See all chapters of A Guide to Solvency II.

Introduction

Group supervision regulates the impact that members of a Solvency II group may have on a UK Solvency II insurer. The rules governing Solvency II groups are contained in the PRA Rulebook (Group Supervision), the Solvency 2 Regulations 2015 (the Solvency 2 Regulations) and Articles 328 to 350 of Commission Delegated Regulation (EU) 2015/35 (Retained EU Law) (the Level 2 Delegated Regulation), and are supplemented by, among other things, PRA Supervisory Statement SS9/15: Group Supervision (as updated) (PRA SS9/15). The rules governing Solvency II groups set standards that must be maintained by the Solvency II group as a whole. In this chapter we set out the rules on group supervision that apply in the UK.

1. Types of Solvency II Groups

There are four scenarios where group supervision applies on a group-wide basis.

Scenario 1

Scenario 1 occurs when a UK Solvency II insurer owns directly or indirectly 20% or more of the voting rights or capital of, or otherwise exercises significant influence over, at least one other UK Solvency II insurer or third-country (re)insurer.

Scenario 2

Scenario 2 involves a UK Solvency II insurer that has a parent entity which is an insurance holding company or a mixed financial holding company with its head office in the UK or Gibraltar.

An insurance holding company is a parent entity that is not a UK Solvency II insurer or a mixed financial holding company, whose main business is to acquire and hold participations in subsidiary undertakings that are either exclusively or mainly UK Solvency II insurers or third-country (re)insurers, or ancillary insurance service undertakings, and where such entities comprise more than 50% of two or more of:

- The parent entity’s consolidated assets.

- The parent entity’s consolidated revenues.

- The group solvency capital requirement (SCR) (as if calculated at the level of the parent entity).

At least one of the parent entity’s subsidiary undertakings must be a UK Solvency II insurer.

A mixed financial holding company is a parent entity other than a regulated entity which, together with its subsidiaries, at least one of which is a regulated entity with its head office in the UK, and other entities, constitutes a financial conglomerate, as defined by the applicable rules.

Scenario 3

Scenario 3 occurs where the top company is an insurance holding company, a mixed financial holding company or a third-country (re)insurer with its head office outside the UK.

Group Supervision 20.1 provides that, as a default position (and unless otherwise agreed with the PRA), the PRA must rely on the equivalent group supervision exercised by the third-country supervisory authorities where the jurisdiction of the third country supervisory authority has been deemed equivalent. At the time of this publication, only Switzerland, Bermuda and the EEA member countries have been deemed to be equivalent for these purposes (note also the position explained below regarding US-parented groups).131

If there is a sub-group headed by an insurance holding company, additional group supervision can be imposed at the level of the UK Solvency II sub-group. Conversely, where it would be more efficient and, importantly, supervisory efforts are not negatively impacted, the PRA can exempt any UK sub-group from additional supervision.

Where the jurisdiction of the third-country parent entity is not equivalent, the PRA has the flexibility to determine whether to regulate the entire group (i.e., from the third-country parent entity down) or, if satisfactory other methods can be agreed, from the level of the top UK holding company down. The PRA exercises this jurisdiction through the UK Solvency II insurer’s authorisation. The purpose of other methods pursuant to Group Supervision 20.1(2) is to ensure sufficiency of governance and prudential solvency at that lower level, and therefore other methods structures will involve ensuring that the group (and, in particular, the constituent UK Solvency II insurers) have appropriate governance, staffing, boards, independence and access to capital when it is required.

Scenario 4

Scenario 4 occurs where a UK Solvency II insurer has a parent entity that is a mixed-activity insurance holding company.

The extent of group supervision for Scenario 4 groups is limited. Parent companies of Scenario 4 groups are not insurance holding companies due to the fact that holding interests in (re)insurers is not its primary business and the group’s main activities are non-financial. The revised definition of insurance holding company has made the delineation between what is a mixed-activity insurance holding company and an insurance holding company clearer, though the presence of insurance intermediaries in a group who place most of their insurance business with group insurers (and/or group insurers who receive most of their business from group intermediaries) continues to complicate matters, especially in the case of Gibraltar carriers.

In determining if a group with a UK Solvency II insurer or a third-country (re)insurer falls within Scenario 4, one must first consider if the parent entity of the group is a UK Solvency II insurer or a third-country (re)insurer. Second, one must consider whether the parent entity is an insurance holding company. Third, one must consider whether the parent entity is a mixed financial holding company. If the answer is no, in respect of the above three stages, the parent entity is a mixed-activity insurance holding company.

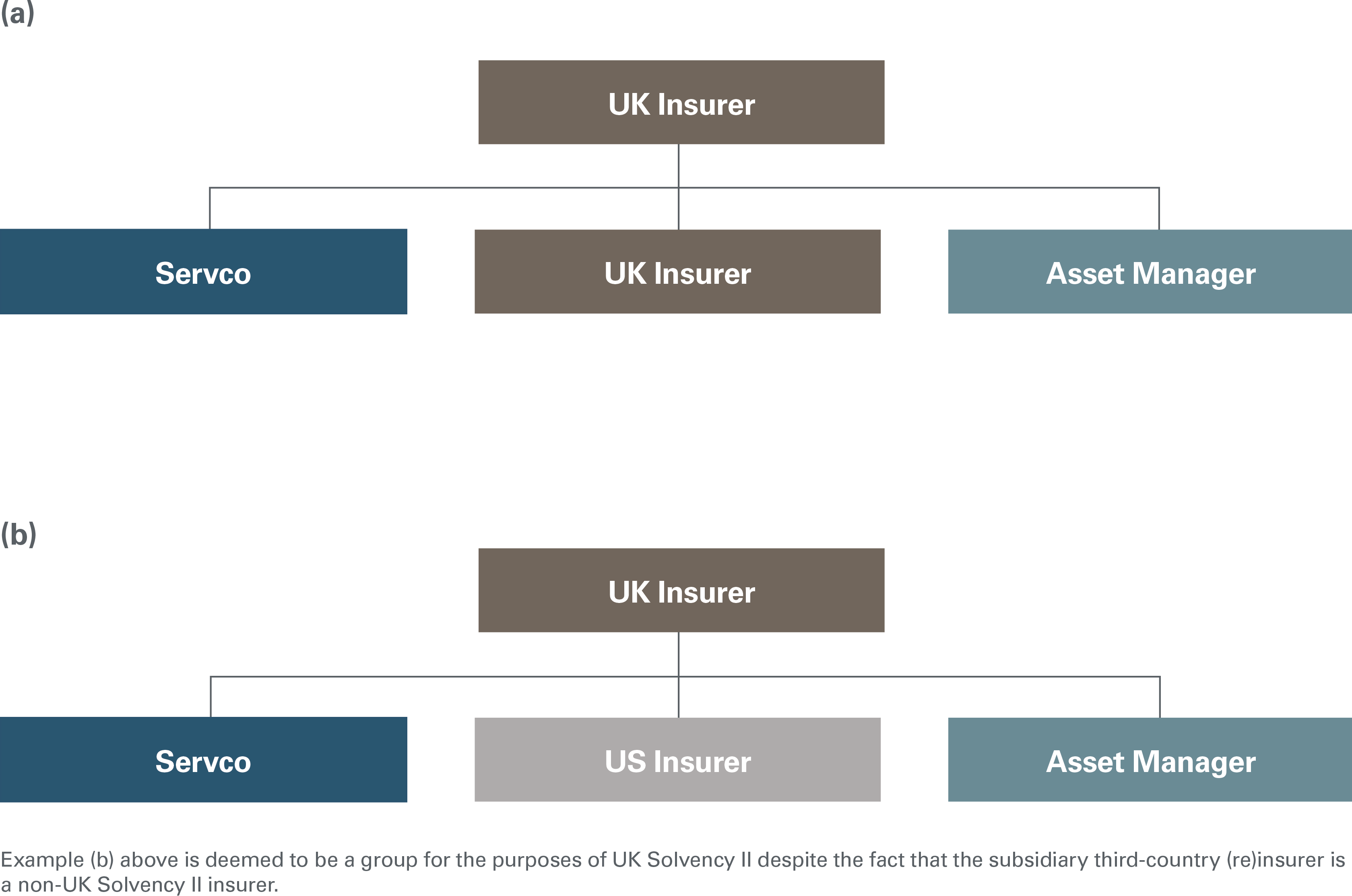

Existence of a UK Solvency II Group at Different Levels of the Group Structure

As noted in the diagram below, a UK Solvency II group can exist at different levels in a group structure.

In this scenario, Group Supervision 2.1 mandates that group supervision rules will apply only at the level of the ultimate UK Solvency II insurer, UK insurance holding company or UK mixed financial holding company in the group. If the ultimate holding company’s head office is outside the UK, the applicable rules will depend on whether the jurisdiction in which the entity is incorporated is deemed to be equivalent to the UK and, if not, whether other methods apply. Note that Regulation 13 of the Solvency 2 Regulations mandates that the PRA has the option to supervise the group at a UK level where a group’s head office is in Gibraltar.

2. Group Supervision: Applicable Rules and Specific Considerations Depending on Type of Group

Scenario 1 and Scenario 2 Groups

Both Scenario 1 and Scenario 2 groups are supervised pursuant to the rules set out in the Group Supervision section of the PRA Rulebook, which includes rules governing group solvency (discussed in the next section), group reporting requirements, certain requirements regarding intra-group transactions, and certain risk management and internal control requirements.

Group Supervision 17 sets out the governance requirements that apply at the level of a Scenario 1 and Scenario 2 group, which are largely similar to the equivalent solo level governance requirements. Requirements include carrying out a group own risk and solvency assessment (ORSA) and implementing risk management and internal control systems.

Pursuant to Group Supervision 16.2, Scenario 1 and 2 groups must report on a regular basis (at least annually) to the PRA all “significant” intra-group transactions by (re)insurers. A very significant intra-group transaction must be reported as soon as practicable. Article 377 of the Level 2 Delegated Regulation makes it clear that an intra-group transaction can be considered “significant” if it would materially influence the solvency or liquidity position of the group or one of the companies involved in the transaction. The PRA expects to be notified of any very significant intra-group transaction before the relevant company has entered into the transaction. Article 377 of the Level 2 Delegated Regulation includes a non-exhaustive list of such transactions.

Scenario 3 Groups

In respect of Scenario 3 groups, Regulation 35 of the Solvency 2 Regulations provides that the PRA must rely on the equivalent group supervision exercised by the third-country supervisory authorities where the jurisdiction of the third-country supervisory authority has been deemed equivalent.

At the date of this publication, only Bermuda, Switzerland and the EEA member countries have been deemed to be equivalent for this purpose. Due to bilateral arrangements between the UK and the US pursuant to the Bilateral Agreement Between the United States of America and the United Kingdom on Prudential Measures Regarding Insurance and Reinsurance (the UK/US Bilateral Agreement) supervision for US-parented groups occurs at the level of the US parent entity and by the supervisor in that parent entity's home state, with the PRA having the ability to supervise at the level of any UK sub-group.

To exercise the process outlined in the UK/US Bilateral Agreement, UK Solvency II insurers in a US-parented group must apply for a rule modification. The application process is standardized. The PRA will issue bespoke individual other methods directions to UK Solvency II insurers that meet the requirements in the UK/US Bilateral Agreement, which effectively amend the requirements of Group Supervision 20.1 and 20.2.

The UK/US Bilateral Agreement streamlines the administrative impact for insurance groups with a US parent entity by requiring that each relevant member of the group and the UK insurance holding company provide to the PRA its group risk report (ORSA or equivalent) within one month of providing same to its US supervisor. The submission including the group risk report must include:

- A description of the (re)insurance group’s risk management framework.

- An assessment of the (re)insurance group’s risk exposure.

- A group assessment of risk capital and a prospective solvency assessment.

As regards to insurance groups with an EU parent entity, a single group supervisor is designated the group supervisor as per Article 247 of the Solvency II Directive.

If there are (re)insurers in more than one EU member state, and the relevant group is:

- Headed by a parent entity that is an (re)insurer, the group supervisor will be the national regulator that supervises that (re)insurer.

- Not headed by a parent entity that is a (re)insurer, Article 247 sets out a number of different factors that must be taken into account in establishing who the group supervisor should be, for example:

- Where more than one (re)insurer shares its headquarters with the same insurance holding company or mixed financial holding company, the supervisory authority of those (re)insurers shall be the group supervisor.

- Where the group is headed by more than one insurance holding company or mixed financial holding company that have their head offices in different EU member states and there is a (re)insurer in each of those EU member states, the supervisory authority of the (re)insurer with the largest balance sheet total shall be the group supervisor.

- Where multiple (re)insurers that have their head offices in the EU also have as their parent the same insurance holding company or mixed financial holding company, and none of the entities have been authorised in the member state in which the insurance holding company or mixed financial holding company has its head office, the supervisory authority that authorised the (re)insurer with the largest balance sheet total shall be the group supervisor.

- Where the group does not have a parent entity, the supervisory authority that authorised the (re)insurer with the largest balance sheet total shall be the group supervisor.

Under Article 247, each relevant national supervisor can dispute whether the selection criteria has been applied appropriately. In the event of a disagreement, EIOPA has ultimate authority to resolve any dispute. Article 248 of the Solvency II Directive sets out the rights and duties of the group supervisor. Article 249 of the Solvency II Directive sets out obligations regarding the cooperation and exchange of information between regulators of (re)insurers in the group.

3. Group Solvency Calculation for Scenario 1 and 2 Groups

Groups falling within Scenarios 1 and 2 are required to calculate their group solvency in accordance with relevant provisions of the PRA Rulebook (Group Supervision 4 to 14). In respect of Scenario 1, it is the UK Solvency II insurer that is required to ensure that group solvency requirements are met. In respect of Scenario 2, where the group is headed by an insurance holding company or a mixed financial holding company, it is the UK Solvency II insurers in the Solvency II group that are responsible for ensuring compliance with group solvency requirements.

There are two possible means of calculating group solvency:

- Method 1: the “accounting consolidation method.”

- Method 2: the “deduction and aggregation method.”

Differing from Method 1, under Method 2, diversification benefits between group members are not recognised. Additionally, the use of local rules is possible under Method 2 for the calculation of group solvency where the relevant non-UK entity is in an equivalent jurisdiction (at this time, Switzerland, Bermuda or an EEA member country).

While Method 1 is the default (Group Supervision 7.1(2)), the PRA may allow Method 2 or a combination of both to be used (a partial Method 2 approach). When assessing whether or not to allow the use of Method 2, the PRA must consider if:

- There is a sufficient amount and quality of information available in a particular instance to allow for the use of Method 1.

- The use of Method 1 be disproportionately burdensome.

- Intra-group transactions are not significant both in terms of volume and value.

- The group includes non-UK entities that are equivalent (either provisionally or absolutely).

The use of Method 2 (in whole or part) most often occurs where the overseas operations of a group are located in a jurisdiction deemed equivalent for group solvency purposes.

4. Group Solvency Calculation: Method 1

Group Supervision 11.1(2) provides that under Method 1 group solvency is assessed by calculating the difference between:

- The own funds eligible to cover the SCR, calculated on the basis of consolidated data.

- The SCR at group level, calculated on the basis of consolidated data.

Consolidation includes all related undertakings whether they are regulated undertakings or not; but not all types of undertaking are included on a fully consolidated basis.

The own funds and SCR sections of the PRA Rulebook apply in respect of the calculation of:

- The group SCR based on consolidated data.

- The calculation of own funds eligible at group level.

Entities Included in the Method 1 Calculation

Group entities not included in the scope of group supervision are excluded from the calculation. It is explicitly stated in Article 335 of the Level 2 Delegated Regulation that consolidated data in respect of each group entity is included, save where:

- Necessary information in respect of an undertaking necessary to calculate group solvency is not available, in which case the book value of that entity must be deducted from the own funds eligible for the group solvency capital requirement and the unrealised gains connected with the participation must not be recognised as own funds eligible for the group solvency capital requirement.

- A company has been excluded from group supervision by the PRA where there are legal impediments to the transfer of information.

- The relevant entity is a special purpose vehicle and compliance has been made with certain relevant requirements.

Data Included in the Method 1 Calculation

The basic principle is that Method 1 uses consolidated data from all entities within the Solvency II group and own funds is calculated as if the Solvency II group was one single insurer. There is proportional consolidation of data where members of the group share control of an entity with an entity outside the group. The proportional share of a group entity’s holdings in credit institutions, investment firms and UCITS management companies, among others, are calculated on the basis of sector specific rules.

Article 335 of the Level 2 Delegated Regulation specifies that the consolidated data should include:

- Full consolidation of data of the following types of undertaking where they are subsidiaries of the parent entity:

- (Re)insurers.

- Third-country (re)insurers.

- Insurance holding companies.

- Mixed financial holding companies.

- Ancillary insurance services undertakings.

- Full consolidation of data of SPVs to which the participating undertaking or one of its subsidiaries has transferred risk and that are not excluded from the scope of the group solvency calculation under Article 329(3).

- Proportional consolidation of data of the same types of undertaking as are referred to in the first bullet above, but where they are managed jointly by one of the aforementioned undertakings and one or more other undertakings.

- Data of all holdings in the types of undertaking referred to in the first bullet above that are not subsidiaries of the parent entity and to which the proportional consolidation does not apply, on the basis of the adjusted equity method.

- The proportional share of the undertakings’ own funds calculated in accordance with the relevant sectoral rules in relation to holdings in related undertakings that are:

- Credit institutions.

- Investment firms.

- financial institutions.

- Alternative investment fund managers.

- UCITS management companies.

- Institutions for occupational retirement provision.

- Non-regulated undertakings carrying out financial activities.

- In accordance with Article 13 of the Level 2 Delegated Regulation, data of all other related undertakings (including ancillary service undertakings, collective investment undertakings and investments packaged as funds) other than those referred to above.

As a default, related undertakings must be valued using quoted market prices in active markets as provided for in Article 10(2) of the Level 2 Delegated Regulation. Where this is not possible the adjusted equity method should be applied. If the adjusted equity method cannot be used, alternatives should be considered.

It may be necessary for adjustments to be made in order to:

- Account for the non-availability or transferability of own funds.

- Eliminate intragroup creation of capital and double use of own funds.

- Address the impact of matching adjustment portfolios and ring-fenced funds.

Third-Country Subsidiaries

It is irrelevant under Method 1 whether or not third-country (re)insurers in the group are in equivalent jurisdictions because the calculation will be carried out by applying Solvency II rules to consolidated data of the group as a whole. A partial use of Method 2 in respect of specific undertakings can be requested by a group. The PRA has wide discretion over whether or not the request is granted.

Treatment of Own-Fund Items

Under Method 1, own-fund items of third-country (re)insurers are classified using the tests set out in Article 332 of the Level 2 Delegated Regulation and Group Supervision 11.3, with adjustments appropriate to the group calculation.

Proportional Shares

Pursuant to Group Supervision 8.1, the calculation of group solvency under Method 1 should take into account the proportional share held in related undertakings that are not 100% owned. Under Group Supervision 8.3, where the subsidiary undertaking does not have sufficient eligible own funds to cover its SCR, unless the PRA decides otherwise, the total solvency deficit must be taken into account in the group solvency calculation.

In addition, Group Supervision 8.3(2) allows for the PRA to determine the applicable proportional share in unusual circumstances, i.e., where the participation is held in an unusual way, such as significant influence.

Treatment in Method 1 Calculation of Ring-Fenced Funds and Matching Adjustment Portfolios

Ring-fenced funds and matching adjustment portfolios should not be fully consolidated in the Method 1 group solvency calculation. Method 1 groups will need to consider the availability and transferability of own funds attributable to a ring-fenced fund or matching adjustment portfolio. Article 330(4) of the Level 2 Delegated Regulation specifies that restricted own-fund items within ring-fenced funds would not be considered as effectively available to cover the group SCR.

Minimum Capital Requirement (MCR) Under Method 1

Where Method 1 is used to calculate group solvency, the consolidated group solvency capital requirement must be, at a minimum, the sum of the MCR of each insurance carrier in the group and the proportional share of the MCR of the related Solvency II undertakings.

For groups using Method 1, the sum of solo MCRs (the group MCR floor) can potentially prove to be higher than the group SCR, which has the effect of, in practice, limiting the diversification benefits available under Method 1.

5. Group Solvency Calculations: Method 2 (Deduction and Aggregation Method)

Method 2 calculates the group solvency requirement based on the accounts of the solo entities. It is calculated by comparing:

- The aggregated group eligible own funds on the one hand.

- The aggregated group solvency capital requirement plus the value in the participating undertaking of the related undertakings.

The value of the related undertakings is added to avoid double counting between the value of those participations in the parent and the own funds of those undertakings in their contribution to group own funds.

Method 2 does not, unlike Method 1, facilitate the recognition of diversification benefits on an intragroup basis.

The application of Method 2 to third-country (re)insurers means, however, that there may be a less onerous treatment than the application of Solvency II rules to the assets and liabilities of those (re)insurers on a consolidated Method 1 basis. Method 2 may also allow for a more practical calculation where calculation on a Solvency II basis may be problematic in respect of the assets and liabilities of a third-country (re)insurer.

With regard to the own funds calculation and SCR and in the absence of equivalence, Group Supervision 10.4 states that SCR and own funds calculation should be carried out by applying Solvency II rules, which may be difficult to apply in practice and may negatively and materially impact group solvency calculations if such entities are significant relative to the size of the Solvency II regulated insurance group.

Equivalence for Group Solvency Purposes

Regulation 19 of the Solvency 2 Regulations provides for equivalence in respect of third-country (re)insurers within a Solvency II group. This is not relevant for the application of the Method 1 calculation, under which Solvency II rules are applied to all consolidated data.

Where the third-country regime is equivalent, the PRA must permit the group to take into account the own funds eligible to satisfy the SCR in the calculation of group solvency, and with respect to national laws adopted by the third country in respect of the group’s SCR, unless it is not in the interests of policyholders to do so or there has been a significant change in the relevant third-country regime. If the third-country (re)insurer is not subject to equivalent supervision, its contribution to the group SCR and group own funds must be calculated on the basis of Solvency II rules.

At the time of this publication, only Switzerland, Bermuda and the EEA member countries have been found to be equivalent for these purposes.132

Under the UK/US Bilateral Agreement, where a U.S. (re)insurer is subject to a local group capital requirement, the PRA must not impose a group capital requirement or assessment at the level of the worldwide parent undertaking of the insurance or reinsurance group.

Treatment of Non-Insurance Undertakings

It is unclear how other related regulated entities should be treated under Method 2. Group Supervision 12.1 to 12.3 only requires the SCR and own funds of the participating (re)insurer and its related (re)insurers and, by virtue of Group Supervision 10.4, related third-country (re)insurers to be taken into account in calculating group solvency.

Article 329 of the Level 2 Delegated Regulation requires, however, the group solvency calculation to include capital requirements and own funds, calculated in accordance with applicable sectoral rules (e.g., for investment firms, credit institutions, UCITS management companies, alternative investment fund managers, etc.) and, in addition, a notional capital requirement and own funds for related undertakings that are non-regulated undertakings carrying out financial activities.

Under Method 2, non-regulated related undertakings (other than those carrying out financial activities) are included as assets of the relevant regulated parent entity within the group calculation and valued in accordance with Article 13 of the Level 2 Delegated Regulation.

Availability and Transferability

As is the case for Method 1 groups, Method 2 groups will need to consider the availability and transferability of own funds attributable to a ring-fenced fund or matching adjustment portfolio. Article 330(4) of the Level 2 Delegated Regulation specifies that restricted own-fund items within ring-fenced funds would not be considered as effectively available to cover the group SCR.

Proportional Shares

The same provisions apply with respect to Method 2 save that, instead of the proportional share being calculated as the percentage used for the establishment of the consolidated accounts, pursuant to Group Supervision 8.2(2), the proportional share is calculated as the proportion of the subscribed capital held, directly or indirectly, by the participating undertaking.

MCR Under Method 2

Whereas under Method 1 the consolidated group SCR must be, at a minimum, the sum of the MCR of each insurance carrier in the group and the proportional share of the MCR of the related Solvency II undertakings, there is no comparable requirement for Method 2. This is because the Method 2 deduction and aggregation method results in a SCR that exceeds the sum of the MCR of each insurance carrier in the group plus the proportional share of the MCRs of the related undertakings that are not wholly owned or controlled.

6. Group Solvency Calculations: Aspects That Apply to Both Method 1 and Method 2

Holding Companies

Group Supervision 14.1 provides that the group solvency calculation should be carried out at the level of that holding company where (re)insurers are subsidiaries of an insurance holding company or mixed financial holding company. Group Supervision 10.3 states that where a group includes a (re)insurer indirectly holding a participation in a related (re)insurer through an insurance holding company or mixed financial holding company, the relevant intermediate holding company through which that (re)insurer holds those shares should be treated as if it were a (re)insurer subject to the rules on SCR and own funds for the purposes of the group solvency calculation.

Elimination of Double Use of Own Funds and Intragroup Creation of Capital

Own funds that represent the same assets in two separate entities must not be double counted. For example, the value of one insurer's holding of ordinary shares in another insurer should not be valued as both an asset of the first insurer and an own fund item of the second insurer. Group Supervision 9.1, 9.7 and 9.8 set out provisions to avoid such double counting. These provisions state that the following shall be excluded from the group SCR calculation:

- The value of any asset of the participating UK Solvency II insurer that represents the financing of own funds eligible for the SCR of one of its related (re)insurers.

- The value of any asset of a related (re)insurer of the participating UK Solvency II insurer that represents the financing of own funds eligible for the SCR of that participating UK Solvency II insurer or any other related (re)insurer of the UK Solvency II insurer.

- Own funds arising out of reciprocal financing between the participating UK Solvency II insurer and a related undertaking, participating undertaking or another related undertaking of any of its participating undertakings.

- Own funds of a related (re)insurer of a participating UK Solvency II insurer arising out of reciprocal financing with any other related undertaking of that UK Solvency II insurer.

Group Supervision 9.8 states that reciprocal financing includes situations where one undertaking holds shares in or makes loans to another undertaking that holds own funds eligible for the SCR of the first undertaking. Article 335(3) (for Method 1) and Article 342(1) (for Method 2) of the Level 2 Delegated Regulation mandate the elimination of intra-group transactions in the group own funds calculation.

Treatment of Undertakings Regulated Under Another Sector

Other regulated entities are included in the insurance group solvency calculation based on their own sectoral rules. Article 329 of the Level 2 Delegated Regulation provides that the calculation of group solvency shall include:

- The capital requirements for related undertakings that are credit institutions, investment firms or financial institutions and the own-fund items of those undertakings calculated according to the relevant sectoral rules referred to in Article 2(7) of the Financial Conglomerates Directive.

- The capital requirements for related undertakings that are institutions for occupational retirement provision and the own-fund items of those undertakings calculated according to Articles 17 to 17c of the IORP Directive (2003/41/EC).

- The capital requirements for related undertakings that are UCITS management companies and the own fund items of those undertakings calculated in accordance with the relevant provisions of Article 7(1)(a) of Directive 2009/65/EC and the own funds of those undertakings calculated in accordance with point 1 of Article 2(1) of that Directive 2009/65/EC.

- The capital requirements for related undertakings that are alternative investment fund managers calculated in accordance with Article 9 of the Alternative Investment Fund Managers Directive (2011/61/EU) and the own funds of those undertakings calculated in accordance with Article 4(1) of that directive.

Special Purpose Vehicles (SPVs)

If an SPV complies with Solvency II requirements or is governed by rules that are deemed to be equivalent, it can be excluded from the group solvency calculation under Article 329(3) of the Level 2 Delegated Regulation.

Availability and Transferability

Pursuant to Group Supervision 9.4, if a supervisory authority considers that own funds eligible for the SCR of a related (re)insurer are not capable of being made available to cover the SCR of the participating undertaking for which group solvency is calculated, those own funds may only be included in the group solvency calculation to the extent that they are eligible for covering the SCR of the related undertaking to which the own funds belong.

Pursuant to paragraph 5A.2 of SS9/15, a group must set out its own assessment of any items that, due to any significant restriction affecting the availability, fungibility or transferability, might be deducted from own funds. Unless a formal determination is made by the PRA in respect of a particular own fund item, a group should report own-fund items as available (notwithstanding its own assessment), except where the treatment of that own-fund item is specifically referenced under Group Supervision 9.1 - 9.6 and Article 330 of the Level 2 Delegated Regulation.

Paragraph 5A.4 of SS9/15 provides that the assessment of the availability of own-fund items of a third-country related undertaking must, instead of being assessed under local rules, must be assessed by reference to the UK group provisions, where a group uses Method 2 for the calculation of its solvency requirements.

Group Supervision 9.2 states that subscribed but not paid-up capital of related (re)insurers of the participating (re)insurer and surplus own funds for which the group solvency is being calculated can only be included in the group solvency calculation insofar as they are eligible for covering the SCR of the related undertaking concerned. Group Supervision 9.3 states that where subscribed but not paid up capital of a relevant related undertaking represents a potential obligation of the participating undertaking or another relevant related undertaking, or vice versa, the amount must be excluded from the calculation entirely.

Paragraph 5A.2B of PRA SS9/15 clarifies that a group should not consider the solo SCR as restricting the availability of own-fund items or assets at group level where the relevant related (re)insurer is subject to the UK Solvency II regime. The PRA expects Solvency II groups to engage from an early stage with the PRA should there be any doubt as to the availability and transferability of group own-fund items.

Paragraph 5A.2E of PRA SS9/15 states that different valuation bases and quality of capital permitted for the purpose of local regulatory requirements may affect the availability of any capital that represents the difference between the contribution to the group SCR and the solo SCR, but also the availability of any surplus capital in excess of the local solo regulatory requirement. The PRA expects UK Solvency II insurers to take this into account when providing it with information on which the PRA will base its judgements as to the point at which other regulators would intervene to restrict flows of capital out of their jurisdiction.

Group Supervision 9.4, itself, refers only to non-availability of own funds eligible for the SCR of related (re)insurers. Therefore, the requirements with regard to other related undertakings is unclear.

Article 330 of the Level 2 Delegated Regulation expands on Group Supervision 9.4:

- Article 330(1) provides that, in assessing whether own funds can effectively be made available to cover the group SCR, supervisory authorities must consider whether:

- The own-fund item is subject to a legal or regulatory requirement that restricts the ability of the item to absorb all types of losses wherever they arise in the group.

- There are legal or regulatory requirements that restrict the transferability of assets to another (re)insurer in the group.

- Making those own funds available for covering the group SCR would not be possible within a maximum of nine months.

- Where Method 2 is used, the own-fund item does not satisfy the requirements set out in Articles 71, 73 and 77 of the Level 2 Delegated Regulation (features determining classification for Tier 1, Tier 2 and Tier 3 own funds), where the term SCR in those articles is to mean both the SCR of the issuer of the own funds and the group SCR.

- Article 330(2) provides that supervisory authorities should consider the Article 330(1) restrictions on an ongoing concern basis and should also take into account any likely costs to the relevant undertaking of making the own funds available for the group.

- Article 330(3) lists items that should be assumed not to be effectively available to cover the group SCR, unless the participating undertaking can demonstrate to the satisfaction of the supervisory authority that this assumption is inappropriate in the circumstances (but see Article 330(5) referred to below). These are:

- Ancillary own funds.

- Preference shares, subordinated mutual members accounts and subordinated liabilities.

- Net deferred tax assets (after deducting the associated deferred tax liability).

Where subordinated debt is intended to be used as group own funds, the UK Solvency II insurer will need to be able to demonstrate to the PRA that such debt should be eligible. The UK Solvency II insurer will need to satisfy the PRA that these own fund items are available to absorb losses anywhere in the group. A firm may demonstrate this through intragroup guarantees, but this is not likely to be appropriate for most groups. The PRA is receptive to proposals for alternative approaches that address the legal restrictions associated with such instruments.

Pursuant to Article 330(4) of the Level 2 Delegated Regulation, the following items should not be considered as effectively available to cover the group SCR:

- Any minority interest in a subsidiary that is a (re)insurer, third-country (re)insurer, insurance holding company or mixed financial holding company exceeding the contribution of that subsidiary to the group SCR.

- Any minority interest in a subsidiary ancillary services undertaking.

- Any restricted own-fund item in a ring-fenced fund.

Where an own fund item of a related (re)insurer, third-country (re)insurer, insurance holding company or mixed financial holding company cannot effectively be made available to cover the group SCR, it can be included in the calculation of group solvency but only up to the contribution of that undertaking to the group SCR.

As stated in paragraph 5A.3 of SS9/15, a group must provide to the PRA details of how own funds may be made available, for example, by paying dividends or selling the assets of an undertaking or insurance holding company to recapitalize other group companies in difficulty, which the PRA will consider when reviewing a group's assessment of transferability. The PRA will expect a group to demonstrate that own funds can be made available within a maximum of nine months, otherwise it will not be able to apply group own funds treatment to those particular own-fund items. It is questionable how the nine month rule can be applied in practice. Particular supervisory scrutiny/judgment is required in respect of assumptions made by insurance groups, which may be unrealistic.

Paragraph 5B.1 of SS9/15 provides clarity on how firms may demonstrate that subordinated liabilities and preference shares are available to absorb losses anywhere in the UK Solvency II group. For example by demonstrating that:

- Each (re)insurer (including any (re)insurer acquired after the relevant instruments were issued) in the Solvency II group has the right to claim against the issuing entity if that (re)insurer is wound up and there is a shortfall for its policyholders and beneficiaries. Furthermore, the right of the group (re)insurers to claim on the issuing entity does not significantly increase group risks, including the level of complexity when winding up and contagion risk for issuing entities that are (re)insurers.

- The legal obligations of the issuing entity to the holders of the instruments, including coupon payments, are subordinated to any claims made by group (re)insurers that are being wound up.

Pursuant to paragraph 5B.1D, the PRA considers, however, that intragroup guarantees used for this purpose increase certain risks in the group, particularly where:

- The issuing entity is a (re)insurer.

- There are multiple (re)insurers in the group.

- The issuing entity is a subsidiary of an entity that either has related (re)insurers or is a (re)insurer.

- There are significant intragroup transactions (both in terms of volume and value).

The PRA expects that it will not be appropriate to use intragroup guarantees to ensure that subordinated liabilities and preference shares are available for these purposes for most groups. Correspondingly, the PRA is receptive to other approaches that UK Solvency II insurers may wish to propose when seeking to demonstrate availability of subordinated liabilities and preference shares, but these must address the legal restrictions derived from such instruments. The PRA will assess such proposals on a case-by-case basis. These complexities are a material driver for large groups to consolidate their carriers, in so far as reasonably possible.

Classification of Group Own Funds

The Level 2 Delegated Regulation sets out rules for how the own funds of group companies should be classified in respect of the group solvency calculations, and these rules apply to both the Method 1 and Method 2 calculations.

Own Funds of Related (Re)insurers at Group Level

Article 331(1) of the Level 2 Delegated Regulation states that own funds of (re)insurers in the group will be classified at group level in the same tier as they are classified at solo level except that:

- The items must be free from encumbrances and not connected with other transactions that would undermine their satisfaction of the relevant criteria at group level (Article 331(1)(b)).

- In order to qualify as group own funds, the item must meet the requirements of Article 71, 73 or 77 of the Level 2 Delegated Regulation (as applicable) both on a solo and a group basis. This means that references to SCR and MCR should be read also to mean the group SCR and the minimum group SCR, and references to the (re)insurer shall be read to mean the participating (re)insurer. Therefore, for example, to qualify as Tier 2 own funds at group level a Tier 2 subordinated debt instrument issued by a related (re)insurer will need to provide for deferral of distributions both on breach of the issuing undertaking's SCR and on a breach of the group SCR (Article 331(1)(a); Article 331(2); and Article 331(3)).

- Own-fund items included in Tier 2 at solo level by of Article 73(1)(j) of the Level 2 Delegated Regulation — i.e., those that which meet the Tier 1 requirements but exceed the limits on subordinated mutual member accounts, preference shares, subordinated liabilities and grandfathered items set out in Article 82(3) of the Level 2 Delegated Regulation — can be included in Tier 1 at group level if the limits set out in Article 82(3) would be met at group level (Article 331(4)).

Group Level Own Funds of Related Third Countries

Own funds of related third-country (re)insurers should be classified using the criteria set out in Articles 69 to 79 of the Level 2 Delegated Regulation with the following additional requirements:

- The items must be free from encumbrances and not connected with other transactions that would undermine their satisfaction of the relevant criteria at group level (Article 332(1)(b)).

- For the purposes of assessing compliance with Article 71, 73 or 77 of the Level 2 Delegated Regulation: (i) SCR shall mean the group SCR; and (ii) MCR shall mean both the capital requirement of the issuing undertaking as laid down by the relevant third-country supervisory authority and the minimum group SCR (Article 332(2)).

Own Funds of Insurance Holding Companies, Mixed Financial Holding Companies and Ancillary Insurance Services Undertakings at Group Level

Own funds of insurance holding companies, intermediate insurance holding companies, mixed financial holding companies, intermediate mixed financial holding companies and subsidiary ancillary insurance services undertakings are classified using the criteria set out in Articles 69 to 79) of the Level 2 Delegated Regulation with the following additional requirements:

- The items must be free from encumbrances and not connected with other transactions that would undermine their satisfaction of the relevant criteria at group level.

- For the purposes of assessing compliance with Article 71, 73 or 77 of the Level 2 Delegated Regulation: (i) SCR shall mean the group SCR; and (ii) MCR shall mean both the minimum group SCR and the insolvency of the insurance holding company, intermediate insurance holding company, mixed financial holding company, intermediate mixed financial holding company or subsidiary ancillary insurance services undertaking.

- References to the (re)insurer shall be read to mean the insurance holding company, intermediate insurance holding company, mixed financial holding company, intermediate mixed financial holding company or subsidiary ancillary insurance services undertaking which has issued the own-fund item.

Own Funds of ‘Residual Related Undertakings’ at Group Level

Article 334(1) of the Level 2 Delegated Regulation prescribes that own funds of other related undertakings will be considered as part of the reconciliation reserve at group level. Article 334(2) provides that the own-fund items should be classified into tiers based on the criteria set out in section 2 of the Level 2 Delegated Regulation where practicable and where the own fund items are material.

Subordination to Group Policyholders

Recital 127 to the Level 2 Delegated Regulation states that:

“In order to ensure that the policyholders and beneficiaries of insurance and reinsurance undertakings belonging to a group are adequately protected in the case of the winding-up of any undertakings included in the scope of group supervision, own-fund items which are issued by insurance holding companies and mixed financial holding companies in the group should not be considered to be free from encumbrances unless the claims relating to those own-fund items rank after the claims of all policyholders and beneficiaries of the insurance and reinsurance undertakings belonging to the group.”

Paragraph 6.5 of SS3/15 states that the PRA expects that the terms of instruments issued by insurance holding companies or mixed financial holding companies should include terms providing that in the case of winding up proceedings of any firm in the group until all obligations by that member of the group to its policyholders and beneficiaries have been met repayment of amounts due under the instrument are refused. In the absence of such provision, the instrument will not qualify as group own funds. The PRA subsequently confirmed in discussions with firms that:

- The deferral applies only to redemption and not payment of interest.

- The requirement does not extend to the winding up of the issuing insurance holding company or mixed financial holding company itself.

7. Group Internal Models

Group Supervision 11.4 provides that an application can be made to use an internal model to calculate either only the group SCR or both the group SCR and the SCR of (re)insurers within the group.

Articles 343 to 350 of the Level 2 Delegated Regulation sets out details of the application requirements and approval procedures.

____________

131 The EU has, at the time of writing, not determined that the UK is equivalent to the EU Solvency II regime, although there are rumors that the EU position may be starting to soften. In respect of EU insurance groups with a UK-domiciled parent, EU member state regulators cannot rely on group supervision exercised by the PRA in respect of EU insurance groups with a UK ultimate parent entity.

132 As at the time of publication, no reciprocal determination has been made by the EU in respect of the UK. UK insurers will need apply EU Solvency II rules to calculate the contribution of the UK undertakings to group SCR.

Download PDF

[View source.]