[author: Chris van Heerden]*

The FDIC set up the SVB bridge bank on March 26, which meant that Q1 bank earnings reports and industry data largely reflected a business environment that had ceased to exist by the time the numbers hit the tape. With the Q2 call report season now largely complete, the new operating environment is becoming clearer. Here are the main contours:

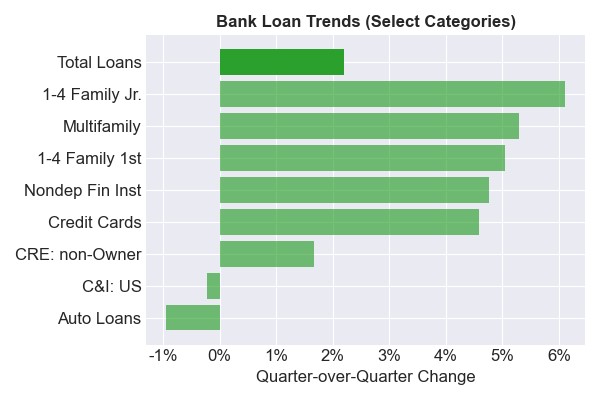

- Asset trends. Bank balance sheets are tilting towards loans, with positive growth in this category, while securities and cash holdings are moving lower. We expect this trend to continue as banks reposition the asset side of the balance sheet to keep track with rising liability costs.

Note: Same-store-sales analysis for institutions that have filed a Q2 2023 call report.

Source: Bankregdata and Cadwalader, Wickersham & Taft LLP.

- Loan Growth. Where is the loan growth coming from? Loans to non-depository financial institutions, where fund finance loans are often included, posted a 4.7% growth rate over the quarter – an impressive annualized clip. (Growth in junior single-family loans may be sign of financially stretched consumers.)

Note: Same-store-sales analysis for institutions that have filed a Q2 2023 call report.

Source: Bankregdata and Cadwalader, Wickersham & Taft LLP.

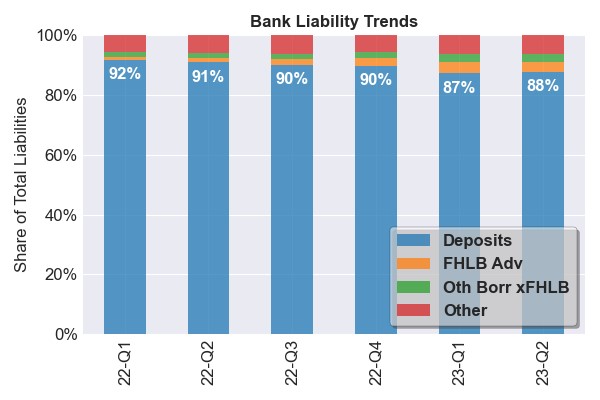

- Liability trends. Liability mix has been shifting away from deposits in recent quarters (with attendant effects on funding costs). In Q2, headline deposits stabilized, but internals weren’t as positive.

Note: Incudes all reporting institutions for each period.

Source: Bankregdata and Cadwalader, Wickersham & Taft LLP.

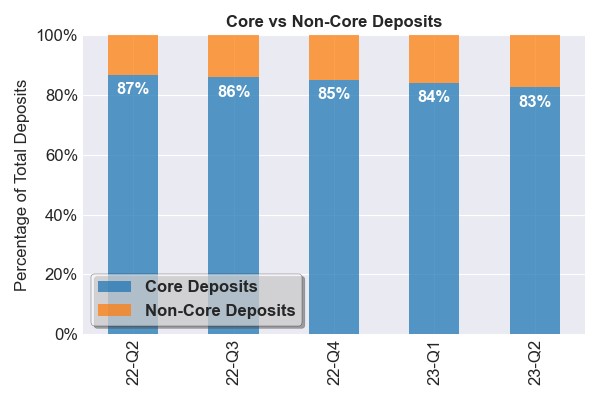

- Deposit internals. Apparent deposit stability was partially manufactured as the share of brokered deposits rose at many institutions and core deposits declined.

Note: Incudes all reporting institutions for each period.

Source: Bankregdata and Cadwalader, Wickersham & Taft LLP.

What does this mean for the industry?

First, funding costs are rising, owing to both rate and cost structure changes. On the rate side, banks continue to compete directly with money market funds and a heavy Treasury Bill issuance calendar, and indirectly with the Fed through its reverse repo facility. Structurally, increased reliance on non-core deposits and secured borrowing (FHLB advances, pledged securities, etc.) adds further upward pressure to funding costs. This means profitability will continue to face pressure, which Moody’s underscored when it downgraded 10 banks on Monday, placed six on review for possible downgrade, and revised the outlooks for 11 banks to negative. More specific to fund finance, we expect margins to stay wide given this context.

Second, we continue to expect the asset mix to tilt towards loans and away from cash and securities as played out in Q2. But recycling the balance sheet into higher yielding assets happens at a much slower pace than liability re-pricing. Rising non-performing loans in some sectors and difficultly in resolving off-sides asset-class concentrations slow the ability to reposition. Capital rules are also evolving.

While long-end rates are rising, the yield curve slope still favors originating at the short-end of the curve. Deposit duration uncertainty favors a shorter loan tenor. Put together, this means fund finance originations may prove resilient but the pace may slow further.

Third, much of the data suggests that the banking industry is ripe for consolidation. Acquisition accounting can relieve core issues facing some institutions and help acquirers fill in their footprint. The capital regime, however, functions like a progressive tax and will influence where combinations make sense. Nonetheless, we’ll likely see a continued reduction in the number of banks in existence in the U.S. over the next five years.

Finally, we’re in an era for new ideas in lending. The incentive to solve for additional capital on the borrower side or for risk participation on the lender side has never been higher in the history of fund finance. We think that the potential payoffs for solving for term funding, securitization, CRT, pref equity, NAV and who knows what other solutions will define the direction of businesses in years to come. (Whether lenders can hack the model to pay innovators outside of basic revenue production could also prove defining – a topic for another day.) We are positioned at the forefront of these developments in the fund finance market and welcome a conversation on where you see your business going.

*Director, Fund Finance