For the upcoming 2024 proxy and annual reporting season, there are a number of key issues to consider and keep an eye on for further developments as preparations commence. This alert provides an overview of these issues and updates in several key areas, including, among others, Securities and Exchange Commission (SEC) disclosure and filing requirements, pending SEC rulemaking, executive compensation matters, and corporate governance trends.

SEC Updates/Trends

Uptick in SEC Comment Letters (Authors: Todd J. Thorson and Brittany Stevenson)

Pursuant to Section 408 of the Sarbanes-Oxley Act, the SEC is tasked with reviewing the filings of companies made under the Securities Exchange Act of 1934, as amended (the Exchange Act), every three years to improve disclosure and financial reporting. However, many companies undergo more frequent reviews, which can encompass the full filing, only the financial statements and related disclosures, or a specific review of certain items of disclosure. Regardless of the scope of review, the frequency of publicly issued SEC comment letters and the number of registrants receiving SEC comment letters in the 12 months ended June 30 have substantially increased, surpassing the number of letters issued in each of the past four years.[1] The topics producing the highest volume of comments include the following:

- Non-GAAP Measures: The emphasis on non-GAAP measures may stem from challenges in applying previous SEC guidance. However, in December 2022, the SEC provided new guidance to clarify existing SEC views and provide further guidance on non-GAAP measures the SEC considers misleading.

- Management’s Discussion and Analysis (MD&A): The SEC’s comments on MD&A have generally focused on (i) the disclosure and analysis of results of operations, (ii) the disclosure of known trends or uncertainties that are expected to impact results, (ii) the metrics management uses to assess performance, (iv) critical accounting estimates, and (v) liquidity and capital concerns.

- Segment Reporting: The SEC’s comments on segment reporting typically involve confirming how a registrant identified its operating segments and how those segments were aggregated into reportable segments. Additionally, the SEC may consider company disclosure on websites or earnings calls, including with respect to any material acquisitions or dispositions or changes in personnel or organizational structure.

- Revenue Recognition: As ASC 606, Revenue from contracts with customers, requires companies to disclose certain qualitative and quantitative information regarding customer contracts, the SEC’s comments have typically addressed performance obligations, transaction prices, any variable considerations, revenue recognition, the gross versus net presentation and any disaggregated revenue.

While predicting future SEC comment letter trends is challenging, the trends described above are expected to continue, and companies should take these into account as they prepare for the 2024 proxy and annual reporting season.

Status of Adopted and Pending SEC Proposals/Related Guidance

Climate Change Rules (Author: Salmon Hossein)

The SEC’s climate change disclosure rules are one of the most consequential and closely watched undertakings of the agency under SEC Chair Gary Gensler’s tenure. The ambitious rules are intended to increase transparency and reporting on climate-related risks for every public company in the United States.

Climate change is one of the most important policy priorities of President Joe Biden’s Administration, and Gensler initially wanted to issue a proposal by the end of 2021. However, since ultimately presenting the March 2022 proposal in Release No. 33-11042, The Enhancement and Standardization of Climate-Related Disclosures for Investors, the SEC has delayed finalizing these rules several times. The delays stem in part from immense public engagement and the far-reaching implications of such a rule change for public companies. The SEC is paying particular attention to the feasibility of Scope 3 reporting, which would track indirect emissions that are caused by a business’s customers or supply chain. Gensler acknowledged that changes will likely be made to Scope 3, as critics remain concerned about anticipated compliance costs and the burden of accurate reporting. Gensler clarified his intention is “only regulating the public companies and not somehow indirectly the private companies.” Regardless of how the proposed rules shake out, the rules will ultimately require public companies to accelerate the capture, measurement and disclosure of emissions data. Though the SEC maintains it is not creating new climate regulations but merely drafting new rules for financial reporting, even such a rule change will significantly impact all publicly traded companies. The timing for final adoption, which was anticipated for the end of this year, is uncertain. The SEC has hinted in recent public speeches that it may seek further public comment and it is expected that there will be legal challenges to the rules upon adoption.

For additional information on these proposed rules, see our alert “SEC Proposes Rules for Climate-Related Disclosures and Extends Deadline for Public Comments,” dated May 11, 2022.

Rules for New 10b5-1 Plans and Insider Trading Policies (Authors: Jennifer R. Rodriguez and Macy T. Munz)

In December 2022, the SEC adopted amendments to Rule 10b5-1 under the Exchange Act and enhanced disclosure requirements in an attempt to establish guardrails around the use of Rule 10b5-1 trading plans and strengthen protections against insider trading. Amendments to Rule 10b5-1(c)(1) add several conditions to and limitations on the availability of the affirmative defense to liability for insider trading under Rule 10b5-1. Enhanced disclosure obligations include new disclosure requirements in an issuer’s periodic reports and proxy statements. Among them are (i) annual disclosure of an issuer’s insider trading policies and procedures, (ii) quarterly disclosure regarding the adoption and termination (including modification) of Rule 10b5-1 and certain other written trading arrangements by directors and officers, and (iii) annual disclosure regarding an issuer’s policies and procedures for granting options in advance of the release of material nonpublic information, together with tabular information setting forth certain information regarding equity-based awards granted to officers and directors close in time to the issuer’s disclosure of material nonpublic information (discussed in more detail below under “Stock Option Grant Disclosures”). The amendments to Rule 10b5-1(c)(1) add the following conditions to and limitations on the availability of the affirmative defense to liability for insider trading under Rule 10b5-1:

- Cooling-off period: A minimum “cooling off” period after the adoption or modification of a Rule 10b5-1 trading arrangement of (i) 120 days for a director or officer (as defined in Rule 16a-1(f) under the Exchange Act) and (ii) 30 days for the issuer, in each case, before trading may begin under the new or modified trading arrangement.

- Director and officer certifications: At the time of adopting or modifying a Rule 10b5-1 trading arrangement, directors and officers would be required to provide to the issuer a written certification that states: (i) that they were not aware of material nonpublic information regarding the issuer or its securities, and (ii) that they are adopting the plan in good faith.

- Restriction on overlapping trading arrangements: The affirmative defense under Rule 10b5-1 would not be available for multiple, overlapping trading arrangements for open market trades in the same class of securities.

- Restriction on single-trade arrangements: The affirmative defense under Rule 10b5-1 would be available for only one single-trade plan in any 12-month period.

- Good faith requirement: A Rule 10b5-1 trading arrangement must be entered into and operated in good faith and not as part of a plan to evade the rule.

Additional changes were made with respect to Forms 4 and 5 filed by Section 16 reporting persons, as summarized below under the section titled “Forms 4 and 5 Reporting.”

The changes summarized above took effect on Feb. 27, subject to phase-in periods for the new disclosure requirements applicable to issuers and Section 16 reporting persons. The new disclosures in periodic reports on Forms 10-Q, 10-K and 20-F and proxy statements discussed herein are or will be required in the first filing that covers the first full fiscal period beginning on or after (i) for smaller reporting companies, Oct. 1, and (ii) for all other issuers, April 1. The changes pertaining to Section 16 reports described below are effective for reports filed on or after April 1. For additional information on these amendments, see our alert “SEC Amends Rule 10b5-1 Trading Arrangement Conditions and Disclosure Requirements for Issuers and Section 16 Reporting Persons to Enhance Insider Trading Protections,” dated Dec. 20, 2022.

Share Repurchase Disclosures (Authors: Jennifer R. Rodriguez, Joseph P. Boeckman and Lance S. Tupikin)

On May 3, the SEC adopted final amendments to the disclosure requirements regarding purchases of equity securities made by or on behalf of an issuer or an affiliated purchaser. However, the amendments were challenged soon after their adoption in a lawsuit filed by the U.S. Chamber of Commerce and two other petitioners, and, on Oct. 31, the U.S. Court of Appeals for the 5th Circuit agreed with certain arguments by petitioners that the amendments were “arbitrary and capricious” and therefore in violation of the Administrative Procedure Act and subject to invalidation. In reaching its conclusion, the court laid out a fairly incisive critique of the process the SEC employed in its adoption of the amendments. First, the court found that the SEC had failed to adequately substantiate the amendments’ costs and benefits. It said that the SEC had not established its threshold proposition that opportunistic or improperly motivated stock buybacks are “genuine problems” for investors; therefore, the primary benefit of the amendments was not proven and none of the costs justified. Second, the court determined that the SEC made a critical error in not considering significant comments submitted by petitioners during the amendments’ comment period.

Rather than invalidating the amendments immediately, the court remanded them for 30 days, giving the SEC a limited opportunity, until Nov. 30, to correct the noted deficiencies. On Nov. 22, the SEC sought an extension of this 30-day period and stayed the rules pending further action, but the extension was denied by the court on Nov. 26. On Dec. 1, the SEC’s Office of General Counsel submitted a letter to the court in which the agency conceded that it was “not able to ‘to correct the defects in the rule,’ … within 30 days of the Court’s opinion.” Consequently, the rule will likely be vacated. The SEC may appeal the court’s decision or attempt to craft a new proposal that addresses the deficiencies identified by the court; in either case, there will be a delay in implementation, relieving issuers who would have otherwise had to comply with the amendments in their upcoming 10-Ks from having to do so for now. In the meantime, issuers remain required to report share repurchases, consistent with existing requirements.

The amendments represented an attempt by the SEC to address an information imbalance between issuers and investors that may affect investors’ investment decisions. The SEC asserts that because issuers are not required to disclose the reasons for share repurchases, investors are left to make inferences about an issuer’s beliefs about its stock value or whether the buyback was used to achieve compensation or earnings targets, which inferences may or may not turn into faulty premises for their investment decisions relating to the stock.

To remedy this information imbalance, the amendments would have required issuers to, among other things, disclose the following information on a quarterly basis in their Forms 10-Q and 10-K:

- Specified daily quantitative repurchase data.

- The objectives or rationales for the respective share repurchases and the process or criteria used to determine the amount of repurchases, along with any policies and procedures related to purchases and sales of securities during a repurchase program by their officers and directors, including any restrictions on such transactions.

- Information about an issuer’s adoption and termination of Rule 10b5-1 trading arrangements, including a description of the material terms of the arrangement, such as the date of adoption, duration and aggregate number of securities to be purchased or sold.

Issuers would also have been required to check a box indicating whether any officers or directors subject to Section 16 traded in the relevant securities within four business days before or after the public announcement of a repurchase plan or program. New Form F-SR would have imposed daily quantitative data disclosure obligations on foreign private issuers that repurchase their shares, with the filing due within 45 days following the end of such issuer’s fiscal quarter. Additionally, issuers would have needed to tag all disclosure information required in both the daily and periodic disclosures by using Inline eXtensible Business Reporting Language (XBRL). For additional information on this proposal, see our alert “SEC Adopts Amendments to Share Repurchase Disclosures,” dated May 15.

For most issuers, the enhanced disclosure requirements were to become effective for Forms 10-K for the year ending Dec. 31.

The SEC indicated that it was proceeding with the remedial steps to address the court’s concerns before the 30-day timeframe expired, so the SEC may continue this work to issue an alternative proposal for reporting additional details regarding share repurchases. As a result, issuers should continue to consider how their repurchase activity and insider transactions and related policies would fit into enhanced disclosure requirements. For additional information on this ruling, see our alert “SEC Amendments Requiring Enhanced Share Repurchase Disclosure Hang in the Balance After Federal Appeals Court Directs SEC to Correct Defects,” dated Nov. 9.

Cybersecurity Incident, Risk Management, Strategy and Governance Disclosures (Authors: Janet A. Spreen and John J. Harrington)

In July, the SEC adopted new rules to enhance and standardize disclosures regarding cybersecurity risk management, strategy, governance and incidents. The rules require reporting companies to file a Form 8-K under a new Item 1.05 to report certain information in the event of a material cybersecurity incident. The rules also require reporting companies to describe in their annual reports under new Regulation S-K Item 106 their processes for assessing, identifying and managing material cybersecurity risks, and whether cybersecurity risks have materially affected or are reasonably likely to have a material effect on the company. This annual disclosure must also describe the roles of the board of directors and management in overseeing and managing material cybersecurity risks.

To be prepared for the new Form 8-K Item 1.05 reporting requirement, companies are advised to ensure their incident assessment and disclosure protocols facilitate timely disclosure of material incidents. As they prepare the new annual disclosures, companies will also need to take stock of their current processes for and the role of management in assessing, identifying and managing material cybersecurity risks, as well as how the board provides oversight with respect to these risks.

All registrants must provide the annual disclosures required by Regulation S-K Item 106 in annual reports for fiscal years ending on or after Dec. 15. All registrants other than smaller reporting companies must begin complying with Form 8-K Item 1.05 on Dec. 18. Smaller reporting companies must begin complying on June 15, 2024.

For additional information on these rules, see our alert “Addressing the SEC’s New Cybersecurity Risk Management, Strategy, Governance and Incident Disclosure Requirements,” dated Oct. 27.

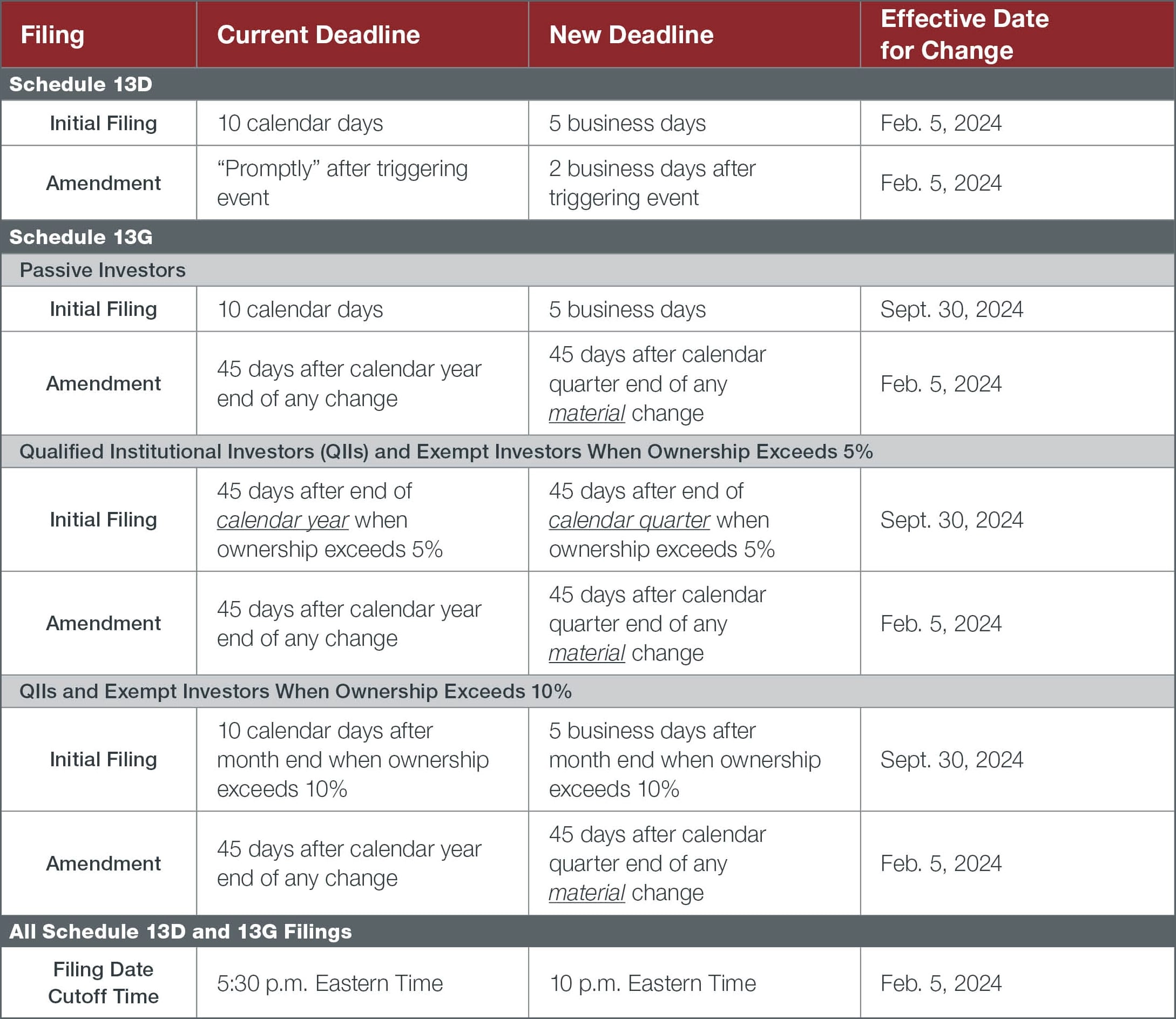

Accelerated Deadlines for Schedule 13D and 13G Filings (Authors: Samuel F. Toth and Janet A. Spreen)

On Oct. 10, the SEC adopted amendments to Sections 13(d) and 13(g) of the Exchange Act that are intended to provide investors with more timely information on the positions of key market participants. The final rules accelerate the filing deadlines for Schedules 13D and 13G, clarify disclosure requirements with respect to derivative securities, require filings to be made with machine-readable data language, and provide additional guidance on other beneficial ownership reporting rules.

Accelerated Filing Deadlines

The rule release also provided:

- Structured Data Language: Beginning Dec. 18, 2024, all Schedules 13D and 13G, except for exhibits attached to such filings, will be required to be filed using structured, machine-readable data language. Filings will be submitted through the Electronic Data Gathering, Analysis, and Retrieval (EDGAR) platform using XML-based language.

- Derivative Securities: The SEC adopted an amendment to Item 6 of Schedule 13D clarifying that a person filing a Schedule 13D is required to disclose interests in all derivative securities that use the issuer’s equity security as a reference security. However, the SEC declined to adopt a bright-line rule that deemed certain holders of cash-settled derivative securities as beneficial owners of the reference covered class, instead deferring to existing guidance requiring an analysis of the facts and circumstances.

- Group Formation: The SEC gave additional guidance regarding when formation of a “group” occurs for the purpose of determining whether the 5 percent beneficial ownership threshold has been triggered as a result of communications by two or more persons for the purpose of acquiring, holding or disposing of securities of an issuer. The SEC provided examples of types of communications that would likely not rise to the formation of a group, including (i) shareholders communicating with each other regarding an issuer or its securities but taking no further actions, (ii) shareholders engaging in discussions with an issuer’s management without taking any further actions, and (iii) shareholders jointly submitting a nonbinding shareholder proposal to an issuer. However, the SEC cautioned that if a beneficial owner of a substantial block of a covered class that will be a Schedule 13D filer intentionally communicates to other market participants that its Schedule 13D filing will be made, the engaged parties are likely to be considered a group if the communications had the intention of causing market participants to purchase the same class of covered security.

The effective date of the amendments is Feb. 5, 2024; however, compliance with the revised Schedule 13G filing deadlines will not apply until Sept. 30, 2024, and compliance with the structured data requirement for Schedules 13D and 13G will not apply until Dec. 18, 2024.

Forms 4 and 5 Reporting (Author: Samuel F. Toth)

Accelerated Reporting and Increased Scrutiny of Gifts

In 2022, the SEC amended Rule 16a-3 to require prompt reporting of bona fide gifts made or received by Section 16 insiders. As a result, these gifts must now be reported on Form 4 within two business days after the transaction date, similar to other reportable transactions. Gifts made prior to Feb. 27, 2023 remain eligible for delayed reporting on Form 5, which is due within 45 days after the end of the fiscal year in which the gift was made.

In its final rule release, the SEC acknowledged that when gifts are closely followed by a sale by the donee, under conditions where the value at the time of the donation and sale affects the tax or other benefits realized by the donor, such gifts can raise policy concerns similar to those of more common forms of insider trading, and may subject the donor to insider trading liability. Nevertheless, the SEC clarified that the affirmative defense of Rule 10b5-1(c)(1) is also available for bona fide gifts. For example, an insider may enter into a binding arrangement instructing their tax advisor to gift a certain number of shares to a charitable organization based on a traditional algorithm or formula or based on achieving certain tax objectives.

New Checkbox and Disclosure for Rule 10b5-1 Trades

Effective April 1, Forms 4 and 5 were amended to add a Rule 10b5-1 checkbox, which requires the Section 16 reporting person to indicate whether a transaction reported on such form was made pursuant to a Rule 10b5-1 trading plan. Furthermore, the instructions to Forms 4 and 5 were amended to require insiders to disclose by footnote the date such Rule 10b5-1 trading plan was adopted.

Rules for Forms 144 (Authors: Brittany Stevenson and David H. Brown)

Electronic Filing of Forms 144

On Sept. 23, 2022, the SEC released the electronic version of Form 144, pursuant to the SEC’s June 2022 adopted amendments that require all Forms 144 to be filed electronically on EDGAR. Prior to the adopted rule change, Form 144 was permitted to be submitted either electronically via EDGAR or in paper form, but Form 144 had almost always exclusively been submitted in paper form rather than in electronic form. Generally, Form 144 must be filed by an affiliate of a reporting company relying on Rule 144 for a resale transaction, as a notice of a proposed sale of that company’s stock when the amount to be sold during any three-month period (i) exceeds 5,000 shares or units or (ii) has an aggregate sales price greater than $50,000.

The SEC expressed its anticipation that requiring electronic submission will provide investors with easier, online access to material information and increase efficiency for market participants by lowering expenses related to paper filings. To be able to comply with the electronic filing form process, potential affiliates that may be required to file Forms 144 should obtain or confirm the EDGAR codes needed to make the electronic filings. If a potential affiliate does not have the necessary EDGAR codes, then such affiliate should apply for such codes as soon as possible, since these applications are not automatically granted by the SEC, and are sometimes subject to further SEC inquiry during the application process. The deadline to comply with the electronic filing requirement was April 13.

Extension of Filing Deadline for Forms 144

On Feb. 21, the SEC adopted amendments to Regulation S-T that extended the filing deadline for Form 144 from 5:30 p.m. to 10:00 p.m. Eastern Standard Time. The deadline for filing Form 144 is the same day that the affiliate places its sell order to sell stock; this deadline is notably earlier than the deadline for reporting the same sale on Form 4 or on Schedule 13D or 13G. The SEC expressed its belief that these amendments will ease the burden on sellers, brokers, counsels and other professionals who must file Form 144 on the same day as placing the sell order, since it is not unusual for sellers who must file Form 144 to be unaware of the requirement to file the form until near the close of the trading day at 4:00 p.m. Eastern Standard Time. The amendments became effective March 20.

Securities Transaction Settlement Cycles (Author: David H. Brown)

On Feb. 15, the SEC adopted amendments to Rule 15c6-1 in order to shorten the standard settlement cycle for most routine broker-dealer securities transactions from two business days after the trade date (T+2) to one business day after the trade date (T+1). The final rule also adopts the new Rule 15c6-2, which aligns the new shortened settlement cycle with how broker-dealers, investment advisors and clearing agencies process institutional trades.

The adopted amendment prohibits broker-dealers from “effecting or entering into a contract for the purchase or sale of a security (other than an exempted security, a government security, a municipal security, commercial paper, bankers’ acceptances, or commercial bills) that provides for payment of funds and delivery of securities later than the first business day after the date of the contract unless otherwise expressly agreed to by the parties at the time of the transaction.” Notably, the rule also shortens the standard settlement cycle to T+2 for firm commitment underwritten offerings registered under the Securities Act of 1933 (the Securities Act) that are priced after 4:30 p.m. Eastern Standard Time.

The new Rule 15c6-2 will require broker-dealers who engage in allocation, confirmation or affirmation processes with another party or parties to facilitate settlement of a securities transaction subject to the T+1 settlement cycle. Practically, broker-dealers are required to (i) enter into written agreements with the relevant parties to ensure completion of the process as soon as technologically possible and no later than the end of the trade date or (ii) establish, maintain and enforce written policies and procedures reasonably designed to ensure the completion of the process as soon as technologically possible and no later than the end of the trade day.

The adopted amendments are the second time that the SEC has modified Rule 15c6-1 to shorten the settlement cycle since establishing the rule in 1993. Since then, the SEC has devoted significant analysis to address perceived counterparty risk created from multiday settlement times. In response to the market volatility that resulted from the COVID-19 outbreak and the volatility associated with trading of “meme” stocks, the SEC proposed the T+1 settlement amendments in order to shorten the settlement cycle and reduce the overall number of unsettled trades at any given time, decrease the total market value of unsettled trades, and improve the institutional trading processes. Based on the observed improvements in credit, market and liquidity risk from the prior adopted amendments in 2017, the SEC expressed its expectation that these new adopted amendments will produce similar results and encourage technological development to reduce settlement times.

As a result of the adopted amendments, market participants should review agreements related to securities lending, repurchase agreements, margin and swap agreements, and other derivatives transactions to make any necessary adjustments for any mismatched settlement cycles. The amendments became effective on May 5, and compliance will be required beginning on May 28, 2024.

Executive Compensation Matters

Dodd-Frank Clawback Regulation (Authors: Stefan P. Smith, Janet A. Spreen and Lance S. Tupikin)

On Oct. 26, 2022, the SEC announced that it had adopted a final rule (the Release) implementing Dodd-Frank Act provisions that require listed companies to implement, disclose and enforce a compensation recovery policy to claw back or otherwise recover excess incentive-based compensation that executive officers received based on financial reporting measures that are later restated. Thereafter, Nasdaq and the NYSE submitted listing standards that required listed companies to adopt, disclose and enforce a “compensation recovery policy” and, on June 9, the SEC approved the amended listing standards.

The policy must require listed companies to claw back or otherwise recover excess incentive-based compensation that executive officers received based on financial reporting measures that are later restated. Affected executive officers are strictly liable for the recovery, which means that an executive officer need not be culpable with respect to the facts that led to the restatement, and a company may not provide its executive officers with indemnity or insurance to insulate them from recovery. The scope of potential recovery extends to all incentive-based compensation received by any current or former executive officer who served at any time during the three fiscal years prior to when a restatement becomes required (i.e., when the board concludes a restatement is necessary or when it should have reasonably so concluded, or when ordered by a court or agency to restate). Incentive-based compensation is defined to include any compensation that is granted, earned or vested based wholly or in part upon the attainment of a financial reporting measure.

The NYSE listing standards allow for the NYSE to suspend and begin delisting procedures with regard to a listed company upon its determination that a listed company is noncompliant and the listed company does not become compliant within any compliance period provided by the NYSE. Nasdaq did not include delisting procedures in connection with its newly adopted clawback procedures.

All compensation awarded on or after Oct. 2 must be subject to the listed company’s policy and the policy must be adopted by Dec. 2. For additional information on required terms of these clawback policies, see our alert “SEC Approves Final Nasdaq and NYSE Rules Regarding Recovery of Incentive-Based Executive Compensation Awarded in Error with Extended Compliance Deadlines,” dated June 16.

Pay-Versus-Performance Disclosure (Authors: Adam W. Finerman, Stefan P. Smith and Macy T. Munz)

On Aug. 25, 2022, the SEC adopted final pay-versus-performance rules that stem from Dodd-Frank Act provisions, requiring registrants to disclose, in both tabular and narrative format, how their executive compensation is paid in relation to their financial performance.

These rules took effect for annual reports, proxy statements and information statements beginning with the fiscal year ended on or after Dec. 16, 2022; however, registrants continue to have questions regarding the requirements. In an effort to clarify some of the common questions, the SEC released 15 Compliance and Disclosure Interpretations (C&DIs) on Feb. 10, and then an additional 10 C&DIs on Sept. 27, to further clarify the Final Rules. Topics covered by this guidance are discussed in more detail in our alert “SEC Clarifies Dodd-Frank Act Pay-Versus-Performance Rules with New C&DIs,” dated Feb. 24, and our alert “SEC Provides Additional Compliance & Disclosure Interpretations for Further Clarification on Pay-Versus Performance Disclosure,” dated Nov. 8. These topics include:

- 128D.01 – Disclosure Not Required in Form 10-K

- 128D.02 – First-Time NEOs and Prior Equity Awards

- 128D.03 – Footnote Disclosure of Adjustments

- 128D.04 – No Aggregation of Adjustments

- 128D.05 – Compensation Peer Group Selection

- 128D.06 – Calculating TSR for Newly Public Companies

- 128D.07 – Compensation Peer Group Changes

- 128D.08 – Net Income Must Be from Audited GAAP Financial Statements

- 128D.09 – Company-Selected Measure as a Derivation of Net Income or TSR

- 128D.10 – Bona Fide Link Between Financial Performance Measure and Compensation

- 128D.11 – Company-Selected Measure and Multiyear Performance Periods

- 128D.12 – Financial Performance Measures and ‘Pool Plans’

- 128D.13 – Multiple PEOs and Comparative Disclosure

- 228D.01 – Change of Fiscal Year

- 228D.02 – Emergence from Bankruptcy

- 128D.14 – Awards Granted Prior to an Equity Restructuring

- 128D.15 – Awards Granted Prior to an Initial Public Offering

- 128D.16 – Awards That Vest Based on Market-Based Conditions

- 128D.17 – Potential for Vesting in Future Years

- 128D.18 – Retirement Vesting

- 128D.19 – Certification of Performance

- 128D.20 – Valuation Techniques

- 128D.21 – GAAP Methodologies

- 128D.22 – Disclosure of Confidential Information

- 118.08 – Non-GAAP Financial Measures

Stock Option Grant Disclosures (Author: Suzanne K. Hanselman)

The SEC adopted amendments to Item 402 of Regulation S-K designed to provide more transparency on an issuer’s practices on the granting of options, stock appreciation rights (SARs) and other option-like awards. Under Item 402(x)(2), issuers must make tabular disclosure on a grant-by-grant basis of each option, SAR or similar award to the CEO and each NEO granted within the period beginning four days before the filing of a periodic report by an issuer or of the filing or furnishing of a Form 10-K, Form 10-Q or Form 8-K disclosing material nonpublic information, and ending one day after the applicable filing or furnishing. The new disclosure does not apply to equity awards that do not have an exercise price such as time- or performance-based restricted shares.

The table must include, for each named executive officer (as applicable) and on an award-by-award basis, (i) the grant date, number of shares and exercise price of the option award, (ii) the grant date fair value of each award computed using the same methodology as used for the issuer’s financial statements under GAAP, and (iii) the percentage change in the market price of the underlying securities between the closing market price of the security one trading day before and one trading day after the disclosure of material nonpublic information.

Item 401(x)(1) requires issuers to disclose their “policies and practices” regarding the timing of awards of stock options in relation to the release of material nonpublic information, and whether and how they take material nonpublic information into account when making such awards. The purpose of the narrative disclosure is to provide insight regarding the issuer’s practices regarding grants of options and option-like awards.

The new option grant disclosure follows SEC Staff Legal Bulletin No. 120, issued in November 2021, which provides guidance for companies as to how they should recognize and disclose the cost of providing “spring-loaded” awards to executives. As defined in SAB 120, a spring-loaded award refers to a “share-based payment award granted when a company is in possession of material nonpublic information to which the market is likely to react positively when the information is announced.” The guidance cautions that if grant-date fair value does not reflect the impact of material nonpublic information it may not be in compliance with GAAP, which could require a restatement.

Issuers may want to reconsider option grant practices to minimize any additional disclosures:

- Consider approving annual awards to have a grant date that is no earlier than the second business day after the release of the Form 10-K.

- For new hires, have a quarterly grant date that ties with the date of release of material nonpublic information, especially for executive officers.

- Be very careful about the timing of off-cycle or special grants.

Even careful planning may not avoid all disclosure. Although issuers usually can generally control the timing of periodic reports on Form 10-K or Form 10-Q, there may be times when a Form 8-K filing is required and the issuer does not control the timing, such as in the case of the resignation of an executive officer or director.

Corporate Governance Trends

ESG Governance and Managing ‘Anti-ESG’ Sentiment (Authors: Tess N. Wafelbakker and David H. Brown)

Environmental, social and governance (ESG), which is the framework in which companies can consider environmental, social and governance issues as a potential measure of value, has become a substantial factor in investment decision-making, finding favor among institutional investors, asset managers, investment funds, retail investors, governments, sovereign wealth funds, corporate investors, regulators and policymakers. This support is often attributed to the growing emphasis on sustainability and ethical practices in the corporate world. In practice, it might appear as actions to combat climate change, commitments to improving the community where the company is based, or implementing corporate governance reforms. Several large institutional investors, including Blackrock, Vanguard and State Street, have publicized that they consider ESG friendliness as a factor in determining where to invest client funds, and various investment firms are offering funds that invest based on ESG strategies.

During the 2023 reporting cycle, companies faced a shift in the focus on ESG – there was continued emphasis on its critical importance, but this was countered by demand for balance and increased regulatory parameters. The counter-demand, characterized as the “anti-ESG” movement, has been rising over the past year, and ESG criteria are facing both heightened scrutiny and uncertainty within the investment community and among policymakers. Some of the criticism and confusion surrounding ESG as investment criteria is centered on the absence of standardized metrics and definitions, a potential short-term focus, the possibility of conflict with fiduciary responsibilities and antitrust concerns.

One prominent critique leveled at ESG revolves around the lack of universally accepted standardized metrics and definitions and the fact that, until recently, ESG reporting has been largely voluntary. Notably, what one organization views as a positive ESG attribute may be interpreted differently elsewhere. This discrepancy is exacerbated by the multitude of entities that now provide ESG ratings – over 600, including Institutional Shareholder Services, MSCI ESG Research, Sustainalytics and the three major credit rating agencies. Each employs distinct methods to assess ESG performance, resulting in variances and inconsistencies. This absence of uniformity and standardization complicates the task of investment decision-makers, making it challenging to conduct accurate and consistent comparisons of ESG performance among different organizations and, in turn, select appropriate investments for specific portfolios. In recent years, some leading frameworks have emerged that feed into the ratings assessments and are common for voluntary reporting, including those established by the Task Force on Climate-related Financial Disclosures (TCFD), Global Reporting Initiative (GRI), and Sustainability Accounting Standards Board (SASB). In 2021, the International Financial Reporting Standards (IFRS) Foundation established the International Sustainability Standards Board (ISSB), which has been developing the IFRS Sustainability Disclosure Standards to build on the existing SASB standards with the goal of creating a unified set of global disclosure standards. The ISSB issued the first version of two sets of standards in June 2023 – one for general disclosures of sustainability-related financial information and the other for disclosing specific information about climate-related risks and opportunities.

Continued acceptance and consolidation of these standards should help to standardize information in a manner that allows for better comparison across organizations; however, to the extent that disclosure is still voluntary and lacks reporting oversight, it still may not provide a solid basis for investment decisions. While SEC climate change disclosure rules remain behind schedule, other regulatory initiatives have moved forward to establish mandatory reporting requirements. Namely, California’s enactment of the Climate Corporate Data Accountability Act and Climate-Related Financial Risk Act and the European Union’s Corporate Sustainability Reporting Directive (CSRD) aim to address these issues by introducing broad mandatory standards for ESG reporting. The California rules apply to both public and private U.S. companies generating over $1 billion and doing business in California and require disclosure in registration statements and periodic reports of Scope 1 and Scope 2 greenhouse gas (GHG) emissions beginning in 2026 and Scope 3 GHG emissions in 2027, as well as the submission of biennial climate-related financial risk reports to the California Air Resources Board beginning in 2026. These rules use the recommendations of the TCFD and impose broader requirements than the proposed rules issued by the SEC. The CSRD has a lower threshold than the California law and applies to (i) large EU companies, including EU subsidiaries of non-EU parent companies that meet at least two of these criteria: (1) an average of more than 250 employees, (2) a balance sheet total of more than €20 million, and (3) a net turnover of €40 million; (ii) companies having securities listed on an EU-regulated market; and (iii) non-EU companies having annual EU-generated revenues in excess of €150 million and with either a large or listed EU subsidiary or a significant EU branch. The CSRD requires these companies to disclose information necessary to understand the impact of their activity on sustainability matters as well as how sustainability matters affect the company’s development, performance and position, and will require detailed disclosure under the European Sustainability Reporting Standards (ESRS). A first set of the ESRS was adopted on July 31. While these rules promote a more uniform reporting framework across organizations, they also will extend their cost throughout the value chain. On Nov. 30, the European Financial Reporting Advisory Group (EFRAG), which develops reporting standards for the European Union, and GRI agreed to align their ESG disclosure standards, which will allow companies reporting under one framework to automatically satisfy requirements under the other. The agreement provides “joint interoperability tools,” which will minimize the compliance burden for the over 14,000 public and non-listed companies that make voluntary ESG disclosures.

A second critique pertains to ESG inadvertently encouraging organizations to prioritize short-term ESG enhancements to artificially inflate their ratings. For instance, companies investing to boost their ESG scores may do so with a short-term performance in mind rather than effecting meaningful long-term changes. Consequently, this approach, which centers on superficial ESG improvements, can detract from addressing more profound sustainability issues. Moreover, such tactics, often labeled “greenwashing,” whereby a company portrays itself as more environmentally and socially responsible than it genuinely is, are not only deceptive but also misallocate capital away from its efficient use.

A third criticism underscores the potential conflict between ESG adoption as an investment criterion and the fiduciary duties assumed by certain decision-makers. While certain financial managers can establish an investment policy statement aligned with client preferences, skeptics question whether certain fiduciary duties, particularly those of pension plan managers, are potentially compromised. Pension plan investment managers bear a fiduciary duty to act in the best interests of the plan’s beneficiaries, which typically involves maximizing financial returns while managing risk. Recent empirical financial research reveals mixed findings concerning the risk-adjusted returns on investments when employing a strict ESG-centric strategy. As pension plan beneficiaries exhibit diverse risk tolerances, time horizons and investment preferences, using ESG criteria as a nonfinancial metric poses an ongoing challenge in harmonizing these considerations with the overarching investment objectives of the pension plan.

Finally, there has been a surge in challenges to ESG initiatives based on antitrust law. One common practice among actors looking to implement ESG policies is to work alongside others in their industry. Of course, when companies cooperate in the marketplace, it raises antitrust concerns, even if the end is to advance ESG objectives. There is currently no exemption from antitrust laws for ESG initiatives, and the lack of exemption creates an opportunity for those opposed to such initiatives to use antitrust laws to potentially block ESG goals. Lawmakers have been increasingly scrutinizing ESG policies over the past several years. For instance, on Nov. 3, 2022, Sens. Tom Cotton, Chuck Grassley, Marco Rubio, Michael Lee and Marsha Blackburn sent a letter to 50 law firms, warning their corporate clients about participating in “climate cartels” or organizations advancing ESG efforts. The senators threatened to use their oversight powers to investigate any alleged antitrust violations in the name of ESG. This letter was followed shortly thereafter by Rep. Jim Jordan announcing an investigation into whether the ESG initiatives of the members of the Climate Action 100+ violated antitrust laws. State attorneys general are also calling for an investigation into the Climate Action 100+ while also pursuing investigations of other groups such as the United Nations Net-Zero Banking Alliance (NZIA). Most recently, on May 15, 23 state attorneys general sent a letter requesting documents from insurers in NZIA. The letter, which detailed purported collusive behavior on the part of NZIA members, alleged that NZIA’s protocols appear to violate both state and federal antitrust laws. While there are actions a company can take to advance ESG initiatives without risking liability under antitrust laws, there are also actions that could expose a company to antitrust liability. Recent litigation reflects how serious some in government are about using their powers under various bodies of law to oppose ESG efforts. Those looking to advance ESG initiatives through cooperation should be extremely wary of antitrust enforcement.

As the future of the ESG movement remains uncertain, companies must balance competing stakeholder interests and regulatory regimes. Despite recent resistance to ESG initiatives, corporate sustainability will continue to be a key concern for institutional investors and other stakeholders alike, as well as regulators. Companies should consider the following best practices with respect to ESG governance and disclosure:

- Add and/or enhance the process for ESG risk management/opportunity assessment and strategic planning. Boards should be educated on ESG-related topics and companies should seek directors with related experience and certifications. In addition, companies should (i) conduct assessments to determine which ESG-related risks, impacts and opportunities are material; (ii) consider peer and industry benchmarking and investor policies; and (iii) highlight the ESG oversight process in their disclosures.

- Monitor and update goals and regulatory compliance requirements. Once a company establishes and discloses its ESG goals, it should (i) continue to monitor such disclosures and objectives to ensure that they remain on track and assess whether any changes are appropriate; and (ii) consider the impact of pending regulations and develop a compliance strategy and update corresponding disclosures accordingly.

- Formalize the process for consistent and accurate disclosure. Companies should (i) integrate ESG disclosures into preparation, review and publication processes used for other public disclosures to ensure sufficient vetting and support; (ii) clearly identify third-party reporting frameworks, timeframes, assumptions and qualifications; (iii) pay attention to the difference between disclosing targets and stating aspirational goals, while also being wary of inadvertent incorporation by reference; and (iv) confirm that their disclosures are uniform and consistent across all media and filings.

Human Capital Management (Author: Tess N. Wafelbakker)

Human capital management (HCM) remains an increasingly significant component of ESG, carrying both risks and opportunities. HCM disclosures have remained a priority for the SEC over the past three years since the agency amended Item 101(c) of Regulation S-K in November 2020, and this heightened focus has resulted in sustained efforts to enhance disclosure requirements. Institutional investors and other stakeholders are also continuing to pay close attention to HCM, given the link between HCM systems and financial performance.

Companies are required to include human capital-related disclosures within the business section of their annual reports on Form 10-K to the extent such disclosures are material to an understanding of the company’s business. The term “human capital” is not defined in Item 101(c); instead, the SEC adopted a principles-based framework that allows companies to tailor disclosures according to their circumstances. However, this principles-based approach has been criticized as insufficient, and research has shown that it yields inconsistent disclosures that cannot be reliably compared by investors. Lawmakers and other rulemaking agencies are attempting to address these concerns.

In July, the Financial Accounting Standards Board issued a proposal to require that companies disaggregate the reporting of major operating costs, which would in turn require companies to disclose employee compensation costs included in the income statement. On Sept. 11, U.S. Sens. Mark R. Warner and Sherrod Brown reintroduced the “Workforce Investment Disclosure Act,” which seeks to build on existing disclosure requirements by requiring public companies to disclose information regarding workforce management metrics, including investments made in skills training, workforce health and safety, employee retention, workforce engagement, and employee compensation. Gensler has stated that these workforce metrics have been a priority of his agenda since the start of his tenure in 2021. Although the bill may not pass the current Congress, it serves as a basis for potential rule proposals.

In late September, the SEC’s Investor Advisory Committee (IAC) approved a report to the SEC containing recommendations calling for “fundamental HCM metrics to anchor industry- and company-specific information to seize opportunities and mitigate risks.” If implemented, the IAC recommendations would substantially increase HCM disclosure obligations. The IAC recommended that the SEC bolster current Item 101(c) by requiring disclosure of turnover or comparable workforce stability metrics; the total cost of the issuer’s workforce, broken down into major components of compensation, to allow investors to evaluate the issuer’s investments in human capital through various productivity measures; and workforce demographic data sufficient to provide investors with insight into the issuer’s efforts to access and develop new sources of talent, including diversity, equity and inclusion (DE&I) efforts, and to evaluate the efficacy of such efforts. The IAC also recommended that the SEC consider requiring narrative disclosure in the MD&A regarding how the issuer’s labor practices, compensation incentives and staffing fit within the company’s broader business strategy. HCM appeared on the SEC Rulemaking Agenda, and proposed rule amendments to enhance HCM disclosure requirements are anticipated later this year.

Separately, sustained pressure from institutional investors and other stakeholders continues to result in companies increasingly including human capital disclosures beyond those on Form 10-K in their sustainability/ESG reports and proxy statements. Companies should pay close attention to the evolving policies of their significant investors and consider what comparable disclosure is being provided by their peers, in addition to any rulemaking developments from the SEC, in approaching both Item 101(c) and any supplemental HCM disclosure in 2024.

Increased Focus on DE&I Efforts (Author: Tess N. Wafelbakker)

In recent years, calls for greater diversity in organizations led to a significant increase in board engagement with DE&I issues and implementation of robust DE&I policies. However, in the wake of the U.S. Supreme Court’s landmark affirmative action ruling in Students for Fair Admissions v. Harvard, corporate DE&I initiatives are coming under intense scrutiny, and boards should be proactive in mitigating the risk presented by a growing number of legal challenges to these efforts. While the Harvard decision relates directly to college and university admissions, mounting recent legal challenges to DE&I efforts in the private sector suggest it may have broader implications.

In July, attorneys general of 13 states sent a letter to the CEOs of Fortune 100 companies threatening “serious legal consequences” over DE&I policies and employment preferences based on race. The letter specifically referenced the Harvard decision and warned that certain race-based policies could violate both federal and state antidiscrimination laws. In addition, private litigation challenges have begun and are expected to continue. Several challenges claim individual discrimination, alleging that adverse employment decisions were the result of DE&I policies, and programs have also been challenged by membership and nonprofit organizations.

Shareholder activists have also attempted to attack DE&I programs, through the shareholder proposal process and derivative suits. In 2023, such proposals fared poorly, with less than 1 percent support on average. In August, the U.S. District Court for the Eastern District of Washington ordered dismissal of a stockholder derivative suit on behalf of Starbucks Corporation against certain of its officers and directors claiming that certain of Starbucks’ diversity initiatives violated federal and state antidiscrimination laws, and also that directors breached their fiduciary duties by implementing such policies. Underpinning the court’s judgment was deference to the business judgment rule.

Companies should regularly and carefully review their DE&I programs and policies to ensure compliance with the law, as legal challenges are expected to continue. Evaluations of DE&I programs should be based on an informed exercise of business judgment, and companies should consider how such programs legitimately advance the mission of their businesses.

Universal Proxy and Bylaws Amendments (Author: John J. Harrington)

The SEC’s universal proxy rule went into effect in the fall of 2022. This rule requires that, in a proxy contest, the company and the activist stockholder list each other’s nominees on their proxy cards. Prior to this rule, voting stockholders generally had to choose between the competing slates of directors. Now, voting stockholders can mix and match to vote for particular directors from each of the competing slates. An activist stockholder running a proxy contest must still file a proxy statement with all required disclosures and solicit votes (at least 67 percent of the voting power, according to the rule). This is a key distinction from the proxy access bylaws that many large companies have adopted, which allow qualifying stockholders to submit a nomination and rely on the company’s proxy statement to provide the necessary disclosure.

After a year of experience under the universal proxy rule, we do not believe it has caused a major change in activist campaigns and proxy contest practices. Time will tell if this occurs over time, but in terms of numbers of campaigns, numbers of proxy contests, costs and other characteristics, we have not seen any major shifts thus far. Concerns have been raised that proxy contests might increase because an activist could in theory run a very basic proxy contest for limited cost, but that has not occurred in meaningful numbers and we believe there is a very limited set of circumstances where such an approach would make sense for an activist.

After the universal proxy rule went into effect, many public companies amended advance notice bylaws in response. Technical amendments to conform to the requirements and process under the new rule are straightforward and not controversial. Some companies also took the opportunity to amend other provisions of their advance notice bylaws to modernize them or bolster their informational and process requirements. In the latter case, this may have been at least partially driven by some recent Delaware case law where the court has upheld rejections by companies of nomination notices by activists. Whether or not related to the universal proxy rule and subsequent bylaw amendments, one trend that appeared in 2023 and is worth watching going forward is an uptick in company rejections of nomination notices by activists as well as related litigation.

Spotlight on Board Efficacy (Authors: Tess N. Wafelbakker and David H. Brown)

Board efficacy has come under increased scrutiny in recent years, with heightened performance expectations driven by both internal and external forces. This scrutiny has led to greater exposure to reputational harm and legal challenges for directors.

Oversight Responsibilities

Fundamental responsibilities of the board include overseeing management and implementing an effective governance regime. This includes the task of monitoring and assessing the performance of senior managers responsible for day-to-day operations and, to be effective, requires continuous review and balance of the company’s strategic initiatives, financial performance, financial reporting processes and compliance. Boards must identify and monitor risks, particularly those critical to the company’s operations, which requires a deep understanding of risks associated with the specific corporate strategy and the company’s processes for managing those risks.

Many public companies assign the oversight of corporate risks to their audit committees. Audit committee members typically have financial and accounting expertise, but may lack experience in other key risk areas such as cybersecurity. Historically, the existence of dedicated risk or compliance committees has been rare, with approximately 9 percent of boards having risk committees, 4 percent having separate compliance committees, and 4 percent having committees focused on environment, health, and safety according to a 2020 National Association of Corporate Directors (NACD) survey of Russell 3000 companies. However, as more specialized skills are needed for boards to understand and assess emerging and complex areas of risk, boards are encouraged to periodically evaluate their structure and committee membership to ensure alignment with the company’s needs. Responsible directors need to have the capacity to review information and control systems to ensure timely attention to relevant issues and risks, and relying on an audit committee that already has significant responsibility may no longer be the ideal approach.

Director Qualifications

In parallel to the evolving oversight challenges and priorities, there has been a noticeable shift in the qualifications sought for members of boards of directors. Traditionally, boards primarily sought individuals with extensive experience in the industry, often focusing on executives or leaders who had successfully been leaders in similar business environments. While industry expertise remains crucial, as noted above, there is an increasing recognition of the need for a broader set of skills and perspectives, such as expertise in the areas of technology, cybersecurity, digital transformation, environmental sustainability and human capital management, as well as with respect to legal, operations and financial issues. This reflects a recognition that businesses today are influenced by factors beyond traditional industry boundaries, including rapid technological advancements, changing consumer expectations and a heightened focus on ESG issues. This enhanced focus on diversity of skill sets complements the continuing emphasis that boards and investors are placing on gender and racial diversity.

A recent victory for more traditional diversity initiatives was the Oct. 18 denial by the U.S. Court of Appeals for the Fifth Circuit of petitions to review the SEC’s approval of the Nasdaq diversity disclosure rule implemented in August 2021. The rule requires companies listed on the Nasdaq exchanges to have at least two diverse board members (female and minority or LGBTQ+) or to explain the company’s reason for not meeting the diversity objective. Nasdaq-listed companies are also required to disclose diversity statistics in a board diversity matrix in their company’s proxy statement (or if companies do not file a proxy, on Form 10-K or 20-F) or on their website. As the rule remains in effect, companies listing on Nasdaq on or after Aug. 6, 2021, should be prepared to comply with the requirement to have at least one diverse director or provide an explanation for failing to achieve such metric by Dec. 31. For additional information on Nasdaq’s diversity requirements, see our alert “SEC Approves Nasdaq Board Diversity Proposal,” dated Aug. 18, 2021. Beyond Nasdaq, many other parties are focused on enhanced board diversity, including state and federal lawmaking agencies, proxy advisory firms, and institutional investors, and this is an element of board composition that will continue to be an area of focus in the coming years.

As a result of these factors, the board’s skill and other attribute matrix should be continuously reviewed, along with board succession plans, to make sure all areas contributing the right diversity mix for the company’s needs are accounted for.

Director Reputational and Liability Risk

Directors can face liability for a failure to provide adequate oversight and, even if the high bar for an actual determination of liability is not met, legal challenges can be costly and distracting and result in reputational harm to the company and the directors. The Delaware court decision in the In re Caremark International Inc. Derivative Litigation,in which the company failed to comply with certain external legal requirements, held that directors could be held accountable for a breach of fiduciary duty in connection with such activity only in cases of a “sustained or systematic failure of board oversight.” Due to such a high standard, post-Caremark Delaware courts often dismissed shareholder lawsuits that claimed a board had a complete lack of oversight responsibility.

Recent rulings, however, suggest that there is still a risk for director liability for oversight failures. Courts have allowed claims alleging breaches of fiduciary duties to survive a motion to dismiss when boards allegedly overlooked issues related to compliance, safety, reporting or other risks or failed to adequately address such issues despite existing company-wide policies. The courts consider factors such as a history of unaddressed deficiencies and a lack of documented active board supervision to determine whether there was “a deliberate failure to act,” and continue to recognize the existence of board risk management and compliance structures as evidence to the contrary.

As a result, it is wise for boards to establish and document effective communication channels between management, the board, its committees and other key company employees in order to adequately oversee risk. While companies cannot eliminate all risk, adopting an effective risk management system that emphasizes timely identification of key enterprise risks, communication of necessary information to relevant executives and the board, and implementation of appropriate monitoring and mitigation systems will reduce the threat of reputational harm and legal challenges arising from an alleged systemic failure of board oversight.

Artificial Intelligence Considerations (Author: Brittany Stevenson)

The rapid rise and adoption of artificial intelligence (AI) possesses the potential to transform entire industries through its ability to deliver new capabilities, mirroring human intelligence, performance and comprehension. This transformative power is not without risk. AI may impact company affairs in a variety of ways and across different areas including corporate governance, labor and employment, consumer protection and relations, product liability, privacy, data protection and cybersecurity, intellectual property ownership and rights, insurance, and government laws, regulations, and policies. The potential benefits of AI in each of these respective areas are vast. To illustrate, AI may be used to identify and mitigate potential risks, or it may be used to collect and analyze data for business or financial projections. In order to ensure the corporate use of AI is responsible, and that data is safeguarded, companies and boards of directors will need to possess a comprehensive understanding of AI’s role and establish a framework for continuous oversight.

Companies and boards of directors should consider (1) the specific opportunities for use and innovation that AI may present for their businesses; (2) any particular and general AI-related risks; (3) the impact of AI use on company stakeholders, including employees, vendors, customers and stockholders; (4) evolving international, federal and state laws and regulations with respect to AI; and (5) oversight of AI use and the development of policies and compliance programs. Board involvement and oversight with respect to AI will be crucial to ensure that AI is used not only to further company strategic objectives and values but also ethically and responsibly. Therefore, to take full advantage of the potential benefits of AI, companies and boards should be proactive in their AI preparations and governance framework. In the U.S., various regulatory bodies are contemplating regulation of AI, including the IRS and the SEC, and companies should closely monitor developments in this area.

[1] Audit Analytics – SEC UPLOAD comment letters issued related to Forms 10-K and 10-Q for the 12-month period ended June 30, excluding SPACs and other blank check entities.

[View source.]