Another source of litigation risk for fund sponsors are claims brought by portfolio company employees. Sponsors should be aware of these risks, particularly when the portfolio company is in distress or is considering a sale or other transaction affecting the disposition of shares in the company. We have set forth below just a few examples of litigation that can be brought against the fund, sponsor, and board designees by portfolio company employees, likely triggering at least indemnity considerations (which need to be evaluated in connection with insurance and indemnity at the portfolio company level), and might also affect the value of the portfolio company and in turn the value of the fund’s assets.

Employee Shareholder Claims

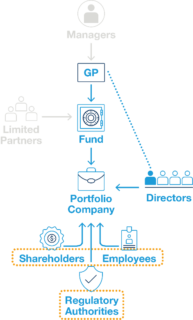

As discussed in prior posts, a fund sponsor’s designation of its own partners as portfolio company board directors provides some measure of control over the company, but also creates potential exposure for the sponsor. For example, in a major company transaction, there may be a divergence of the fund’s interests (as a shareholder) from certain of its fellow shareholders (such as employees who hold a different class of equity interests) and even the company itself. That divergence of interests may be particularly acute between common shareholders and preferred shareholders, whose preference shares may give them priority in the distribution of any proceeds of a sale. Often, a fund will hold some combination of preferred shares and common shares, particularly if the investment was made at a later stage in the life of the portfolio company, whereas employees often hold common shares.

Examples of unequal rights and restrictions between share classes include voting preferences, liquidation preferences, and anti-dilution preferences. These preferences can produce wildly divergent outcomes between shareholders, leading to disputes. Employees holding common shares may claim that a director – and particularly a fund designee – breached their duties to the company and the shareholders by voting for a transaction that produced a disproportionately favorable outcome for the fund.

Given this background, fund sponsors should consider the risk of an employee shareholder lawsuit against the company, its directors, and even the sponsor entities, in the dissolution or sale of a portfolio company. Employees holding common shares may be inclined to sue if they believe the value of their shares was impaired disproportionately and unfairly relative to other share classes in the dissolution or sale. Additionally, if a director is also a representative of a fund that owns preferred shares, the employees may allege that the director was conflicted and favored the preferred shareholders over common shareholders in the sale to maximize the fund’s investment. With increasing frequency, fund sponsors (along with the share-holding fund(s)) are named directly as defendants, and accused of aiding these alleged breaches of fiduciary duties. At a minimum, the fund is indirectly at risk because of its indemnification obligations to the board designee and through the financial risk.

Conflicts can also arise when employee shareholders feel aggrieved (whether warranted or not) by the differential treatment of their common shares as compared to shares of preferred shareholders. For example, preference shareholders of a portfolio company may be able to sell in a secondary market stock transaction, while employee common shareholders are often blocked from these transactions. Similarly, when a portfolio company faces liquidity issues, it may seek convertible debt or equity financing. Cram-down financing may disproportionately dilute the value of employees’ common shares and cause employees to seek to recover their lost value through litigation.

WARN Act Claims

Delaware courts have allowed WARN Act class action suits against fund sponsors, in addition to the portfolio company’s management. Again, this is a situation where increased control by a fund sponsor equates to increased litigation exposure. Both federal and state WARN Acts obligate companies to warn employees if the company can reasonably foresee that it will not be able to meet payroll. The key consideration in determining potential direct liability of a fund sponsor is how much control the sponsor exercised over decisions and operations at the company. Even if the fund sponsor is not involved sufficiently to be named as a defendant itself, it can still face indirect risk in a Warn Act case through its indemnity obligations to board designees who are often named as defendants in WARN Act lawsuits.

Whistleblower Claims

We have seen more whistleblower activity, in increasingly high-profile cases with high rewards, where employee whistleblowers are exposing inconsistencies and financial impropriety relating to valuations, including 409A option valuations and impairments to goodwill, particularly for acquisitive portfolio companies. Additionally, a flag raised on how a portfolio company is valuing itself could trigger an interest in how the fund sponsor is valuing the company for purposes of its own accounting and reporting, particularly when the sponsor has one of its own members on portfolio company board.

ERISA Stock-Drop Claims

Boards and board committees with responsibility for administering employee retirement plans that contain the option to buy company stock are under the obligation to ensure that maintaining the stock fund option is prudent—i.e., for the benefit of the employee participants of the plan. Directors with fiduciary responsibility for the plan run the risk of litigation of claims under ERISA if an employee elects to invest some of his/her plan holdings in the stock, yet the board knows something about the health of the company that would make it imprudent for the stock to be available for plan investment. Plaintiffs in these cases face a high pleading standard, but history guides that employees will still pursue claims when there has been an impairment in the value of the company affecting their retirement.

For further information regarding how to mitigate risks, such as those above, contact us regarding The Portfolio Company Playbook: A Fund Sponsor’s Guide to Risks and Liability.

Keep an eye out for Chapter 4 of the playbook, which will cover navigating additional sources of direct liability risks to the fund.

[View source.]