Stakeholders across London's capital markets are ready to seize the opportunity to reform and reenergize IPO activity in one of the world's most important financial centers

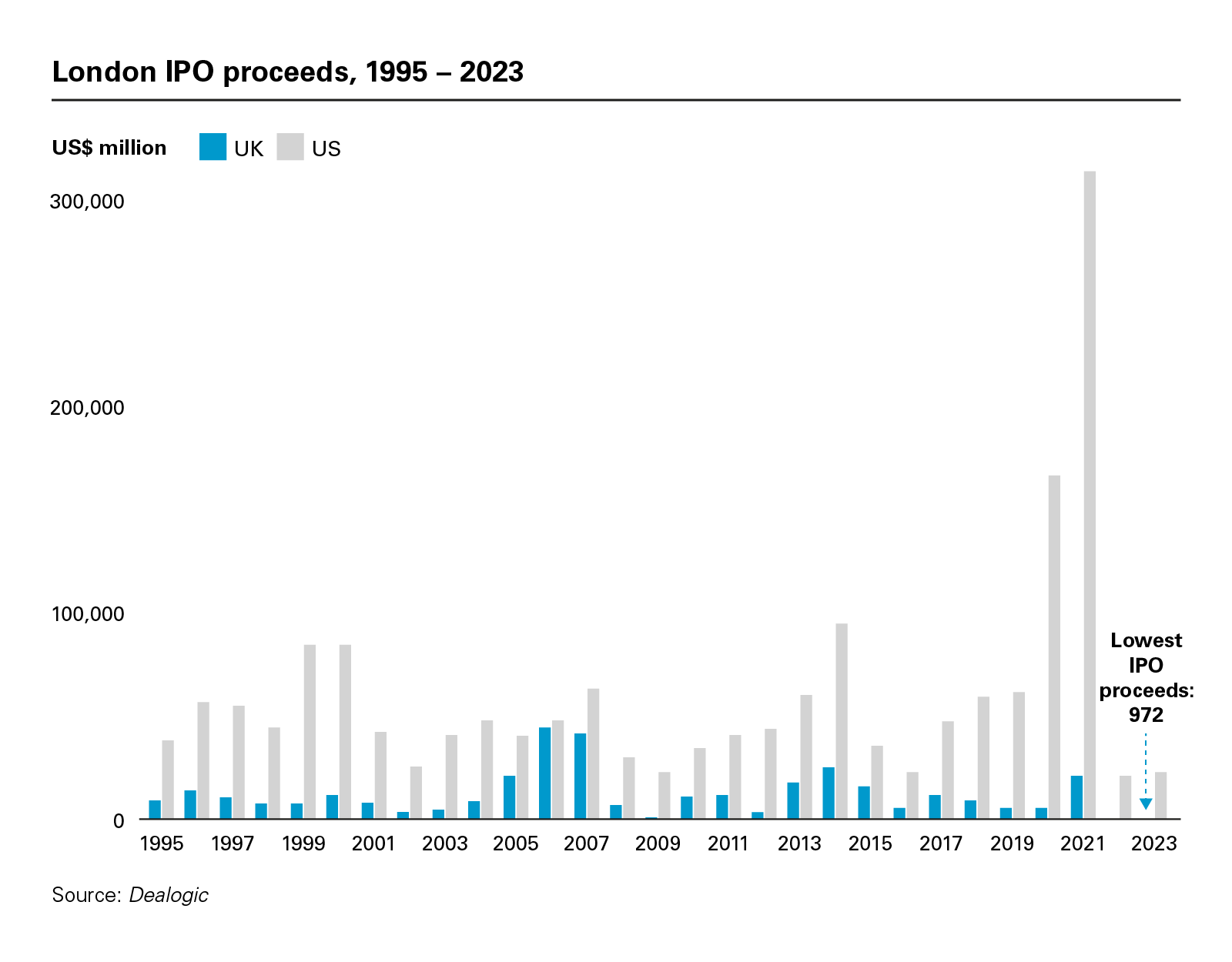

Along with other stock exchanges across the world, the London Stock Exchange (LSE) had a challenging 2023, recording only 23 new listings with a total value of less than US$1 billion. This represented a 23 percent year-on-year decline in IPO proceeds and a 53 percent drop in the IPO count. The LSE was not alone—EMEA IPO proceeds dropped by 44 percent year-on-year in 2023, with the IPO count down by almost a third.

View full image: London IPO proceeds, 1995 – 2023 (PDF)

As with other global markets, rising interest rates, high inflation and geopolitical uncertainty were among the factors contributing to the slow LSE IPO activity in 2023. In addition, the LSE has had to contend with other long-term challenges that have put the brakes on potential IPO activity.

Nonetheless, stakeholders in the London market are optimistic that the reforms to the UK listing rules and a collective willingness to direct more domestic investment into London-listed companies present a generational opportunity to reinvigorate the competitiveness of London as a listing venue.

IPO issuers look elsewhere as liquidity dries up

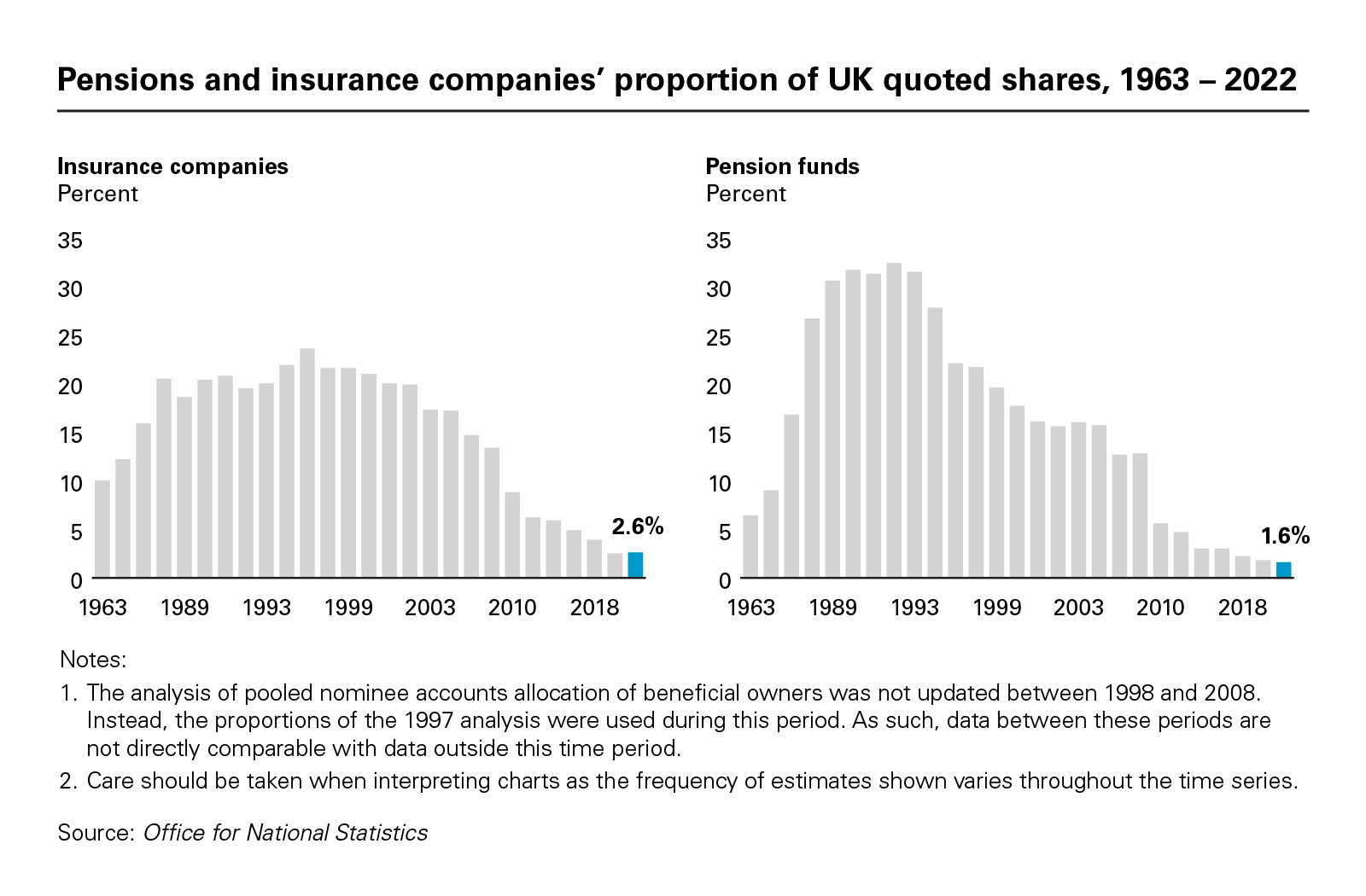

One of the most significant challenges facing the LSE has been the gradual decline of institutional investment in UK equities.

According to the UK's Office for National Statistics (ONS), insurance and pension funds held only 4.2 percent of UK listed shares at the end of 2022. This figure is in marked contrast to the 45.7 percent reported by ONS in 1997.

View full image: Pensions and insurance companies’ proportion of UK quoted shares, 1963 – 2022 (PDF)

View full image: Pensions and insurance companies’ proportion of UK quoted shares, 1963 – 2022 (PDF)

Investors seeking more profitable returns in the international markets could be one driver of the outflows, but many commentators have pointed to changes to accounting standards in 2000. Since then, companies have been required to calculate the surplus or deficit of their defined benefit pension schemes annually and to disclose deficits as a financial liability in their accounts. This may have prompted companies to shift pension funds away from UK shares to lower-risk assets such as corporate and government bonds.

The UK listing rules have also been a focus for market participants seeking to enhance London's competitiveness as a listing venue. The need for premium listed companies to obtain shareholder approval for significant transactions and related party transactions and the prohibition on dual class share structures have been highlighted as examples of areas in which London's rules are more onerous than competing exchanges.

The decline in UK institutional investment in UK equities and the UK's regulatory framework have undoubtedly impacted London's competitiveness, and this has given rise to issuers looking at other exchanges, especially with respect to certain sectors—tech and biotech in particular. However, whether UK companies would be better served listing in New York rather than London is a nuanced consideration. The data show that, on a five-year look back, the majority of UK companies that have listed in New York have suffered material reductions in their market value. So, with certain specific and limited exceptions, it is by no means clear that UK companies would be better served by listing in New York rather than London.

Change presents opportunity

The challenges facing the LSE have not gone unnoticed. There is a growing sense of cohesion and alignment across all stakeholder groups, including politicians (of both major parties in the UK), investors, companies, regulators, advisers and the LSE, on the need for change to reinvigorate the equity capital markets in London.

After a period of extensive consultation, the UK's Financial Conduct Authority is moving ahead with a program of reforms that will overhaul the UK listing framework and present a more competitive proposition to potential IPO candidates.

The package of reforms is designed to streamline the eligibility requirements applicable to IPO candidates and the ongoing obligations with which they will have to comply after listing. As such, more emphasis will be placed on ensuring that investors have all the appropriate information they need to make their investment decision. The reforms will include combining the premium and standard listing segments into one listing category for equity shares of commercial companies; removing the requirement for shareholder approval for significant M&A and related party transactions; and allowing dual-class share structures.

It is anticipated that these changes will bring London into alignment with the US and European stock exchanges and put the LSE in a better position to compete for IPOs.

However, "leveling up" the UK's listing regime rules is just one piece of the puzzle. The UK's pension system and its executive compensation and approach to taxation are some of the other potential areas for reform. Focusing on the pension system, consolidating the UK's fragmented pension market is another lever, with significant potential to improve liquidity in London's equity markets.

The UK has the second-largest pool of long-term capital in the world, with close to £5 trillion held in pension and insurance funds, according to Citi and asset manager abrdn. This capital, however, is highly fragmented. There are more than 3,000 defined contribution schemes in the UK managing around £600 billion in total assets (£200 million each on average). There are also more than 5,000 defined benefit schemes in the UK, three-quarters of which have less than £100 million in assets.

Compared to other pension systems in the world (for example, in Australia, there are 120 "super" schemes with around £10 billion in assets each), the fragmented UK system has made it more difficult to diversify and manage risk. Consolidating the UK's schemes will help to diversify bond-heavy allocations and support more capital flows into UK equities.

Policymakers have seen the value in the consolidation of pension funds. In the 2023 Autumn Statement, Chancellor Jeremy Hunt outlined a program to have the majority of defined contribution plans managed in schemes of more than £30 billion and for local government pension funds to be consolidated into pools of £200 billion or more.

UK pension fund consolidation will be complex and challenging. But there appears to be a willingness across the board to make progress on this front and seize what many stakeholders see as a once-in-a-generation opportunity to drive change and reenergize IPO activity in London in the months and years ahead.