Welcome to the Credit, Debit, or Prepaid Cards and Consumer Banking chapter of our annual report Consumer Financial Services 2023 Year in Review.

Looking Ahead to 2024

We expect continued focus by the CFPB on “junk” fees, including enforcement actions and rulemakings.

We anticipate the potential adoption of a new rule limiting the type and amount of fees lenders can charge.

Key Trends From 2023

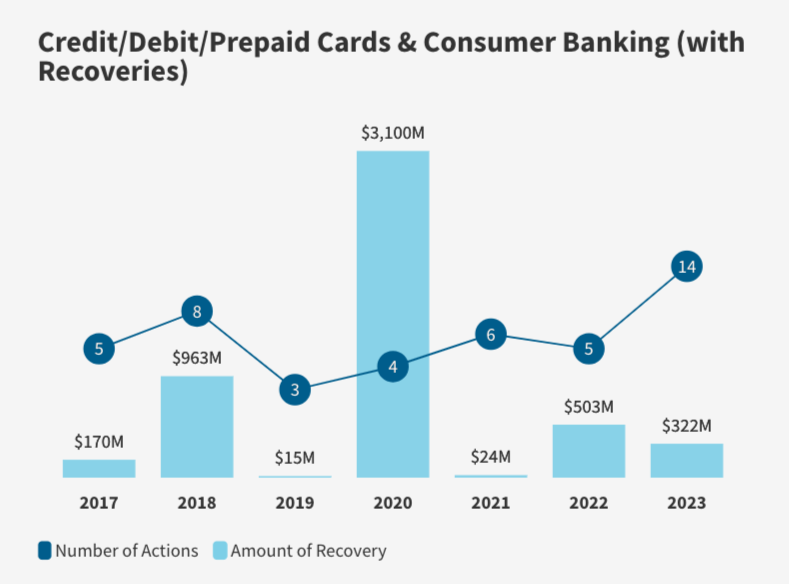

In 2023, Goodwin tracked 14 publicly announced enforcement actions related to credit, debit, or prepaid cards or consumer banking. Financial institutions faced enforcement actions regarding a variety of allegations ranging from technical Regulation Z violations to intentional ethnic discrimination. This represents an increase in the number of publicly announced enforcement actions from five such actions in 2022. Total recoveries amounted to more than $322 million in 2023, a decrease from last year’s recovery of $503 million.

In the News

Consistent with 2022, the CFPB continued its focus on “junk fees,” a broad term the CFPB has used to describe a wide range of fees financial institutions may charge consumers, ranging from so-called “surprise” overdraft fees to fees charged for basic information requests to “pay-to-play” fees. In announcing its report analyzing “junk” fees and interest charged to credit and debit card consumers, the CFPB highlighted its finding that American consumers paid $130 billion in interest and fees on their credit cards. CFPB Director Chopra stated, “[w]ith credit card debt crossing the trillion dollar mark, we will be working to prevent bait-and-switch tactics when it comes to rewards and to increase refinancing activity so consumers can get lower rates.” At the Consumer Law Scholars Conference, CFPB Deputy Director Zixta Martinez noted that junk fees “ignore consumer preferences, take away financial flexibility, distort markets, and increase costs.”

On April 13, 2023, while testifying before the Pennsylvania House of Representatives, CFPB Senior Advisor Brian Shearer stated that the CFPB has “been using every tool at our disposal to fight illegal junk fees, including rules, guidance, enforcement, and supervision.” He pointed to several examples of actions the agency has taken, including a proposed rule that would reduce credit card late fees by $9 billion a year, a 2022 enforcement action ending with the defendant bank paying nearly $200 million in relief for charging its customers “surprise” overdraft fees, and the recently released report on the CFPB’s findings of junk fees in confidential examinations.

The rule highlighted by Shearer, proposed on February 1, 2023, would limit the amount of late fees consumers incur through three primary provisions: (1) lowering immunity provision in the Credit Card Accountability Responsibility and Disclosure Act of 2009, which allows for certain late fees, to $8 for a missed payment (the CFPB has reported that some banks have charged consumers as much as $41 for each missed payment); (2) ending the automatic annual inflation adjustment of said fee amount; and (3) capping late fees at 25% of the required minimum payment.

Moreover, the CFPB’s October 2023 guidance concerning Section 1034(c) of the CFPA noted that “requiring a consumer to pay a fee or charge to request account information, through whichever channels the bank uses to provide information to consumers, is likely to unreasonably impede consumers’ ability to exercise the right granted by section 1034(c), and thus to violate the provision.” In its guidance, the CFPB provided a nonexhaustive list of the types of activity for which charging fees could violate Section 1034(c): “(1) to respond to consumer inquiries regarding their deposit account balances; (2) to respond to consumer inquiries seeking the amount necessary to pay a loan balance; (3) to respond to a request for a specific type of supporting document, such as a check image or an original account agreement; and (4) for time spent on consumer inquiries seeking information and supporting documents regarding an account.” This guidance is consistent with the CFPB’s growing intolerance for fees affiliated with consumer banking accounts that Goodwin has noted over the past two years.

2023 Enforcement Highlights

CFPB Reaches $9 Million Settlement with Bank Over Regulation Z Allegations

In May, the CFPB announced it had reached a settlement with a national bank to resolve allegations that the bank had violated consumer protection laws in connection with credit card transactions by “fail[ing] to properly manage and respond to customers’ credit card disputes and fraud claims.” The settlement brought an end to a 2020 lawsuit involving allegations that the bank violated TILA (and its implementing Regulation Z) by (1) improperly denying customer reports of fraud and errors and failing to provide refunds, and (2) failing to provide required documents and referrals to customers who had submitted billing errors. In addition to paying a $9 million fee, the bank agreed to make several changes to its credit card, including “prohibiting its employees from requiring customers to provide a fraud affidavit signed under penalty of perjury in support of a credit card claim” and ensuring that it refunds any fees or other charged amounts in response to valid billing-error notices and unauthorized use claims.

Bank Pays Nearly $27 Million to Settle Discrimination Claims Brought by CFPB

In November, the CFPB and a national bank entered into a consent order to resolve allegations that the bank engaged in intentional discrimination against Armenian Americans who had applied for credit cards with the bank. The CFPB alleged that between 2015 and 2021, the bank singled out credit card applicants suspected of being of Armenian descent based on their surnames and applied more stringent criteria to such applications, “including denying them and requiring additional information or placing a block on the account.” The CFPB further asserted that bank supervisors instructed employees not to discuss the practice in writing or on recorded phone lines and that employees were taught to lie about the reason for the adverse actions against the applicants, typically citing suspected credit abuse. According to the CFPB, these practices violated the Equal Credit Opportunity Act and its implementing regulation, Regulation B, and the Consumer Financial Protection Act (CFPA). Pursuant to the consent order, the bank has agreed to pay $1.4 million to affected consumers as well as a $25.4 million penalty.

CFPB and OCC Enter Into Consent Orders With Bank Over Allegations Regarding Its Prepaid Benefit Debit Accounts

In December, the CFPB announced it had entered into a consent order with a national bank regarding its handling of consumers’ prepaid card unemployment benefits accounts. During the COVID-19 pandemic, the bank had contracts with at least 19 states to deliver unemployment benefits to consumers through its prepaid card. The CFPB accused the bank of violating the CFPA and EFTA by (1) failing to provide consumers with accurate instructions as to how to unfreeze their accounts when certain antifraud controls were triggered, and (2) failing to provide provisional credits pending the investigation of unauthorized transfers reported to the bank under Regulation E. Under the consent order with the CFPB, the bank agreed to pay $5.7 million in redress to consumers as well as a $15 million fine. The Office of the Comptroller of the Currency separately fined the bank $15 million in a coordinated investigation.

[View source.]