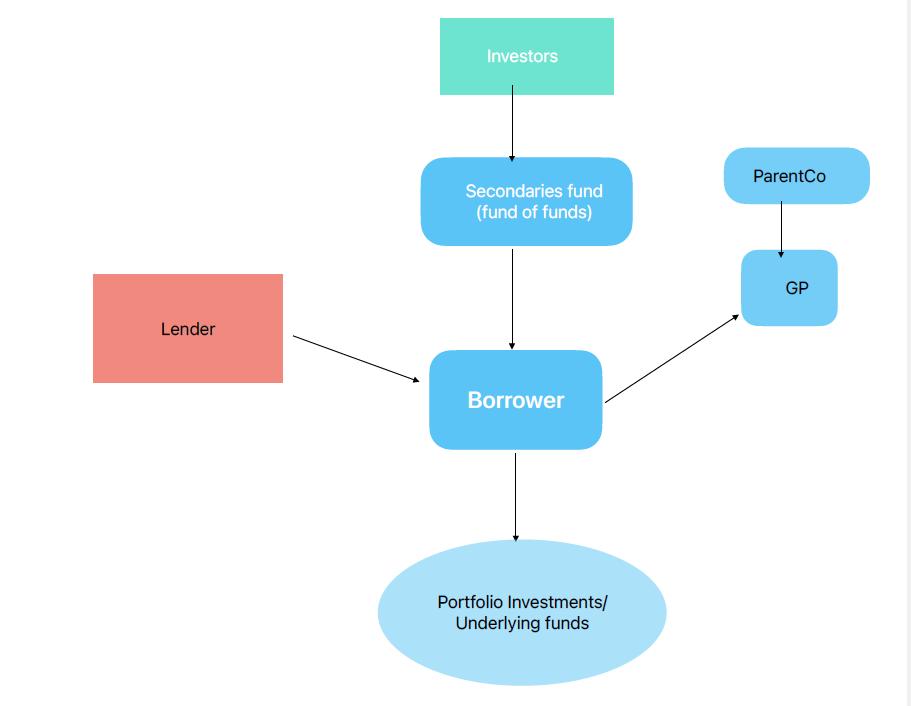

Whilst subscription line or capital call facilities look to the uncalled capital commitments of investors as the collateral backing the financing, NAV facilities look down the structure to the underlying assets of the fund. Such funds typically establish a special purpose vehicle (SPV), which may be in the form of a limited partnership, which will hold the portfolio investments that form the borrowing base of the facility. The amount available to be drawn by the borrower is limited by the value of the borrowing base and whilst the overall facility is typically longer term than the 1-2 year capital call arrangement, that borrowing base may be more limited in the early stages of fund life, giving rise to a facility structure something akin to a cross-over between an acquisition finance and a portfolio backed NAV deal. In such “narrow backed” circumstances, the robust enforceability of the security over the underlying is of keen importance to the lender. The security will likely be comprised of:

- a pledge of 100% of the ownership interests in the SPV;

- if the SPV is a partnership, a general partner interest pledge; and

- relevant bank account security;

together with, potentially in some structures:

- a fund level guarantee;

- asset level security over relevant cash/securities holdings; and

- pledge by the parent of ownership interests in the GP itself.

A simplified diagram of this structure is set forth below.

Borrowing base and eligibility criteria

As mentioned above, the borrowing base of the facility is calculated by reference to the NAV of the portfolio investments underlying, together with, to the extent applicable and/or available, cash and/or securities in relevant accounts. In early fund life, the aggregate NAV of all portfolio investments may be limited and for purposes of the facility underlying this may be narrowed even further by the eligibility criteria. Generally, in order for an investment to be “eligible” for the purposes of inclusion in the borrowing base, it must satisfy specified criteria which are the subject of substantial negotiation in every facility. In some cases, a portfolio may already be (substantially) established, in which case it can be assessed up front and appropriate thresholds for these criteria determined. Lenders will typically undertake due diligence on the underlying portfolio investments, which in the case of secondaries funds will mean a deep dive into the underlying fund terms.

Typical due diligence considerations include:

- questions around transfer restrictions or consent rights which apply including any third party or regulatory consents required to transfer relevant fund assets subject to the security

- any rights of first refusal

- change of control or equivalent exit provisions

- any specific restrictions on assignments

- any specific KYC requirements or conditions of accession for transfers

- reporting or other obligations on the investments

The point about an early fund life facility is that, if this process is difficult when a pre-existing portfolio is laid before the lenders for detailed consideration, it is all the more challenging when the relevant features of the assets must be predicted based on pipeline expectations only. There is an inherent tension between borrower desire for certainty of funding on the one hand, and lender wish to retain discretion over the constituents of the borrowing base on the other.

Security and consents issues in secondaries fund financing

This brings us neatly to one of the main structuring issues for asset-backed secondaries facilities – GP consent requirements arising from restriction on transfers and pledges in the underlying fund documentation. The due diligence carried out on the underlying investments will look at whether GP consent to transfer is required (or expected to be required at some point in the future, as applicable). Issues arise as the terms of the partnership agreements often provide that granting a direct or indirect security interest, as well as any future transfer which may be effected as a result of security enforcement, will require consent of the fund’s general partner. General partners who are solicited for consent can be unresponsive and in some cases might object to the future admittance of a lender (or its transferee) as a limited partner in their fund. Clearly it would benefit neither the borrower nor the lender for the borrower to be in breach of such consent requirements as any potential breach could ultimately affect the value of the underlying portfolio.

As a result, a compromise can be reached in bifurcating the approach on investments depending on their impact on the borrowing base. The borrower and lender may set out criteria and thresholds to delineate the key investments making up the borrowing base from the lender’s perspective, for which consent, if required pursuant to the fund documents, must be expressly obtained. For the remaining, otherwise eligible but less substantial investments, an approach of deemed consent may be taken whereby, again where consent is required, evidence that the GP has been contacted and no express objection provided will be sufficient to include such investment into the eligible portfolio. This solution aims to resolve this potential issue on a risk-based approach which is satisfactory to both borrower and lender as the borrower must have demonstrated active steps taken to obtain necessary consents and the lender has comfort of potential future security enforcement challenges being resolved by either express or deemed consent.

Conclusion

Secondaries fund financing is a valuable tool for sophisticated market participants looking to unlock alternative financing including for building new fund portfolios and financing existing fund structures. Whilst the security arrangements and GP consents can bring some challenges and require careful due diligence, these challenges can be overcome and allow secondary funds to access competitive pricing on leverage terms and enhance their returns.

Fund Finance Webinar Series: “Financing the Fund Lifecycle”

Join us for a series of three webinars in which our multi-jurisdictional fund finance team will explore financing the fund lifecycle through all relevant stages. Our Fund Finance Webinar Series, “Financing the Fund Lifecycle”, starts with Webinar one: The Beginning on Thursday, 22 February 2024 (4 p.m. GMT). Click here to register.