On July 17, 2019 the IRS released Notice 2019-45 resolving a preventive care problem that has been plaguing many high deductible health plans (“HDHPs.”). The Affordable Care Act’s free preventive care mandate appears to be working. People are catching medical problems sooner. As a result, many employers have embraced the concept of free preventive care and want to go a step further – providing free preventive care for certain chronic conditions, such as asthma, diabetes, and heart disease. However, they have run into a snag. Under IRS guidance, treatment for chronic conditions is not “preventive care” and covering it before the deductible is met jeopardizes the plan’s status as an HDHP.

Before IRS Notice 2019-45 was released, free preventive care for certain chronic conditions could not be provided under an HDHP before the deductible was met because IRS guidance provided that preventive care generally does not include any service or benefit intended to treat an existing illness or injury. The Notice provides a good summary of the prior guidance on preventive care.

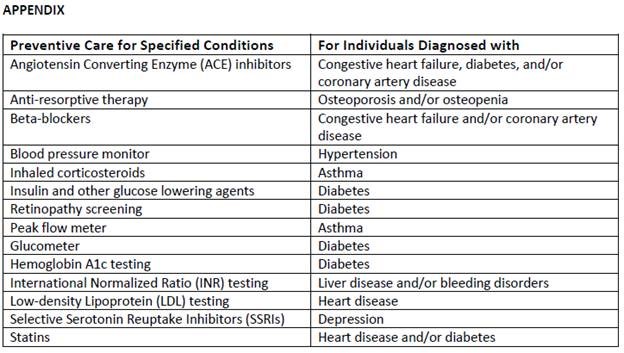

Now, in addition to items that are preventive care under prior guidance, the medical services received and items purchased, including prescription drugs, for certain chronic are deemed to be preventive care for someone with that chronic condition. The list below is from the Appendix to Notice and is an exhaustive list of the medical services and drugs that are deemed to be preventive care for the treatment of the specified chronic conditions. The Notice indicates that the list will be updated every five to ten years.

The Notice is effective July 17, 2019. Employers that want to take advantage of these new rules may need to adopt plan amendments and prepare employee communications explaining the new rules. Health plans must be careful that they do not provide free preventive care for chronic conditions beyond what is listed in the Appendix. Doing so would cause a health plan to not be an HDHP, rendering all participants, not just those who receive free preventive care for chronic conditions, ineligible to make or receive health savings account (“HSA”) contributions.