Corporate Chapter 11 filings remained relatively low in 2014, down slightly from 2013, due to a robust capital market environment, low interest rates and easy access to financing. These and other factors allowed highly leveraged borrowers that might otherwise have been Chapter 11 restructuring candidates to refinance or pursue other nonjudicial restructuring alternatives. Among those companies that filed corporate bankruptcies, the District of Delaware and the Southern District of New York continued to capture the lion's share of cases. An examination of available statistics for Chapter 11 filings reveals that these dynamics are consistent with trends which span several years.

Chapter 11 Filing Volume

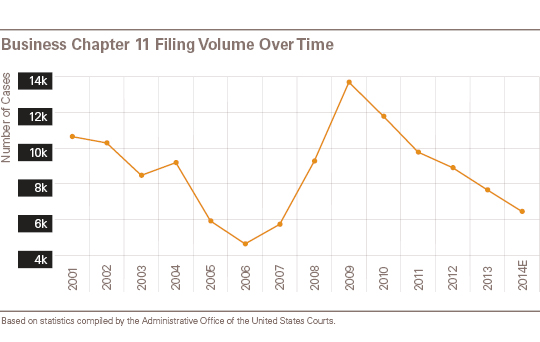

Chapter 11 filings increased exponentially during 2008 and 2009, followed by a steady decline in filing volume after 2010. An estimated 6,453 business bankruptcies were filed in 2014 (based on the data available at the time of writing), down 16 percent from 2013 and 53 percent from the peak of 2009. Nonetheless, corporate bankruptcy filings in 2014 remained 40 percent above the historic low in 2006. The chart immediately below depicts Chapter 11 filing volume over time.

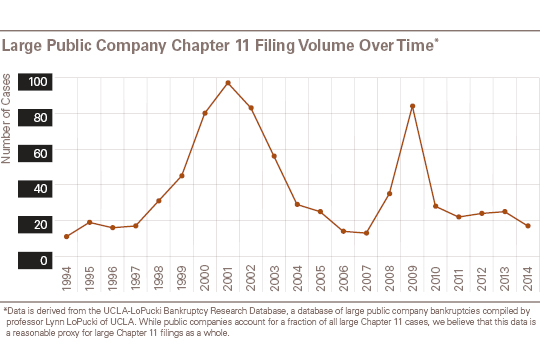

Large public company Chapter 11 filings (i.e., public companies with assets greater than $280 million) follow similar trends. Such filings peaked during each of the last two recessions, followed by a rapid reversion to historic rates. Only 17 large public companies filed Chapter 11 cases in 2014, slightly below the average of 21.7 cases filed in nonpeak years and well below the more than 80 annual filings of large companies in 2001 and 2002 as well as 2009. The chart immediately below shows the volume of large public company Chapter 11 cases over time.

Venue

The District of Delaware and the Southern District of New York attracted more than 14 percent of all 2014 corporate bankruptcy cases filed (measured as of the end of September 2014) and 17 percent of all such cases filed since 2001. These jurisdictions have received an even larger share of large public company Chapter 11 filings. Since 1980, 36 percent of such cases have been filed in the District of Delaware and 20 percent have been filed in the Southern District of New York. By comparison, the next most-frequent venue (the Northern District of Texas) accounted for less than 4 percent of all large public company filings during the same period. These venue trends have intensified in recent years, with the District of Delaware and the Southern District of New York attracting more than 75 percent of large public company filings since 2010. The chart immediately below shows venue selection in large public company cases from 2010 to present.

The concentration of Chapter 11 cases in Delaware and the Southern District of New York has led to criticism of the current venue statute, which some have alleged leads to opportunistic forum shopping. Conversely, defenders of the current statute argue that the frequency of Chapter 11 filings in Delaware and the Southern District of New York is attributable to the convenience, experience and established case law of these jurisdictions. It remains to be seen whether Republican control of the Senate will increase the likelihood of venue changes in the coming years.

The concentration of Chapter 11 cases in Delaware and the Southern District of New York has led to criticism of the current venue statute, which some have alleged leads to opportunistic forum shopping. Conversely, defenders of the current statute argue that the frequency of Chapter 11 filings in Delaware and the Southern District of New York is attributable to the convenience, experience and established case law of these jurisdictions. It remains to be seen whether Republican control of the Senate will increase the likelihood of venue changes in the coming years.

Proposed Reforms to Chapter 11

The American Bankruptcy Institute's Commission to Study the Reform of Chapter 11 recently released its Final Report recommending comprehensive reforms to Chapter 11 of the Bankruptcy Code. The report is the culmination of a three-year effort by over 150 restructuring professionals to evaluate Chapter 11 in light of the changing environment in which financially distressed companies operate. Notable recommendations for reform include:

-

Adequate protection would be determined based on the foreclosure value of the secured creditor's collateral.

-

DIP financing orders cannot impose milestones requiring the debtor to perform material tasks within the first 60 days (e.g., conduct a sale or file a plan).

-

No 363 sales of all or substantially all assets (363x sales) within the first 60 days unless the debtor demonstrates by clear and convincing evidence a high likelihood that the value of the debtor's assets will decrease significantly.

-

363x sales must satisfy requirements similar to plan confirmation requirements.

-

Junior, out-of-the-money stakeholders may be entitled to receive an allocation of value from senior creditors to reflect a possible upswing in the reorganized debtor's value.

-

The cost of capital for similar debt issued to companies comparable to the debtor as a reorganized entity should be used when determining the appropriate discount rate for purposes of cram down.

-

Elimination of the requirement of at least one impaired accepting class of creditors for plan confirmation.

-

No appointment of an unsecured creditors' committee if the general unsecured creditors do not need representation in the case (e.g., if their claims are out-of-the-money).

It remains to be seen which, if any, of the ABI's recommendations will gain traction with Congress and result in changes to Chapter 11. A more fulsome analysis of the ABI's report is the subject of a separate update.